What do you do when one of the most promising growth stocks of the last two years falls over 71% year-to-date? Do you go all in, or do you avoid it like the flu? If the stock is Unity Software (U), you could consider buying the dip because this stock will likely surge when the market stabilizes. We are bullish on Unity Software stock.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Unity creates and deploys 3D content. It is one of the most important players in the game development space. The company says, “Our platform provides a comprehensive set of software solutions to create, run, and monetize interactive, real-time 2D and 3D content for mobile phones, tablets, PCs, consoles, and augmented and virtual reality devices.”

If you’ve played games like Temple Run, Angry Birds, or Super Mario Run, you’ve been playing games built on Unity platforms.

Why Did Unity Stock Crater Recently?

Unity stock had been steadily falling in 2022 as part of the market sell-off. The company hit the $210 level in November 2021. As the pandemic began to die down and the gaming world cooled down, so did Unity stock. However, the company has also fallen over 14% since it released its Q1 2022 earnings on May 10.

Revenue came in at $320.1 million, up 36% from Q1 2021. Revenue from its Create Solutions (this is the company’s core development segment for both gaming and non-gaming companies) was up 65% to $116.4 million.

Next, revenue from Operate Solutions (this is the segment that develops ad tools, analytics, and other tools and features for developers) was up 26% to $184 million.

Finally, Strategic Partnerships (this segment handles deals with gaming companies) brought in $19.7 million in revenue, up 11% from Q1 2021. These are all very decent numbers, so what explains the fall?

A major reason was the company’s weak guidance for Q2 2022. Revenue guidance for Q2 was just $290 million to $295 million, up 6%-8% year-over-year but down almost 8% quarter-over-quarter. Revenue guidance for the whole year was $1.35 billion to $1.42 billion, up 22%-28% year-over-year. However, Unity’s earlier guidance for 2022 expected growth of 36%. The market gave a big thumbs down to these numbers.

The reason why 2022 revenues are not going to be great is because of a glitch in Unity’s Operate Solutions segment. Its Audience Pinpointer tool, which delivers targeted audience campaigns, suffered software problems. A lot of data that flowed through Unity platforms was not analyzed, and as a result, the company couldn’t monetize it. This led to a reduction of almost $110 million in revenue estimates.

If you exclude the Audience Pinpointer’s malfunction, the company would have matched expectations, and maybe the stock wouldn’t have suffered.

Why Unity Software Stock is Attractive

Unity Software President, Chief Executive Officer, and Executive Chairman, John Riccitiello, said, “While there are external factors to consider, the Operate challenge is mostly caused by internal factors in Unity monetization in an otherwise healthy market. We see these challenges as temporary and not structural and do not expect them to impact future prospects of our business beyond 2022.”

Riccitiello said that Apple’s changes to its privacy policy were not the major reason for the dip in revenues. He said Unity was able to navigate Apple’s policy change but was hit hard by two issues. The first one was the Audience Pinpointer malfunction. The second one was that “we lost the value of a portion of our data, training data due in part to us ingesting bad data from a large customer.”

Unity has said it expects a recovery period where it will rebuild its data and improve its model before revenue recovers and customers scale up, leading to more monetization. The company has also delayed the launch of certain features on the Audience Pinpointer.

Unity, prior to Q1 2022 earnings, had given guidance that it would grow revenues at 30% year-over-year. If we take the CEO’s comments at face value, the company will grow slower only in 2022 and be back on track in 2023. You have to keep in mind that 2023’s growth will be on a lower base than the one predicted earlier.

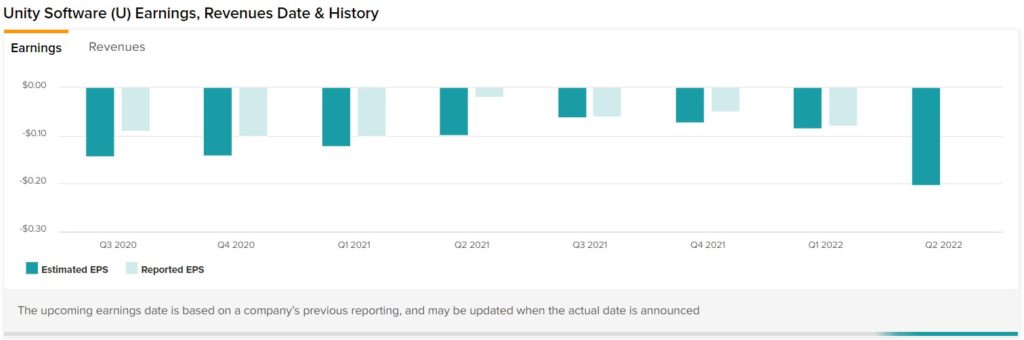

The company has 1,083 customers that have spent over $100,000 in the last 12 months. This number grew 29% from 837 customers in Q1 2021. Outside the gaming segment, the company has around 3,000 customers creating digital replicas of physical worlds so they can experiment in them. The company’s loss per share was $0.08 compared to a loss of $0.10 in Q1 2021. Unity’s bottom-line numbers have improved.

Wall Street’s Take

Turning to Wall Street, Unity Software has a Strong Buy consensus rating based on 11 Buys and three Holds assigned in the past three months.

At $76, the average Unity Software stock forecast implies 83.9% upside potential.

Conclusion

Unity stock is trading at around 8x its forward enterprise-value-to-sales ratio. If you believe in the company’s long-term potential (like us), then it could prove to be a great purchase. The metaverse is set to grow rapidly in the coming years, and companies like Unity will be in a prime position to benefit from this growth.

Read full Disclosure