After a stretch of volatility that came off the back of President Trump’s global tariff announcements, the stock market has shifted back into rally mode as worries over the proposed tariffs have eased. The S&P 500 has jumped 20% from its April low, while the tech-heavy Nasdaq has surged 27%.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

The gains have investors in a mood to buy – but the uncertainties have them wondering just how far to take that. In a climate like this, it’s good to have a reliable navigational aid for the stock markets, a tool to point out just which stocks show the highest potential for gains, no matter how events shake out.

That’s where TipRanks’ Smart Score comes in. Powered by AI, this tool sifts through millions of daily stock transactions and evaluates equities based on factors shown to predict future performance. Each stock is rated on a scale from 1 to 10, with ‘Perfect 10’ stocks checking all the right boxes.

We used the tool to pinpoint two of these top scorers. Both carry ‘Strong Buy’ consensus ratings and offer double-digit upside potential. Here’s what you need to know.

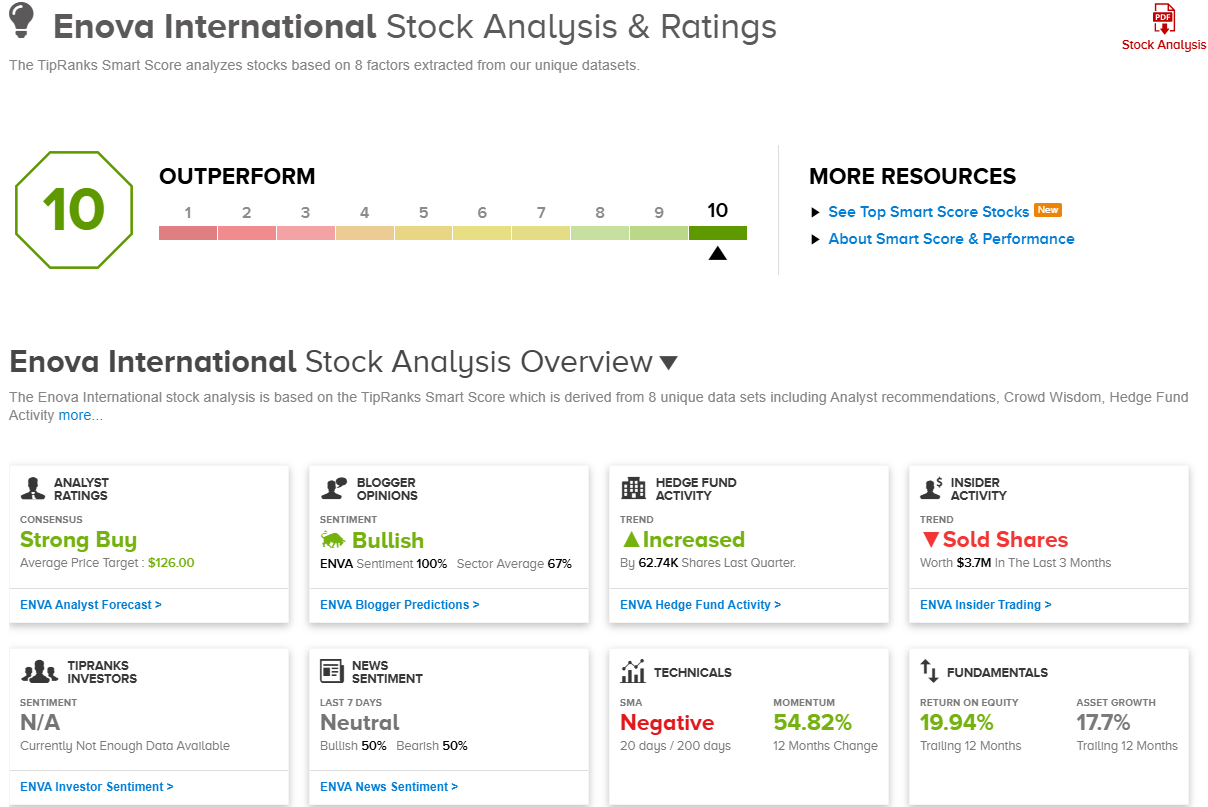

Enova International (ENVA)

First on our list of ‘Perfect 10’ stocks is Enova International. This alternative online financial services company focuses on providing credit and financial access to small business and consumers who are underserved by the regular banking sector. Since it started operations in 2004, Enova has become a $2.38 billion company in a growing sector of the finance industry and has provided funding for over $61 billion in loans to more than 12 million customers.

Enova uses a world-class, machine learning platform to provide services to its mainly non-prime customer base. The company operates through a network of businesses. On the consumer credit side, these include CashNetUSA and NetCredit in the US market, providing access to installment loans, CAB loans, credit lines, and personal loans. Outside the US, Simplic operates in Brazil and Pangea works in Latin America and Asia. On the small business side of the operations, OnDeck, Headway Capital, and Business Backer provide services customized for the small business community, including term loans and lines of credit, small business loans, and funding solutions for working capital.

All of Enova’s business segments are supported by strong data analytics and machine learning algorithms, allowing the company to tailor its financial services to the specific needs of each customer. In its more than 20 years of operations, the company has collected an impressive database of loan histories and customer behavior, allowing it to fine-tune its machine-learning platform, improving its ability to meet its customers’ needs while ensuring that customers are able to repay loans.

In recent quarters, the company has seen steady growth in both revenues and earnings. Enova last reported its financial results for 1Q25, and in that quarter saw revenue of $746 million and a non-GAAP EPS of $2.98. The top line was up more than 22% year-over-year and beat the forecast by $11.86 million; the bottom line was 22 cents per share better than had been expected. Enova’s credit performance was described as strong during the quarter; the net charge-off ratio was stable at 8.6%, and the consolidated 30+ day delinquency ratio was 7.7%. The company reported total liquidity, including cash, liquid assets, and available credit facility capacity, of $1.1 billion.

For Seaport analyst Bill Ryan, the key points here are Enova’s strong edge in data analytics and its status as a leader in online lending. He writes of the company, “Our Buy rating reflects several factors beginning with the data that has been collected since 2004, which we believe provides the company with a strong competitive advantage, particularly in loan underwriting and generating superior credit performance. Competition is fairly limited and the company’s market share is very small as well, which should allow ENVA to provide controlled growth over the long-term in the sub- and non-prime consumer loan markets, and in its small business lending platform.”

“Enova’s business is highly scalable since it is an online only lender, and variable costs represent over 50% of total expenses. We believe the company’s consumer lending business will prove more resilient in economic downturns which has been a concern for investors recently. This is due to very high margins, manageable credit loss volatility for subprime borrowers based on historical performance, and a more variable cost structure,” Ryan went on to add.

Along with that Buy rating, Ryan gives ENVA a $124 price target that points toward a 33.5% gain in the next 12 months. (To watch Ryan’s track record, click here)

Overall, this lender’s Strong Buy consensus rating is based on 7 recent analyst recommendations, which include 6 to Buy and 1 to Hold. The shares are priced at $92.85 and the average price target, of $126, is slightly more bullish than the Seaport view, suggesting a one-year upside potential of 36%. (See ENVA stock forecast)

Iridium Communications (IRDM)

Next up on our list of ‘Perfect 10s’ is Iridium Communications, a global satellite telecommunications company that offers a range of communications solutions to keep people connected – anywhere on Earth, on land or sea or in the air, from pole to pole. That’s a tall order, but Iridium fills it with a combination of modern tech and skillful applications, offering services ranging from satellite phones to mobile broadband access. The company’s technology and services are used by more than 2.4 million billable subscribers.

Iridium offers a variety of subscription plans, tailored for customers of every sort, at every scale. Plans can be tailored for individual, personal use; for business and organizations; and for governmental and non-governmental organizations. The company bases its service on a constellation of satellites, positioned in low Earth orbit (LEO). By using an LEO configuration for its satellite network, Iridium requires a larger fleet – but can offer stronger signals and faster connections. Iridium’s constellation orbits the planet at altitudes of approximately 485 miles, much closer to the surface than the 22,000-mile-high geostationary orbits used by most competing networks. This allows Iridium to offer its benefits with a fleet of satellites featuring smaller, lower-powered antennas without sacrificing signal clarity and operating at lower costs. Iridium deployed its first satellite in 1997, had the network at full capacity in 1998, and completed a full system upgrade in 2019.

Iridium’s LEO constellation configuration offers one additional benefit. Geostationary satellites orbit over the equator, making coverage at the Earth’s higher latitudes, both north and south, more difficult. This is not an issue with LEO satellites in polar orbits – their normal paths cover the poles and high latitudes, giving Iridium clear coverage across the entire planet.

Iridium’s products and services have found use in a wide range of applications, from adventure travel to ocean communications to remote area exploration to secure government voice links. In addition, Iridium is entering the PNT market – that is, position, navigation, timing – which is essential in providing accurate GPS, mapping, and locator services. Iridium entered the PNT segment last year, through its acquisition of the satellite technology company Satelle.

On the financial side, Iridium reported its 1Q25 results this past April. At the top line, the company had total revenues of $214.9 million, which beat the forecast by over $3 million and translated into 5% year-over-year growth. Iridium’s earnings per share came to 27 cents, or 6 cents per share better than had been expected.

This stock caught the eye of Oppenheimer analyst Tim Horan, who is upbeat about Iridium’s positioning in the LEO satellite service segment. The 5-star analyst says of the company, “In our opinion, the company is not well understood by the Street. Although it will compete with other LEO operators such as Starlink and AST SpaceMobile, IRDM’s service is the only truly global coverage with guaranteed service, and it will now have a unique global PNT service… The company is positioned as the leader in satellite-based global IoT communications, has entered the PNT market through its Satelles acquisition, and has a growing direct-to-device opportunity as new standards are set to support compatibility with unmodified smartphones.”

Horan puts an Outperform (i.e., Buy) rating on this stock, and his $34 price target implies a one-year upside potential of 29%. (To watch Horan’s track record, click here)

The 5 recent analyst reviews of this stock break down 4 to 1 in favor of Buy over Hold, giving IRDM its Strong Buy consensus rating. The shares are priced at $26.34 and their $36 average price target suggests a gain of 36.5% in the year ahead. (See IRDM stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.