If there’s one thing the markets dislike, it is uncertainty, and we have plenty of that right now. Investors remain cautious about both the economic effects of the tariffs on global trade and the probability of a recession.

Claim 30% Off TipRanks

Forget margin or options. Here's how the pros trade WDCIn this environment, investors want to find stocks with solid foundations, shares that stand to gain no matter what the market conditions. The key to finding these stocks lies in the data, the flood of information generated by thousands of traders dealing in thousands of stocks for tens of millions of daily transactions. The sheer volume of data presents an obstacle to stock picking – but the TipRanks Smart Score offers a way to sift through the pebbles, and find the valuable nuggets.

The Smart Score uses an AI-powered algorithm and natural language processing to gather, collate, and sort all of the data generated by the market’s normal activity – and then to use that data to rate every stock against a set of factors that are known to correlate with future outperformance. Each stock is then given a score, a single digit on a 1-to-10 scale, with the ‘Perfect 10s’ denoting the top-scoring shares.

We’ve used the data platform at TipRanks to look up two of these high-scoring stocks that have also earned top marks from the Street’s analysts. Here they are, presented along with some of the analysts’ comments.

Western Digital (WDC)

First up on our list of ‘Perfect 10’ stocks is Western Digital, a major player in the computer memory industry. The company is a leader in the global supply chain for hard disk drives, data center drives, and data center platforms, and also has a significant business in portable drives and network attached storage solutions. The company also produces and markets the cable accessories needed for installations and attachments.

Until this past February, Western Digital was also a major player in the market for flash memory and storage. The company entered the flash market at large-scale in 2016, with its $19 billion acquisition of SanDisk. In February of this year, Western Digital spun off its SanDisk brand. The spin-off was made fully effective on February 24, when SanDisk started trading independently under the SNDK ticker.

Western Digital’s shares dropped sharply in the aftermath, reflecting investor worries that the company will have difficulty maintaining revenues without the lucrative flash memory segment.

A look at the company’s last earnings report, however, shows that the hard disk drive (HDD) business has been accelerating recently, at a much faster pace than flash. The fiscal 2Q25 results showed that Western Digital had total revenues of $4.29 billion; of this total, $2.41 billion came from the HDD side, while $1.88 billion came from flash products. HDD revenues were up 76% year-over-year, compared to the 13% y/y gain in flash.

The company’s total revenue in fiscal Q2 was up 41.6% from fiscal 2Q24, and beat the forecast by $30 million. At the bottom line, Western Digital’s non-GAAP EPS of $1.77, while showing a strong turnaround from the 75-cent EPS loss in the prior-year period, missed the forecast by 5 cents per share.

According to Morgan Stanley analyst Erik Woodring, the company’s success in HDD is the key point to the narrative. He writes of the stock, “WDC benefits from accelerating data growth, which drives storage demand in the cloud and on-prem. We believe that we are still in the middle of the cycle upturn – demand outstrips supply with continued upward pressure in HDD pricing – and entering a period of AI-driven storage demand growth, which will benefit both HDDs and flash shipments. While WDC is behind STX in HAMR timeline, we believe WDC will remain its leading HDD revenue and profits market share in the near term with its competitive UltraSMR solutions for high-capacity drives before the industry shifts to wider adoption of HAMR. We believe the magnitude of the valuation discount vs. STX is overdone with its market share leadership.”

These comments back up Woodring’s Overweight (i.e., Buy) rating on WDC shares, and his $46 price target suggests that the stock will gain 25.5% over the coming year. (To watch Woodring’s track record, click here)

The Morgan Stanley stance is bullish, but the consensus rating on Western Digital is even more so. The stock has a Strong Buy consensus rating, based on 16 recent analyst reviews that include 13 Buys and 3 Holds. The stock is currently priced at $36.68 and its $68.13 average price target implies that it will appreciate by an impressive 86% by this time next year. (See WDC stock forecast)

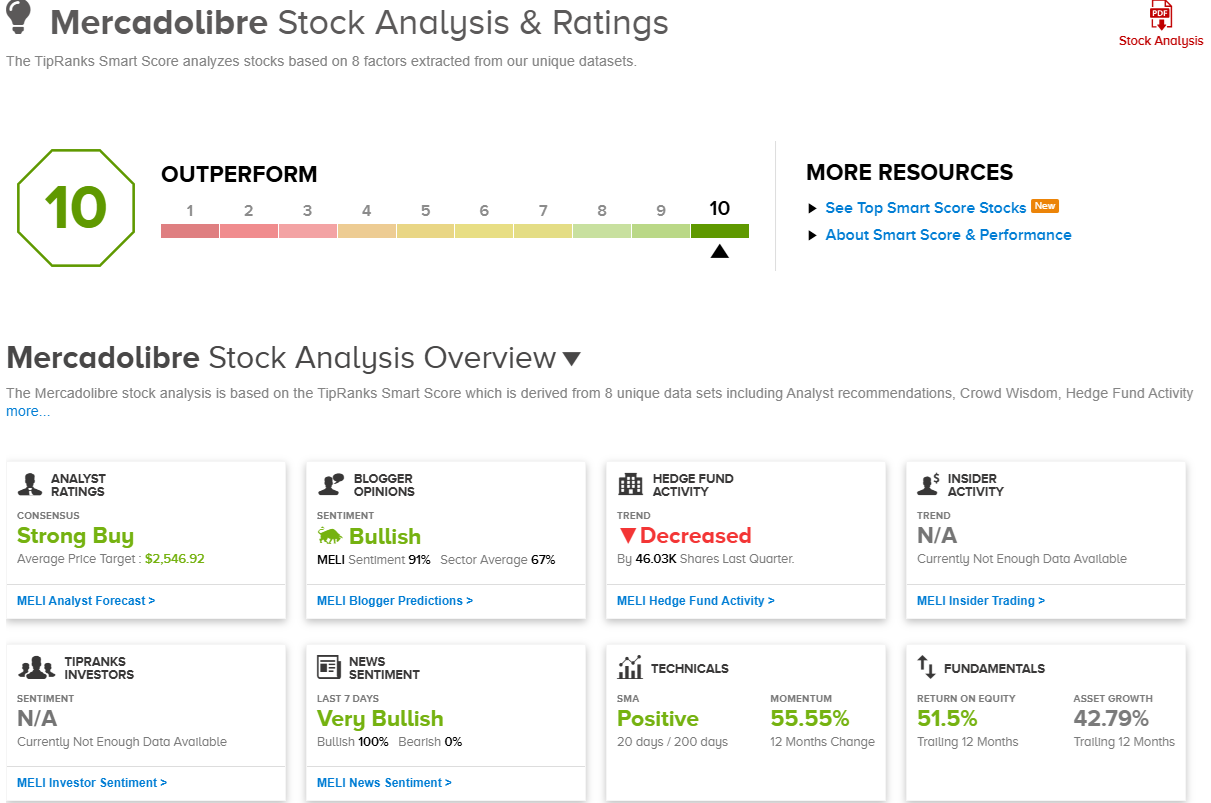

MercadoLibre (MELI)

From memory hardware, we’ll switch gears and look at e-commerce for our second ‘Perfect 10’ performer. MercadoLibre is a $100-plus billion player in this field, and the leading online retail firm in Latin America. The company operates in 18 Latin American countries, including such giants as Brazil, Mexico, and Argentina, as well as smaller countries such as Dominican Republic, El Salvador, and Panama. MercadoLibre’s home region is a potential gold mine for an online retailer, with more than 665 million people and a fast-growing middle class that wants to tap into the global markets.

The company offers services through several divisions, including its core MarketPlace, the online platform that connects buyers and sellers; Mercado Credito, a consumer credit service; Mercado Pago, for online payments; and Mercado Publicado, that focuses on digital advertising. Together, these platforms make MercadoLibre a giant in both e-commerce and fintech, with a market cap of $106 billion and annual revenue, in 2024, of nearly $21 billion.

Zooming in to look at the last reported quarter, 4Q24, we find that MercadoLibre finished its 25th anniversary year with a set of blockbuster financial results. The company’s quarterly revenue of $6.1 billion was up 37.4% year-over-year, and came in $120 million better than had been expected. The bottom line, an EPS of $12.61, was $5.05 ahead of the forecast. The company’s financial results were supported by strong user growth – in Q4, annual unique buyers on the site surpassed 100 million, and the fintech side reported 61 million monthly active users.

In addition to these strong results, MercadoLibre’s stock has been climbing – and even the tariff brouhaha has not derailed the stock’s success. MELI is up 53.2% in the last 12 months, and up 25% for the year-to-date. This is a dramatic outperformance when compared to the NASDAQ’s modest 4% one-year gain and 15.5% year-to-date loss.

This online retailer has caught the attention of Benchmark analyst Fawne Jiang, who is impressed with the company’s proven record of achieving regional dominance. She writes in her recent assumption of coverage, “MELI stands out as a dominant regional leader in the global e-commerce setting, leveraging underpenetrated markets in Latam that are primed for significant growth in both online retail and fintech. With a proven track record of local expertise and knowhow on top of strong execution, we believe that the company offers investors a robust sustainable long-term growth outlook, supported by a diverse range of drivers, making it a unique and highly attractive EM investment candidate.”

Unsurprisingly, Jiang rates MELI as a Buy, and her $2,500 price target points toward a one-year upside potential here of 17.5%. (To watch Jiang’s track record, click here)

Overall, MercadoLibre’s 14 recent analyst reviews include 13 to Buy and 1 to Hold, supporting the Strong Buy consensus rating. The shares are priced at $2,128.33 and have a $2,546.92 average price target that implies an upside of 20% on the one-year time horizon. (See MELI stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.