Market sentiment can shift fast, as seen in recent sessions. The tech rally that had been the driving force behind the past year’s gains appeared to stall earlier this month, but the markets have been in bullish mode once more since the start of the week.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

In an uncertain situation like this, investors need a quality data analysis tool, to make sense of the rapidly changing conditions. The Smart Score, from TipRanks, fits that bill, using AI-powered natural language algorithms to sift through the huge volume of daily trading data, and winnow out the top-scoring stocks. Every stock is compared to a set of factors that have proven reliable as predictors of future performance and given a simple score on a scale of 1 to 10, with the ‘Perfect 10s’ indicating stocks that are primed for gains.

We’ve gotten a start on this, looking at two stocks that have scored the Perfect 10 even amidst market uncertainty. According to the data, each stock also boasts a Strong Buy consensus rating and a double-digit upside. Here are their details, and comments from the Street’s analysts.

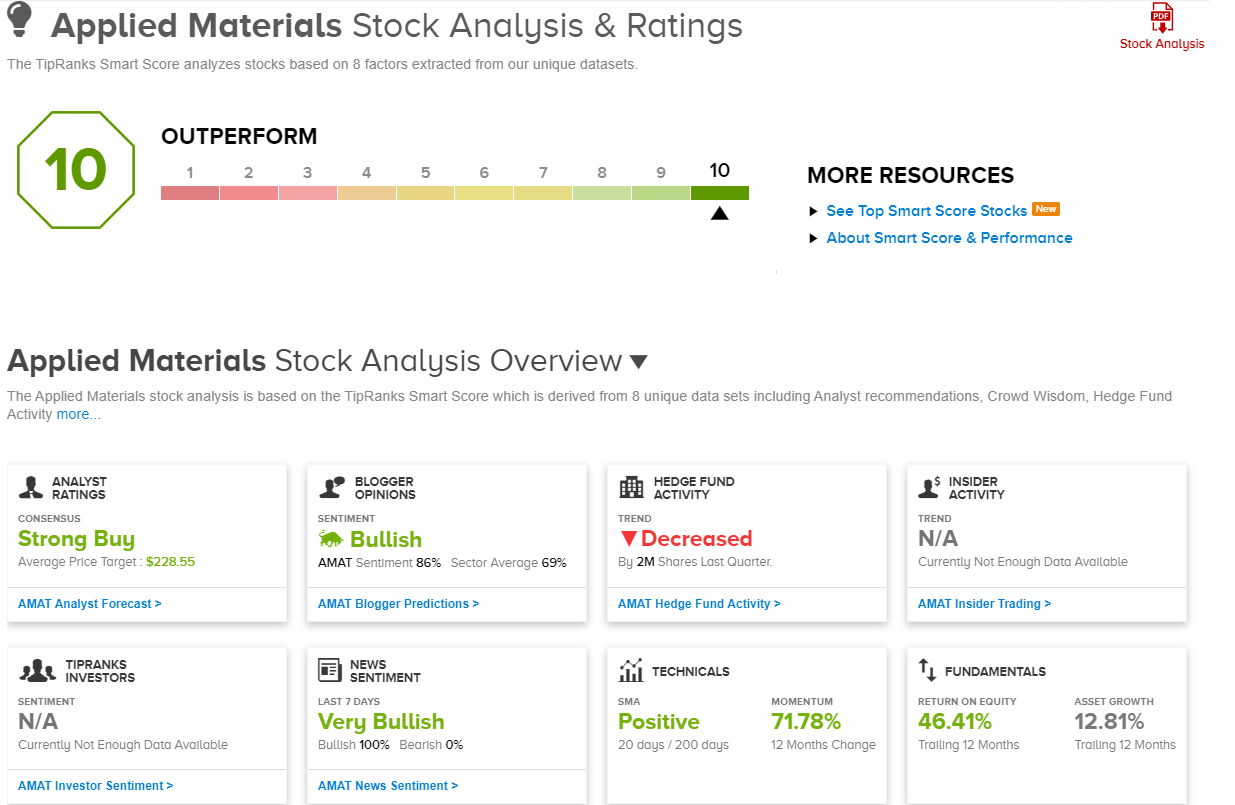

Applied Materials (AMAT)

We’ll start with Applied Materials, a tech company that provides vital support for the semiconductor chip industry, in the form of software and equipment. Applied Materials brings its engineering knowledge to play in high-tech manufacturing, providing solutions for both semiconductor chip companies and flat-screen display manufacturers. The company’s integrated circuit products are used in chip design and are found in a wide range of consumer electronics.

This company works in a high-demand niche, with customers who are willing to pay a premium for quality – and that has been supportive of Applied Materials’ revenue. In the past several years, the quarterly top line has come in consistently between $6 billion and $7 billion, and the company had full-year revenues of $26.52 billion in its last fiscal year, 2023. Applied Materials currently has a market cap of $160.5 billion.

In its last earnings report, for the first quarter of fiscal 2024 (January quarter), Applied Materials had a top-line revenue total of $6.71 billion, relatively flat year-over-year and beating the forecast by $220 million. The company’s earnings, an EPS of $2.13 by non-GAAP measures, was 22 cents better than had been anticipated. The shares trended higher following the release and are up by 19% year-to-date (and 71.5% over the past year) even after a recent pullback over worries China is reducing chip imports.

For Evercore analyst Mark Lipacis, who holds the #6 overall rating from TipRanks, the key point about Applied Materials is the company’s sound position in its industry. The 5-star analyst writes of AMAT, “Being a deposition market share leader, we think AMAT is well positioned to benefit from the SemiCap secular drivers, namely 1) Bigger chips; 2) Complex manufacturing; 3) Trailing Node Buildouts and 4) Semiconductor nationalization. We view AMAT as a particular beneficiary of increased demand for advanced packaging, trailing node demand, and Gate-All-Around and backside power chip architectures.”

Lipacis goes on to put an Outperform (Buy) rating on the shares, with a $260 price target that indicates his confidence in a 34.5% upside for the coming year. (To watch Lipacis’ track record, click here)

This tech stock has picked up 24 recent analyst reviews, with a breakdown of 19 Buys, 4 Holds, and 1 Sell to back up the Strong Buy consensus rating. The shares are priced at $193.24, and their $228.55 average price target suggests a one-year upside potential of 18%. (See AMAT stock forecast)

Trimble Navigation (TRMB)

The next stock on our Perfect 10 list is another tech firm focused on providing the software, hardware, and services needed in high-tech manufacturing. Trimble Navigation works with a wide range of industries, including building and construction, agriculture, government, transportation, utilities, and even specialties like geospatial imaging. The company’s products include items such as inertial navigation systems, global navigation satellite system receivers, aerial drones, laser rangefinders, and software processing tools to put all of this together.

While the company’s background is in hardware, Trimble is shifting more towards services and system maintenance, vital niches in a digital world. The company is developing core technology offerings in positioning, connectivity, and data analytics, all in high demand by globally networked companies, and bills its services as a connection between the digital and physical worlds. Trimble’s solutions aim to improve function for its customers, from productivity to quality to sustainability, while keeping up safety standards.

In an interesting move, Trimble announced on April 1 that it had closed a joint venture transaction with the agricultural giant AGCO. The joint venture is known as PTx Trimble and targets the agriculture technology niche, designed to provide an industry-leading agriculture platform, with precision factory fit and retro-fit applications for farmers globally. Trimble holds a 15% stake in the joint venture.

When we look at Trimble’s last financial release, we see that the company generated $932.4 million at the top line in 4Q23. This was more than $20 million better than the estimates and was up almost 9% year-over-year. Trimble’s bottom line was reported as a non-GAAP earnings-per-share of 63 cents, 3 cents better than the forecast. The company had an annualized recurring revenue (ARR) of $1.98 billion at the end of Q4, a solid metric that bodes well for future business. The ARR was up 24% year-over-year.

This stock caught the attention of analyst Kristen Owen, from Oppenheimer, who notes the solid ARR growth and the company’s strong sales. “Its next phase of growth will be driven by the business model evolution from discrete products to systems solutions, with the ability to sustain a significant portion of ARR growth within its existing customer base,” Owen said. “TRMB is also making it easier for customers to do business with it by realigning its go-to-market from product-based to account-based sales, which we believe can drive bottom-line re-acceleration as sales efficiency improves. We believe TRMB has a long runway of incremental catalysts including closing the AGCO JV, delevering/buybacks, resegmentation, continued portfolio refinement, and its 2H24 investor day.”

All of this supports Owen’s Outperform (i.e. Buy) rating on the stock, and her $72 price target implies that TRMB will appreciate by 20.5% this year. (To watch Owen’s track record, click here)

There are 6 recent analyst reviews on this name, and the 5-to-1 split in favor of Buy over Hold gives the stock a Strong Buy consensus rating. The shares are priced at $57.97 and the $66.80 average price target suggests an upside of 15% on the one-year horizon. (See TRMB stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.