Let’s talk about stock picking. It’s a bit like going to an orchard: if you get there too late, the low-hanging fruit is all gone, and you’ll have to work harder to find the best pieces. Orcharders have ladders and pruning hooks to make the job easier; retail investors can turn to the Smart Score.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

The Smart Score uses a combination of AI and natural language processing, through an algorithm by TipRanks, to gather and collate the mountain of raw data tossed up by the regular daily activity of the stock market – and then it compares every stock to the data, using the collected information and the analysis results to give each stock a simple score.

The score is set on a scale of 1 to 10, and the stock analysis is based on a comparison to a set of factors that are known as sound predictors of future share outperformance. A ‘Perfect 10’ from the Smart Score indicates a stock that is likely to show strong gains going forward.

Then those ‘Perfect 10s’ are also getting love from the Street’s analysts, which is a clear sign of stocks that are sending a bullish signal – and investors should pay attention. So, let’s do that; here are the details of 3 stocks that have earned the ‘Perfect 10,’ and have recent Buy ratings from the professional stock watchers.

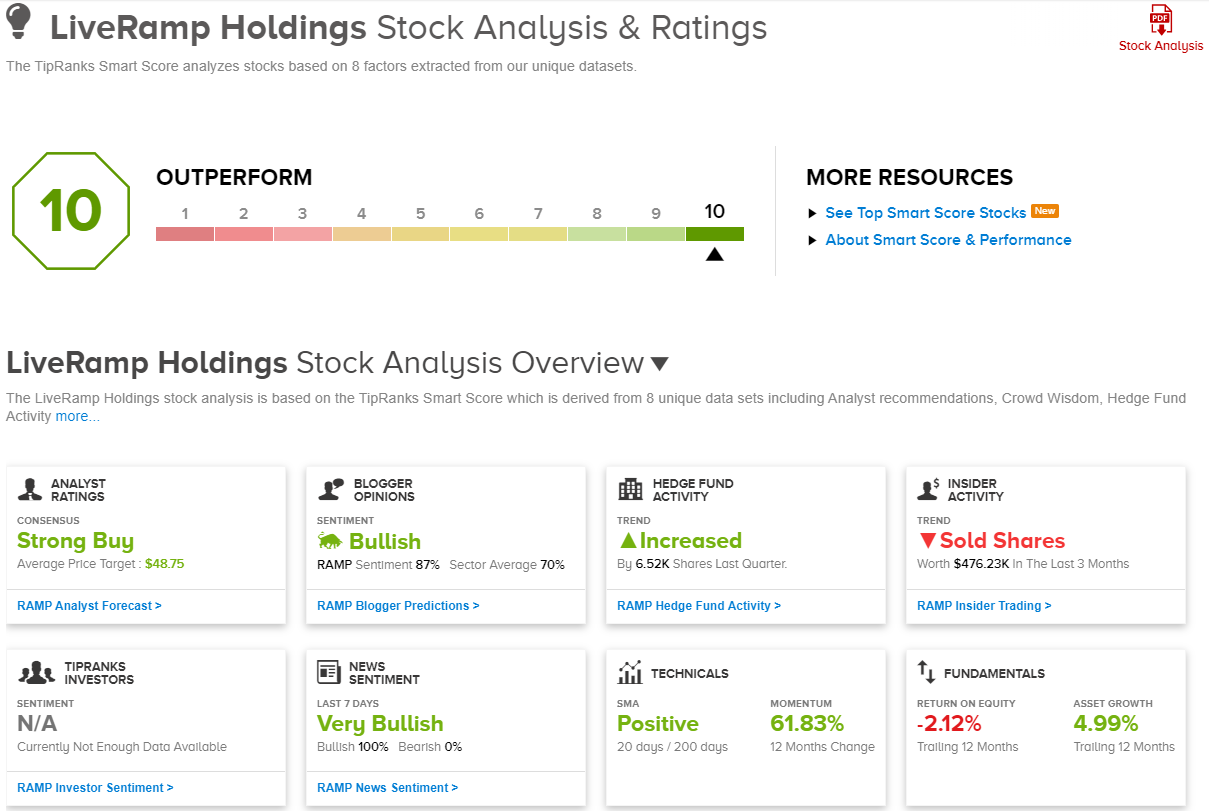

LiveRamp Holdings (RAMP)

The first stock on our list is LiveRamp, a tech firm based in San Francisco and excelling in data enablement. LiveRamp’s platform allows its enterprise customer base to make their data accessible, usable, and secure; in short, the company offers data solutions that are customizable and scalable. It’s a necessary niche, and has found acceptance from numerous big-name firms. LiveRamp’s customers include such giants as Google, Walmart, Marriott, Hulu, and Office Depot.

At the user level, LiveRamp gives its customers a platform capable of connecting devices and people with data across the digital and real worlds. The result: faster integration, more efficient workspaces, and improvements in digital security.

The company’s strong product has led to some solid business numbers. LiveRamp reported 895 direct subscription customers at the end of fiscal 3Q24 – the quarter ending on December 31, 2023 – and of those, 105 have subscription contracts worth $1 million or more in annual revenue. The company’s total subscription revenue for the quarter was up by 5% year-over-year, reaching $132 million.

This was one part of the company’s total revenue for the quarter, which came to $174 million, representing a 10% year-over-year gain and exceeding the forecast by $2.15 million. The company realized a 29% year-over-year increase in ‘marketing and other’ revenue, reaching $42 million in the period. At the bottom line, LiveRamp’s non-GAAP earnings per share were 47 cents, 7 cents better than had been expected. Looking at the company’s share performance, we see that RAMP has risen by more than 58% over the past 12 months, but has been slipping since the early-February earnings release and is down more than 10% year-to-date.

For Evercore analyst Kirk Materne, this stock represents a turnaround story after some recent slowdowns. He writes of the company and its shares, “We continue to believe that following a material (largely macro-induced) slowdown in growth in 2023, the company is well positioned to reaccelerate growth in 2024 (FY25) and beyond as the digital ad environment continues to improve, and LiveRamp benefits from being able to deliver identity, activation, addressability, and measurement at scale. The acquisition of Habu (announced in January) rounds out the ‘clean room’ capabilities of the company, adding increased integrations with the public cloud providers (namely Azure and Databricks with the addition of Habu) as well as expanding measurability in ‘walled gardens’, which account for ~3/4 of non-search digital advertising.”

Looking ahead, the analyst adds some explanation on just why he thinks these shares are going to climb higher, saying, “Finally, the company is working towards a ‘rule of 40’ operating profile, expanding operating margins by ~500bps in FY24 (as of the most recent guide) and expects similar expansion in FY25. The company’s margin expansion is further augmented by share repurchases ($60-80mn expected in FY24). Given these improving fundamental factors and solid initial F3Q (Dec.) results, we view the current valuation of ~3x EV/CY25 as leaving some room for upside.”

For Materne, this all adds up to an Outperform (Buy) rating, and his $50 price target implies the shares will gain 49% in the 12 months ahead. (To watch Materne’s track record, click here)

Overall, LiveRamp holds a Strong Buy consensus rating, based on 6 unanimously positive analyst reviews. The shares are trading for $33.50 and their $48.75 average price target suggests an upside of 45.5% on the one-year horizon. (See LiveRamp stock forecast)

BridgeBio Pharma (BBIO)

For the second stock on our list, we’ll shift over to the biomedical research field, where BridgeBio Pharma focuses on developing new treatments for genetic diseases with clear genetic drivers. These are conditions that are known to be genetically linked – and known to be caused by a single genetic mutation for each disease. Per BridgeBio, there are more than 8,000 disease conditions that meet this description, affecting millions of patients. That’s a huge potential customer base for a biopharmaceutical researcher, especially when we realize that there are fewer than 50 therapeutic agents approved by the FDA in this area.

BridgeBio is working to expand this area of treatment and has more than 15 active research tracks in its pipeline, targeting more than 20 disease conditions. The most advanced drug candidate, acoramidis, is a potential treatment for transthyretin amyloid cardiomyopathy (ATTR-CM). The company’s new drug application (NDA) for this candidate has been accepted for review by the FDA, with the PDUFA date set for November 29, 2024. In addition, the European Medicines Agency has also accepted the company’s MAA (Marketing Authorization Application) for acoramidis.

The company has also recently released data from the Japanese Phase 3 human clinical trial of the drug. The study, which focused on Japanese ATTR-CM patients, showed positive results – particularly, no patient mortality over a 30-month period.

BridgeBio generates most of its revenue through licensing agreements. That revenue track is facing pressure due to an ongoing legal suit involving Pfizer. Pfizer is undertaking a defense of its own ATTR-CM drug against generic copies; if Pfizer is successful, it will protect its intellectual property – and open up the field to BridgeBio, which will then face reduced competition.

When we look at the analysts, we find Danielle Brill, of Raymond James, taking a bullish stance on this company, based mainly on the strength of acoramidis. She writes, “We believe oral TTR-stabilizers (BBIO’s acoramidis/ PFE’s tafamidis) will remain as the gold-standard first-line therapy for patients with ATTR-CM. While there was some concern that the silencers (i.e., ALNY’s vutrisiran) might have a strong case for use ahead of the stabilizers, that now seems highly unlikely given the recent setback and change of stats plans for ALNY’s Ph 3 HELIOS-B trial.”

Brill sees the IP lawsuits as a potential booster, too, and also outlines the financial potential of the ATTR-CM market for BridgeBio: “There is still an IP overhang on BBIO, as PFE continues to litigate with generic filers — but we are cautiously optimistic that PFE’s patent estate will be protected until 2035. As the lawsuit progresses, there have been positive signs that PFE will be successful in defending their IP. If PFE’s patent holds, we think BBIO could capture ~20% of the projected $15B TAM, which translates to ~$3B in peak sales. Given the uncertainty, our model reflects risk adjusted peak net sales of ~$1.6B.”

The bottom line for Brill is an Outperform (Buy) rating on the shares, along with a price target of $45 that indicates her confidence in a 51% one-year upside potential. (To watch Brill’s track record, click here)

The Strong Buy consensus rating on BBIO shares is based on 12 recent analyst reviews, including 11 Buys and 1 Hold. The average price target, $50.73, and the $29.76 trading price, together suggest a 12-month gain of 70.5%. (See BBIO stock forecast)

IDEAYA Biosciences (IDYA)

We’ll wrap up with another biotech company in the biopharmaceutical field. IDEAYA is a precision medicine company, with a pipeline of drug candidates that have the potential to become first-in-class or best-in-class therapeutic agents. The company’s pipeline is made up of small molecule compounds and targets various cancers. IDEAYA uses molecular diagnosis methods to screen its patient populations, allowing for the fine targeting of synthetic therapeutic agents tested in clinical trials.

The most advanced products in those clinical trials are darovasertip, also called IDE196. It is a PKS inhibitor targeting genetically-defined cancers based on GNAQ or GNA11 mutations. IDE397 has wide applications as it is an MAT2A inhibitor, targeting cancer tumors that include an MTAP gene deletion – a class that includes some 15% of solid tumors. Finally, IDE161 is a PARG inhibitor being studied for efficacy against tumors with HRD, or homologous recombination deficiency.

Darovasertip is the subject of multiple clinical trials, with the most recent positive results coming from its trial as a combo therapy with crizotinib. In this trial, it showed ‘evidence of superior clinical efficacy in any-line and first-line MUM (metastatic uveal melanoma) patients compared to standard of care.’ The company has recently expanded its Phase 2 trial of darovasertip in combo with crizotinib against GNAQ/11 metastatic cutaneous melanoma. On the IDE397 track, the company has set up a collaboration with Gilead to study the IDE397-trodelvy combo in a clinical study for the treatment of MTAP bladder cancer.

The company’s most recent development was the announcement earlier this month of a clinical collaboration with Merck to evaluate IDE161 in combination with Keytruda as a treatment for patients with MSI-high and MSS endometrial cancer. IDEAYA will sponsor the clinical trials based on this collaboration.

This stock caught the eye of Justin Zelin, a 5-star analyst from BTIG. Zelin is bullish on IDYA’s high-quality pipeline, and writes of the company, “Lead drug daroversitib has demonstrated encouraging clinical data in the untapped HLA-A2(-) uveal melanoma pt population, who are ineligible for tx with Immunocore’s KIMMTRAK. We view positively IDYA’s MAT2A program, IDE397, as having a differentiated approach towards MTAP-deleted tumors, and we will keenly follow synergistic data from the PRMT5i combination program, which we believe could potentially be best-in-class. We believe the early pipeline is underappreciated and see value-creation opportunities on the generation of additional de-risking POC data for IDE161 and Werner helicase programs.”

Quantifying his stance, Zelin rates the stock as a Buy, with a $55 price target implying a 29% increase in share price in the coming year. (To watch Zelin’s track record, click here)

This is a stock with a unanimously positive Strong Buy consensus rating, based on 10 analyst reviews. The shares are trading for $42.51 and their $52.90 average target price points toward a 24.5% upside potential over the next year. (See IDYA stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.