To buy and sell stocks successfully means you have to find and read the bullish signals – and that in turn means you have to know the signals to read. It’s not really a trick, though, since everything a stock investor needs to know is wrapped up in the accumulated data of the stock markets.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

That accumulated data, however, presents an imposing roadblock. It’s the aggregated data from thousands of investors trading thousands of stocks, making millions of transactions every day. The Wall Street professionals, who build their careers watching individual stocks and sectors, have years to spend learning the ins and outs of the market data; for the average investor, there’s the TipRanks Smart Score.

The Smart Score is a data collection and collation tool, based on a sophisticated AI algorithm, using natural language processing to gather all the data from the markets – and to use it to rate every stock according to a set of factors that are known by past results to successfully predict future outperformance.

Based on that comparison, every stock is given a simple score, on a scale of 1 to 10, with a ‘Perfect 10’ indicating a stock that has all of the signals lined up right.

We’ve used the TipRanks database to pull up a couple of those ‘Perfect 10s,’ stocks that the analysts see as sending bullish signals. Here are the details, along with comments from some of the Street’s stock analysts.

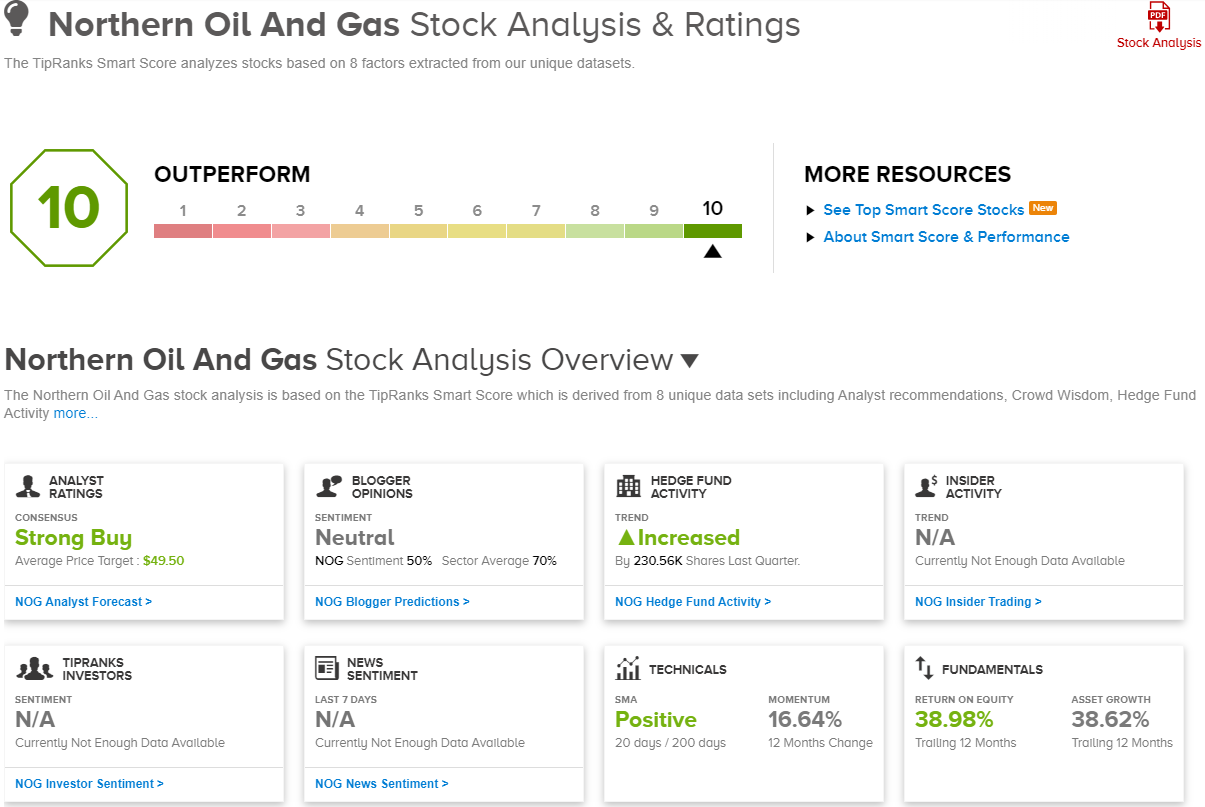

Northern Oil and Gas (NOG)

The first name on our list is Northern Oil and Gas, one of the US energy industry’s independent companies. Northern’s operations include the acquisition of land holdings in hydrocarbon-rich regions; the exploration of those holdings; the development and exploitation of recoverable energy reserves; and the production of usable crude oil and natural gas. Northern owns over 300,000 acres in major energy areas such as the Williston Basin, the Permian Basin, and the Marcellus Shale of Appalachia.

Northern’s portfolio is based around high-quality land holdings with a low breakeven price and nearly 10,000 wells. Northern does not operate the wells itself; rather, the company owns the lands and the resources underneath and controls the wells, which in turn are operated by more than 100 third-party actors, both public and private. The largest share of Northern’s holdings is in the Williston Basin, approximately 178,200 acres, while the gas-rich Appalachian holdings total some 54,200 acres, and the Permian holdings come to nearly 40,000 acres. The Permian Basin holdings generate some 45% of NOG’s production, while the Williston accounts for 41%. Production in the Appalachian region accounts for 14% of the company’s production. The lack of correlation between the size of a regional holding and its contribution to Northern’s total production reflects, in part, the relative density of the energy reserves in these areas. Crude oil makes up 59% of Northern’s output, and natural gas makes up 41%.

In the first quarter of 2024, Northern reported a company record in quarterly production, generating 119,436 Boe per day and realizing $396.3 million in total revenues. However, this figure was down almost 32% year-over-year and missed the forecast by $109.7 million. The company’s quarterly earnings looked better, with the non-GAAP EPS coming in at $1.28 per share and beating the forecast by 11 cents and, based on an adjusted net income of $130.5 million.

Looking at the company’s prospects, Bank of America analyst Noah Hungness likes the potential for future expansion. He writes, “In our view, NOG is well positioned as the largest public non-op company to participate in large future M&A. NOG’s ability to leverage its first mover advantage that built a ~120 mboed public non-op oil and gas company will not be replicated over the next few years and is in a unique space to work with operators to complete larger deals that we expect may come from aftershocks of the historic wave of M&A we saw last year.”

These comments back up Hungness’s Buy rating on Northern Oil and Gas, while his $48 price target suggests the shares will gain 29% on the one-year horizon. (To watch Hungness’s track record, click here)

This stock’s Strong Buy consensus rating is based on 11 recent reviews that include 9 to Buy and 2 to Hold. The shares are currently trading for $37.26 and their $49.50 average target price implies a one-year upside potential of 33%. (See NOG stock forecast)

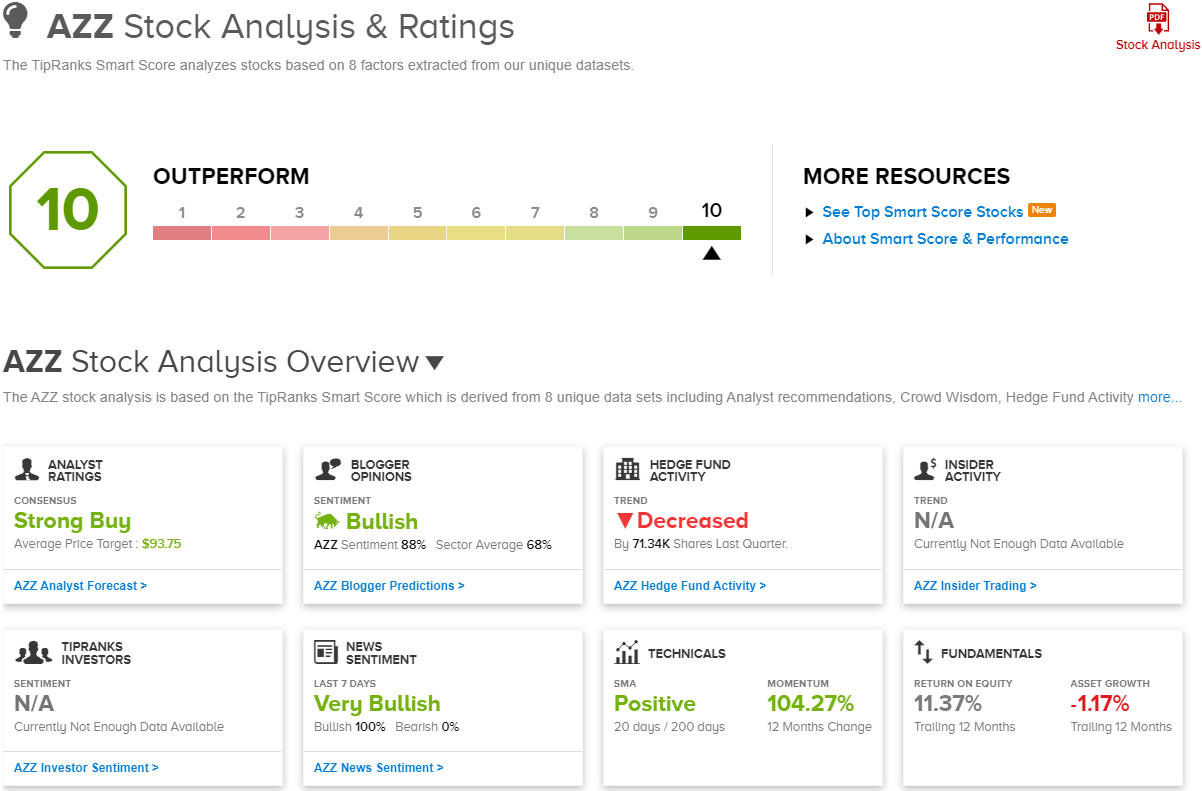

AZZ, Inc. (AZZ)

There are so many different products in our day-to-day lives, machinery, and tools, that it’s easy to take them for granted – and it’s easier to overlook just how wondrous the technology behind them is. Take metals, for example: the basic material for most appliances and tools in your home. Most metal products would rapidly corrode just from the oxygen in the atmosphere if it weren’t for the various coating technologies exemplified by AZZ.

This company is a leading provider of industrial coating tech, providing the protective coatings and technologies that make metals viable on most of our world’s basic tools, from home appliances to factory floor machine tools. AZZ is the leading provider for hot-dip galvanizing technology in North America, a technique whereby steel or iron items are dipped in molten zinc in order to form an alloy surface layer that prevents corrosion and extends the metal’s life. In addition, AZZ is also a major provider of precoat metals for coil-coated metal solutions, another cost-effective technology to give metal surfaces enhanced weather and corrosion resistance.

AZZ’s fiscal year 2024 ended this past February 29, and in April, the company reported its fiscal 4Q24 results. The earnings release showed a quarterly top line of $366.5 million, up almost 9% from the prior year and more than $15 million ahead of the estimates. The company’s fourth-quarter bottom line was reported as a non-GAAP EPS of 93 cents; this was up from just 30 cents in fiscal 4Q23, and was 23 cents better than had been anticipated. The company’s sound results were driven by a 13.4% y/y increase in precoat metals sales, which hit $212.1 million. Metals coatings sales were up 3.3% y/y.

This stock has caught the attention of Jefferies analyst Laurence Alexander, who notes that increases in on-shore manufacturing are benefiting AZZ through a ripple effect. “As the largest independent North American provider of metal coatings, AZZ benefits from strong secular trends in favor of reshoring and infrastructure upgrades and a cyclical recovery in metals demand,” Alexander said. “Growth >GDP, >20% margins and >$5/share avg. FCF before dividends should support significant multiple expansion, in our view–and a path to double by 2026.”

The analyst goes on to give AZZ shares a Buy rating with a $105 price target that points toward a one-year potential gain of 33%. (To watch Alexander’s track record, click here)

While there are only 4 recent analyst reviews on this stock, they all agree that it is one to Buy – making the Strong Buy consensus rating unanimous. The shares are priced at $79.12 and the $93.75 average target price suggests an 18.5% upside in the next 12 months. (See AZZ stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.