If there’s one thing that the ongoing wars in Ukraine and the Middle East can show us, it’s that the techniques and tools of warfare are changing. While Napoleon’s ‘big battalions’ still have an advantage, Stalin’s ‘quantity over quality’ no longer holds. The armies of tomorrow will need the best weapons and the best technology, and plenty of both.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

That shift is already underway, according to Stifel analyst Jonathan Siegmann, who sees the defense sector approaching a pivotal transformation.

“We believe the defense industry is at the start of a period of considerable change,” Siegmann opined. “Credible US deterrence is dependent on affordably evolving our weapon systems, recapitalizing the defense industrial base, and transforming government contracting. The defense industry of tomorrow will be faster moving, more fragmented, and less dependent on centralized planning. There is bipartisan political and industry support for transforming the acquisition process. While prior reforms have been underwhelming, we expect the geopolitical environment, outside capital, and the disruptive administration to catalyze greater changes today.”

Looking ahead, Siegmann sees clear winners emerging, noting: “We believe equity markets will increasingly reward the companies that can profitably invest in the growing areas of defense. We believe low-cost mass production, asymmetric weapons, software-enabled capabilities, and on-shoring will be the key differentiators.”

These points lead Siegmann to select three defense stocks as his top picks right now. He’s far from the only analyst positive on these names; according to the TipRanks data platform, Wall Street is bullish on all three. Here are the details.

CACI International (CACI)

First on our list is CACI International, one of the multitude of information and technology contracting firms that operate in the Beltway region of Maryland and Northern Virginia, surrounding Washington DC. CACI is based in Reston, a Virginia suburb that is well known as a home for many contractors with close ties to the Federal establishment – and CACI is exactly that. The company’s work is wide-ranging; CACI provides expertise in the tech and national security fields, and especially in technology applicable to national security. The company works with a multitude of government agencies and is well known for its connections with the Department of Defense, the Department of Homeland Security, and the various Intelligence Community entities.

As for actual services, CACI provides a variety of solutions in enterprise IT, cybersecurity, military mission support, applied engineering, and data management. CACI is even known as a provider of mission operations support for the space program. CACI is capable of providing outsourced services in everything from HR to financial oversight to supply chain management, and can act as an independent watchdog for government departments.

CACI has also developed expertise in AI, taking advantage of the AI boom to develop new services for its clientele. The company is recognized as a leader in the application of AI and deep learning to the defense industry, and has proven able to meet rapidly evolving needs in a cost-effective manner.

This company’s last set of financial results covered fiscal 3Q25 (March quarter). CACI reported $2.17 billion at the top line in the quarter, beating the forecast by over $36 million and growing 16% year-over-year. The $6.23 non-GAAP EPS was 63 cents per share better than had been anticipated. The company generated $187.9 million in free cash flow, up 84% year-over-year. The company reported a work backlog of $31.4 billion as of March 31, up 9.8% y/y.

That backlog presents the starting point for Siegmann’s coverage of this stock. As he writes, “CACI International’s focused bidding strategy has built a high-quality backlog which we believe can sustain MSD% growth and higher margins. CACI’s acquisition strategy is consistent and well-executed. We expect CACI to continue executing M&A transactions and increase their exposure to new defense tech areas. Our Buy rating reflects CACI’s premium valuation being justified through its ongoing financial outperformance, growing exposure to growth vectors in new defense, and strong M&A history.”

Siegmann backs up that Buy rating with a price target of $576, a figure that points toward an upside of 24% on the one-year horizon.

The Strong Buy consensus rating here is based on 10 analyst reviews, with a 9 to 1 split favoring Buy over Hold. The shares are currently trading for $465.37, and they have an average price target of $536.25, implying a 15% upside by this time next year. (See CACI stock forecast)

Teledyne Technologies (TDY)

Next on our list of Stifel defense picks is Teledyne Technologies, a company that is more than just a defense firm. Teledyne acts as a technology and service provider across a wide range of industries, including defense and aerospace, but also including such industrial essentials as factory automation, environmental monitoring, electronics design, deepwater oil and gas exploration, and even medical imaging and pharmaceutical research.

Teledyne offers its customers a large variety of practical products, from digital imaging sensors and cameras capable of working in visible, infrared, and X-ray light spectra, to marine monitoring and control instrumentation, to aircraft information management systems, to more defense-oriented electronics and satellite communication subsystems. The company also develops and provides precision-engineered systems on order for the defense, space, environmental, and energy sectors.

The company provides these products and services through four business divisions: instrumentation, digital imaging, aerospace & defense electronics, and engineered systems. Together, these divisions brought the company $1.45 billion in revenue during 1Q25, up 7.4% year-over-year and some $10 million above the forecast. The firm’s non-GAAP EPS came to $4.95, 3 cents per share better than had been estimated.

Checking in with Stifel’s Jonathan Siegmann again, we find the analyst upbeat about this company’s fundamentally sound position. Siegmann writes of the stock, “Teledyne is an attractive portfolio of niche digital imaging, instrumentation, and aerospace & defense businesses unified by specialized advanced technology, high barriers to entry, and high reliability products. Teledyne’s longer-cycle businesses (anchored by defense) are currently due to accelerate from their substantial backlog increase at the same time as their shorter-cycle businesses are stabilizing and poised to return to growth. Margins are expected to further expand from operational improvements and mix.”

This name gets a Buy rating from Siegmann, whose $626 price target suggests the shares have an upside potential of 23.5% over the next 12 months.

While Teledyne only has 5 recent analyst reviews, they are all positive – making the Strong Buy consensus rating unanimous. The shares have a trading price of $506.67 and an average target price of $576.20, together indicating room for a 14% upside for the stock this coming year. (See TDY stock forecast)

AeroVironment (AVAV)

We’ll finish in the world of applied robotics, a field that has found plenty of practical applications in the world’s military establishments. AeroVironment is a well-known developer and manufacturer of drones – unmanned aerial vehicles (UAVs) and uncrewed aircraft systems (UASs) in more technical jargon – and also produces several lines of unmanned ground vehicles (UGVs) and high-altitude pseudo-satellites (HAPS). These vehicles, whether autonomous or remote-operated, are designed to provide military users with strong reconnaissance capabilities, while loitering munition systems (LMSs) can provide offensive and defensive fire support over the battlefield.

The key to this company’s success is its focus on providing ‘solutions that work,’ with battle-tested vehicle designs capable of meeting battlefield needs on land, sea, and air. The company understands that military applications have no margin for error, and that every system must work right the first time; this understanding lies behind AeroVironment’s commitment to high quality at every stage of product development and testing, from putting together prototypes to marketing field-deployable systems.

In recent weeks, AeroVironment has announced several new contracts, in line with the company’s constant push to maintain and expand its business. In mid-May, the company landed a new contract with the Netherlands to modernize that country’s fleet of Puma UAS vehicles. Also in May, AeroVironment received a $5.1 million contract from the US Army to use the company’s Tomahawk Grip TA5 as a dismounted common controller for human-machine teams. And in mid-June, AeroVironment and Denmark entered into an agreement to expand allied UAS systems in Europe.

Perhaps most importantly, on May 1, AeroVironment completed its $4.1 billion merger with BlueHalo. This move expanded the company’s portfolio and its ability to deliver proven unmanned vehicle systems across all realms.

Earlier this week, AeroVironment released its financial results for fiscal 4Q25 as well as the full fiscal year 2025. For the quarter, the company’s revenue came to $275 million, up almost 40% and described by the company as ‘record fourth quarter revenue.’ At the bottom line, AeroVironment’s non-GAAP EPS of $1.61 was up from $0.43 in fiscal 4Q24. For the full year, the company reported revenue of $821 million, up 14% from fiscal 2024. The stock surged following the readout, bringing AVAV’s year-to-date gains to 77%.

In his coverage for Stifel, Siegmann lays out the reasons to get behind this firm. He writes, “AeroVironment is a leader in several key areas in new defense, namely loitering munitions (Switchblade family of drones) that we believe will be critical as the entire industry undergoes a transformation. The company’s recent merger with BlueHalo provides exposure in space, counter-drone, and missiles, all of which are priorities for the DoD. We anticipate a steep ramp in organic EBITDA in the legacy AVAV portfolio and BlueHalo. Our Buy rating reflects AeroVironment’s positioning as a pure-play new defense tech company with rapidly growing sales and earnings driving increased investor enthusiasm and multiple expansion.”

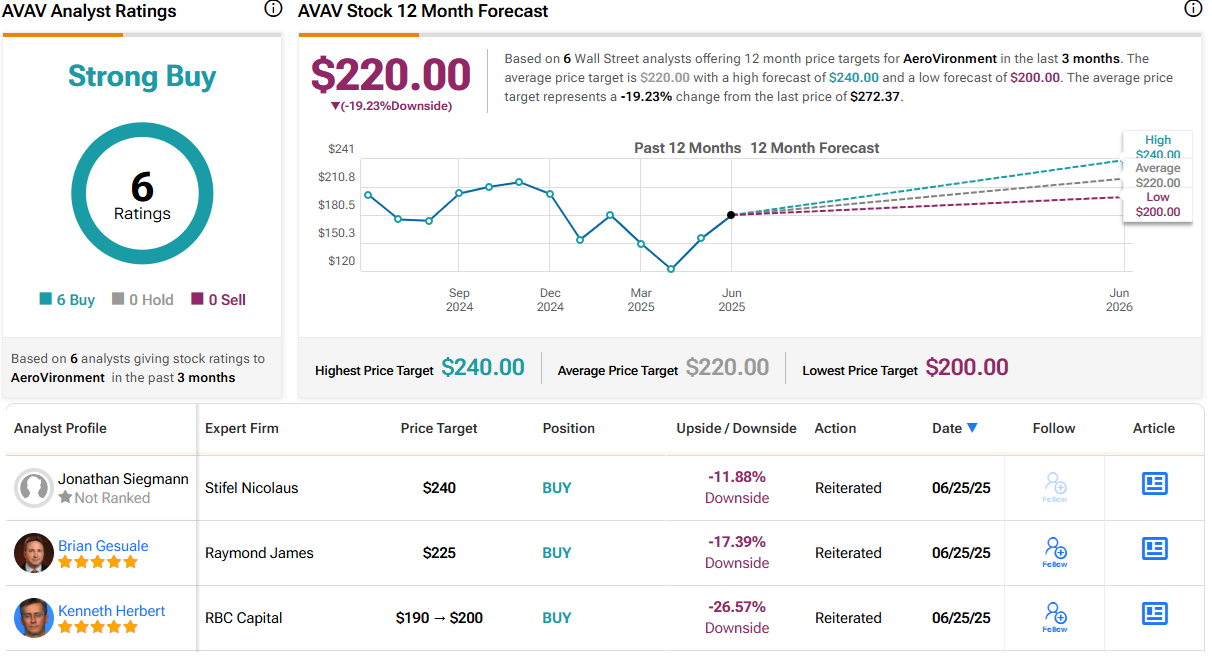

Along with the noted Buy rating, Siegmann puts a $240 price target on this stock, although the recent uptick has taken the stock well beyond that figure.

The Wall Street consensus on AVAV is a unanimous Strong Buy, based on 6 recent positive analyst reviews. However, the gains have taken the shares 19% above the $220 average price target. It will be interesting to see whether analysts increase their price targets or lower their ratings shortly. (See AVAV stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.