One thing is for sure, 2020 threw the world into a tailspin. The spread of COVID-19 devastated the economy, and took investors on a rollercoaster ride that featured massive amounts of volatility packed into a span of only a few months.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Investors saw stocks take a fast and frightening nose dive, only to be followed up by a fierce V-shaped rebound. Against this backdrop, U.S. 10-year and 30-year bond yields plummeted to all-time lows and unemployment levels clocked in at alarming highs.

Still, despite all of the chaos, a select few retail names have stolen the show, delivering applause-worthy performances.

With this in mind, we used TipRanks’ database to identify three retail stocks that have earned a “Strong Buy” consensus rating from the analyst community. Let’s take a look.

Carter’s (CRI)

First in line is Carter’s, a company whose name is synonymous with childrenswear. The company’s brands include Carter’s, OshKosh, Skip Hop, Child of Mine, to name a few, and it operates three segments: U.S. Retail (1,100 retail stores), U.S. Wholesale (18,000 locations) and International.

Carter’s second quarter operating results were negatively impacted by the COVID-19 pandemic. Retail stores were closed for much of the quarter and sales to wholesale customers declined. Overall, sales fell 29.9% to $219.5 million, while adjusted earnings per share dropped 43% to $0.54. A bright spot in the quarter was online sales, which jumped an impressive 101%.

Despite the poor quarter and lingering effects of COVID-19, B.Riley FBR analyst Susan Anderson, believes the company is well positioned, pointing out the name has rebounded 24% since March 23. “The bright spot is that CRI is not exposed as much to BTS (back to school) relative to competitors and 50% of sales come from the baby category, which is not impacted by an anticipated weaker BTS season,” she commented.

On top of that, the B.Riley FBR analyst considers Carter’s to be the best of the bunch, stating, “…we continue to believe CRI is the premier children’s apparel retailer and manufacturer that will be able to come out of the COVID-19 pandemic on stronger footing as other children’s retailers struggle.”

Anderson rates the stock a Buy, writing, “CRI’s high e-commerce penetration, growth initiatives, and cost-reduction measures make CRI a strong buy.” She has a $103 price target on the stock, which adds up to a potential rise of 27% from the current share price. (To watch Anderson’s track record, click here)

Similarly, most of the Street is on board. 3 Buys and only 1 Hold assigned in the last three months add up to a Strong Buy analyst consensus. In addition, the $101.25 average price target puts the potential upside at 25%. (See Carter’s stock analysis on TipRanks)

Callaway Golf Company (ELY)

Next in line is Callaway Golf Company, a leading manufacturer of golf clubs and related products under the Callaway, Jack Wolfskin, OGIO and TravisMathew brands. The company sells its products through golf and sporting goods retailers as well as mass merchants.

Callaway experienced a strong sales rebound in June, with sales rising by 8% compared to June 2019. Still, the overall second quarter operating performance was poor due to COVID-19. Revenue fell 34% to $297 million, while adjusted earnings plummeted 84% to $0.06 per share.

Writing for Raymond James, five-star analyst Joseph Altobello notes while earnings reflected “meaningful near-term disruption from COVID-19,” the results “exceeded expectations on the top and bottom lines.” Also, “recent trends look encouraging,” in the analyst’s opinion.

The stock has mostly recovered from a massive plunge earlier in the year, and is up a whopping 283% since March 18. Altobello is enthusiastic about Callaway’s prospects going forward. “The sport of golf has been somewhat insulated from COVID-19 headwinds given the ability of players to easily maintain social distancing. We anticipate further improvement over the balance of the summer, and with retail essentially open for business, the outlook for equipment manufacturers such as Callaway is much more favorable, while apparel trends are improving as well (albeit to a lesser degree),” he explained.

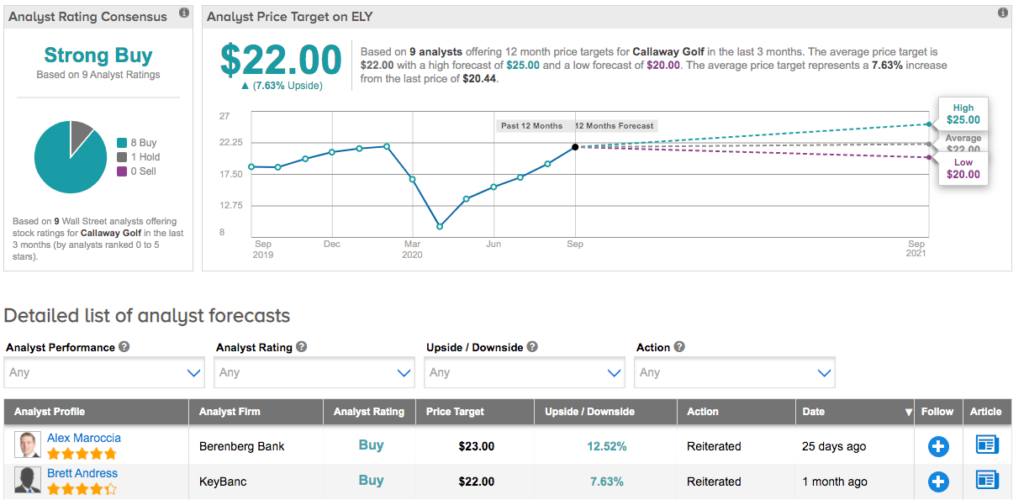

Accordingly, Altobello rates Callaway an Outperform (i.e Buy) and puts a $22 price target on the stock, which means there’s upside potential of 8%. (To watch Altobello’s track record, click here)

Overall, the company gets a Strong Buy consensus rating from the analyst community with 8 Buy ratings and only 1 Hold. The average price target matches Altobello’s. (See Callaway stock analysis on TipRanks)

Canada Goose Holdings Inc. (GOOS)

Rounding out our list is Canada Goose, which is known for its red, white and blue patch. It manufactures premium outerwear such as parkas, down jackets, rainwear and knitwear.

Canada Goose has taken a heavy hit from the COVID-19 pandemic. Sales and earnings per share in the most recent quarter sank 63% and 66%, respectively, though they were basically in line with expectations.

Management has taken steps to ease the pain by improving inventory management and realigning its cost structure. In addition, with online sales rising sharply, the company has increased investments to support the demand. Wells Fargo analyst Ike Boruchow weighed in on the initiatives, stating, “GOOS can weather the storm…Looking ahead, favorable seasonality limits headwinds in 1H and the focus is on improvements in the key holiday quarter.”

So, where does the company go from here? The Wells Fargo analyst is of the opinion that the brand has staying power, noting that it has bounced back by 69% since March 16. “Canada Goose is a heritage brand rooted by the “made in Canada” identity and family-run origins. This authenticity appeals to a range of customers across the fashion luxury and recreational outdoor spaces, providing a broad addressable market, which we believe remains still largely untapped given the sales base of their much-larger competitors,” he said.

What’s more, Boruchow believes there are still significant untapped opportunities for growth. Expounding on this, he commented, “When looking at GOOS across the spectrum of other outerwear brands (both mid-tier and luxury) it appears that the brand still has runway for growth as they begin to push ancillary channels, categories and geographies.”

Based on the above, Boruchow has an Overweight (i.e Buy) rating on GOOS. The price target of US$34.45 (C$45) represents substantial potential returns of 37%. (To watch Boruchow’s track record, click here)

What does the rest of the Street say? The bulls win with an overwhelming majority. 7 Buys and only 1 Hold translate to a Strong Buy consensus rating from the analyst community. The average price target of US$30.37 (C$39.79) is not as bullish as Boruchow’s, but still offers a significant potential return of 21%. (See Canada Goose stock analysis on TipRanks)

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.