What kind of stocks stir up controversy like no other? Penny stocks. These tickers trading for less than $5 per share have earned a reputation as some of the most divisive names on Wall Street, with these plays either met with open arms or given the cold shoulder.

Meet Samuel – Your Personal Investing Prophet

- Start a conversation with TipRanks’ trusted, data-backed investment intelligence

- Ask Samuel about stocks, your portfolio, or the market and get instant, personalized insights in seconds

It’s understandable why some investors are wary. Those opposed are quick to point out that there could be a very real reason these stocks are changing hands for pocket change, with the low share prices often masking obstacles like weak fundamentals or troubling headwinds.

That said, others are drawn in by the sheer growth potential of penny stocks. The fact is that even minor share price appreciation can mean huge percentage gains, and thus, serious returns. What’s more, your money goes further with these bargain names.

No matter which side you take, one thing is certain, due diligence is necessary before making any investment decisions. That’s where the experts come in, namely the analysts at Roth Capital. These pros bring experience and in-depth knowledge to the table.

With this in mind, our focus turned to two penny stocks that have received a thumbs up from Roth Capital analysts. Running the tickers through TipRanks’ database, both have been cheered by the rest of the Street as well, as they boast a “Strong Buy” analyst consensus. Not to mention substantial upside potential is on the table.

Cellectar Biosciences (CLRB)

Leveraging its patented phospholipid drug conjugates (PDCs) delivery platform, Cellectar Biosciences develops cutting-edge treatments for cancer. Based on the potential of its drug candidate, CLR 131, and its $1.24 share price, Roth Capital thinks that now is the time to get in on the action.

Representing the firm, analyst Jonathan Aschoff tells clients that he is optimistic about CLR 131, which is a small-molecule, targeted PDC designed to deliver cytotoxic radiation directly and selectively to cancer cells, in the lymphoplasmacytic lymphoma (LPL)/Waldenstrom’s macroglobulinemia (WM) indications.

According to Aschoff, following its Type B guidance meeting with the FDA, “CLRB is prepared to initiate its first pivotal CLR 131 trial in LPL/WM after achieving a 100% ORR and 75% major response rate in four patients.” He points out that although CLRB just reported promising results in multiple myeloma (MM) (40% ORR in triple class refractory (TCR) patients at total body doses of at least 60mCi), LPL/WM was selected for the initial pivotal trial based on the very strong initial results and the lower competition for patients.

“We view this as a prudent decision because NCCN compedia listing in MM is a mere peer-reviewed publication away, if first approved in LPL/WM. We also note that CLRB has steadily improved its dosing of CLR 131, essentially fractionating the doses so that higher total body doses are well tolerated,” Aschoff further explained.

Adding to the good news, the therapy generated activity in preliminary Phase 1 unresectable brain tumors. Aschoff added, “Disease control was shown in two heavily pretreated patients with ependymomas, showing the drug’s ability to cross the blood brain barrier, and all doses through 60 mCi/m2 have exhibited a favorable safety profile.”

To this end, Aschoff rates CLRB a Buy along with a $10 price target. Investors could be pocketing a gain of 713%, should this target be met in the twelve months ahead. (To watch Aschoff’s track record, click here)

Are other analysts in agreement? They are. 5 Buys and no Holds or Sells have been issued in the last three months. So, the message is clear: CLRB is a Strong Buy. Given the $5.48 average price target, shares could soar 345% from current levels. (See CLRB stock analysis on TipRanks)

Applied Genetic Technologies (AGTC)

With vast gene therapy experience, Applied Genetic Technologies designs and constructs all critical gene therapy elements and brings them together to develop successful treatments for patients. Currently going for $4.50 apiece, Roth Capital believes this stock’s long-term growth narrative is strong.

Firm analyst Zegbeh Jallah points out that recently released data for its XLRP gene therapy program, which is expected to enter pivotal studies in Q1 2021, reaffirmed his bullish thesis. “Despite the market not fully appreciating the data given how the stock traded, we continue to believe that the results suggest that AGTC could have a best-in-class therapy, which is supportive of the planned pivotal efforts,” he explained.

Providing an update on the results of the Phase 1/2 XLRP study, using the FDA’s criteria, AGTC evaluated responses at 12 months in the lower dose groups (2 and 4), and 6 months in the higher dose groups (5 and 6). According to Jallah, “initial responses were observed in dose Groups 2, 3, 4, 5 and 6, with impressive response durability even at 12 months.”

On top of this, at 6 months, the dose used in Group 5 resulted in a 43% response rate or a 57% response rate if excluding a patient not meeting the enrollment criteria. In Group 6, a response rate of 50% was observed, or 100% excluding patients not meeting the enrollment criteria.

Jallah added, “All measurements were obtained in the 36 perimetry grid, which we believe should make it easier to preselect loci likely to respond. Although BCVA is not the primary endpoint, BCVA improvements, which can capture changes in the central region, were maintained at 12 months.”

Even though some investors have expressed concern about Meira’s competing therapy, Jallah believes AGTC’s technology could have a leg up. “Overall, we believe that the data from both companies is strongly indicative of the efficacy potential of gene therapy for inherited retinal disease, and although differences in the study design makes direct comparisons difficult, we believe that AGTC could have a competitive advantage heading into pivotal studies,” he commented.

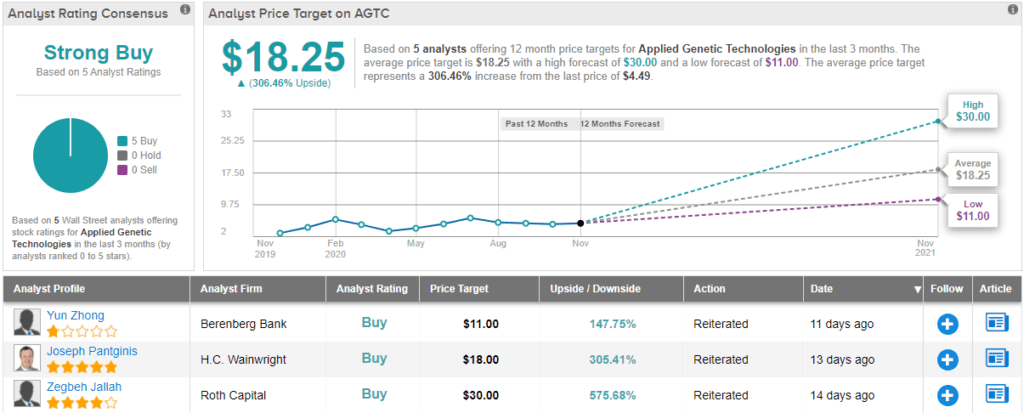

In line with his optimistic approach, Jallah reiterated a Buy rating and $30 price target, indicating 568% upside potential. (To watch Jallah’s track record, click here)

All in all, other analysts echo Jallah’s sentiment. 5 Buys and zero Holds or Sells add up to a Strong Buy consensus rating. The average price target of $18.25 is less aggressive than Jallah’s but still leaves room for upside potential of 306%. (See AGTC stock analysis on TipRanks)

To find good ideas for penny stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.