The fourth quarter is now upon us and that means Tesla (NASDAQ:TSLA) will soon be announcing its delivery haul for Q3. The EV leader is set to announce its global third-quarter deliveries on Thursday (October 2) and it is already understood that it will be a better showing than this year’s abysmal first two quarters.

Claim 55% Off TipRanks

New trading tool for TSLA bearsAccordingly, ahead of the announcement, William Blair’s Jed Dorsheimer, an analyst who ranks among the top 3% of Street stock experts, has raised his delivery estimate.

As anticipated, the end of the EV tax credit resulted in a pull-forward in demand, but the uptake has exceeded Dorsheimer’s expectations. Strong U.S. demand for the new Model Y has been a “bright spot,” while a rebound in China and other regions has helped offset ongoing softness in Europe. As such, the analyst has increased his third-quarter delivery estimate from 437,000 to 480,000 vs. the Street’s forecast of 443,000. “We believe the buy-side is ahead of the sell-side here and closer to our estimate,” Dorsheimer went on to say.

Looking ahead to Q4, Dorsheimer is taking a cautious view on margins due to a slowdown in auto deliveries and reduced revenue from regulatory credits. “However,” the analyst said, “the market has looked through our concerns and momentum from robotaxi, Elon Musk’s stock purchase, and new energy storage products have pushed the stock to near all-time highs.”

The climb back to that peak notched last December represents a big turnaround after the shares took a heavy beating earlier this year, with car sales plummeting and Elon Musk’s political activities souring sentiment.

Now shares are trading at an enterprise value of 118x Dorsheimer’s 2026 EBITDA estimate, representing a “significant premium” to technology peers, which trade at 20–25x. The analyst anticipates that the effects of the OBBB (One Big Beautiful Bill) will result in a reset of Street estimates, putting pressure on this multiple premium. “After Street estimates reset, we will look for more data points on our bullish views on energy storage and robotaxi to regain momentum,” the analyst further said.

Dorsheimer counts risks here that include competition – especially from Chinese EV makers and energy storage companies – geopolitical exposure due to significant business in China, and “key-man risk” related to CEO Elon Musk.

For now, Dorsheimer remains on the sidelines with a Market Perform (i.e., Neutral) rating, although he says it is a stance he finds “increasingly difficult to maintain.” The analyst has no fixed price target in mind. (To watch Dorsheimer’s track record, click here)

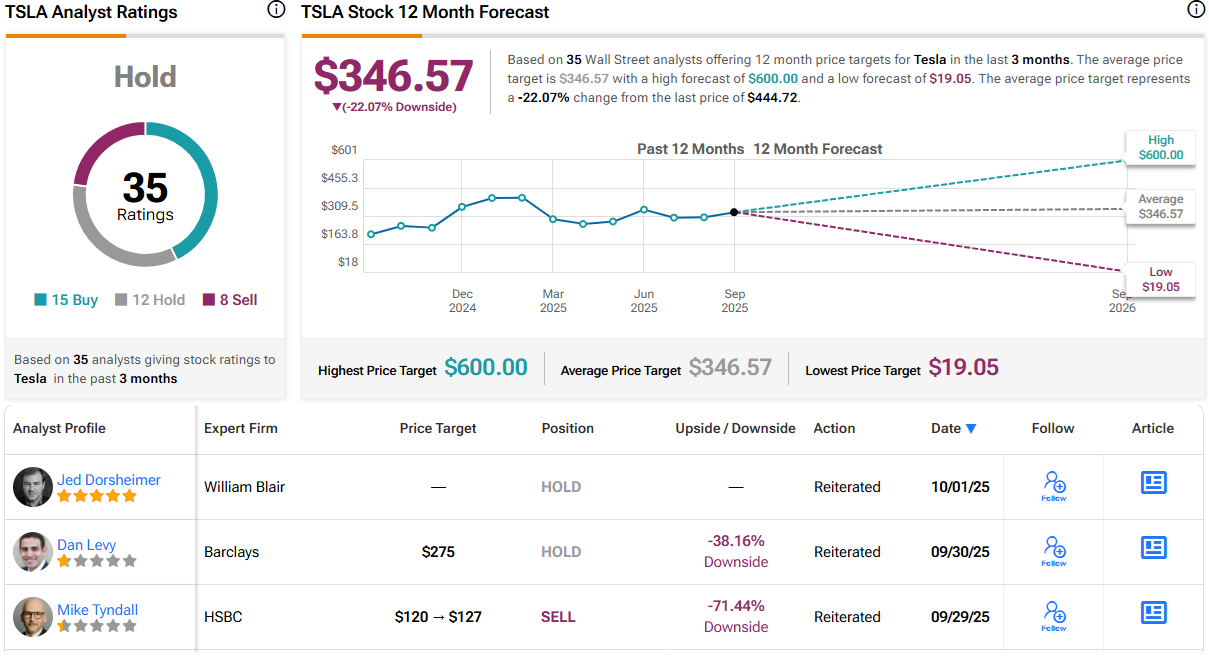

Others on the Street do have targets, and the average lands at $346.57, a figure that suggests the stock will fall by 22% in the months ahead. Overall, based on a mix of 12 Holds, 15 Buys and 8 Sells, the analyst consensus rates the stock a Hold. (See Tesla stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.