Tattooed Chef (NASDAQ:TTCF) is officially going bankrupt, and I definitely do not believe that anyone should bet on this once-promising start-up. I am bearish on TTCF stock because, unfortunately, Tattooed Chef’s management painted a rosy picture of the company’s future prospects even while Tattooed Chef had major problems.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Hailing from California, Tattooed Chef offers prepared plant-based meals that can be ordered online and sometimes found in the freezer section of grocery stores. Tattooed Chef’s meals actually look pretty tasty, and before U.S. inflation got out of hand, the company’s future probably seemed bright.

However, persistent inflation has undoubtedly made it difficult to sell Tattooed Chef’s plant-based offerings, which aren’t cheap. Besides, the market’s enthusiasm for unprofitable start-up businesses has waned during the past year or so. Now, Tattooed Chef’s hapless shareholders must decide whether to hold on through the company’s Chapter 11 filing. Personally, I’d say it’s best to cut one’s losses and learn some valuable lessons.

Tattooed Chef: Confidence Isn’t Enough

I wouldn’t necessarily characterize Tattooed Chef as a “zombie” company, but it’s been unprofitable for a while, and that’s certainly a telltale sign. Also, as I’ll discuss in a moment, Tattooed Chef’s sales haven’t been stellar lately. Nevertheless, the company’s chief executive sounded quite confident during the most recent quarterly earnings call – but maybe he was too confident.

Let’s backtrack a little bit to Tattooed Chef’s update from March of this year. As the company implemented cost-cutting initiatives, Tattooed Chef President and CEO Sam Galletti claimed to observe “early indications of our progress on a sequential quarterly basis, with material improvements expected to manifest beginning in Q1 2023 and continuing throughout the year.”

That’s all fine and well, but as always, informed investors needed to read the fine print at the bottom of the page. In particular, Tattooed Chef admitted that it “expects cash at December 31, 2022 of approximately $6 million,” which isn’t very much cash for a company to continue its operations. Furthermore, Tattooed Chef acknowledged that it “continues to require additional debt or equity capital and is pursuing multiple paths of opportunity to raise such capital as soon as practicable.”

Fast-forward to May, and Galletti mentioned the word “confidence” or “confident” multiple times during the company’s first-quarter 2023 conference call. Confidence is fine, but it has to be backed up by the data. In Tattooed Chef’s case, the data in Q1 2023 was mixed, at best.

Tattooed Chef’s Glaring Red Flags

Suffice it to say, Tattooed Chef’s top-line results weren’t stellar. On a year-over-year basis, the company’s net revenue declined 12.7% to $59.1 million. Moreover, Tattooed Chef reported a gross loss of $4.1 million in Q1 2023 versus a $4.1 million gross profit in the year-earlier quarter.

Turning to the bottom-line results, I suppose it’s slightly positive that Tattooed Chef narrowed its net loss from $20.2 million in the year-earlier quarter to $19 million in 2023’s first quarter. I suspect that this marginal improvement resulted from Tattooed Chef’s reduction of expenses rather than from the company actually selling a lot of plant-based meals during that time.

Meanwhile, another bright red flag waved as Tattooed Chef received a noncompliance notice from the Nasdaq exchange. You might assume that’s because TTCF stock fell below the Nasdaq exchange’s $1 minimum bid price, but that’s another issue entirely. This particular noncompliance notice occurred because Tattooed Chef allegedly failed to file its Form 10-K annual report in a timely manner.

Then, on the last day of June, Tattooed Chef dropped a bombshell on its already-struggling shareholders. In a press release, Tattooed Chef stated that it’s filing for Chapter 11 bankruptcy protection and selling its assets to the highest bidder(s) with an “expedited sale process.”

I don’t know about you, but when I read “expedited sale process,” I’m thinking “fire sale” and “everything must go.” Going forward, Galletti hopes to “provide clarity on the future of the Company for all our stakeholders.” Again, the CEO exudes confidence though it’s probably not warranted; Tattooed Chef’s shareholders should expect nothing in the end because that’s probably what they’ll get.

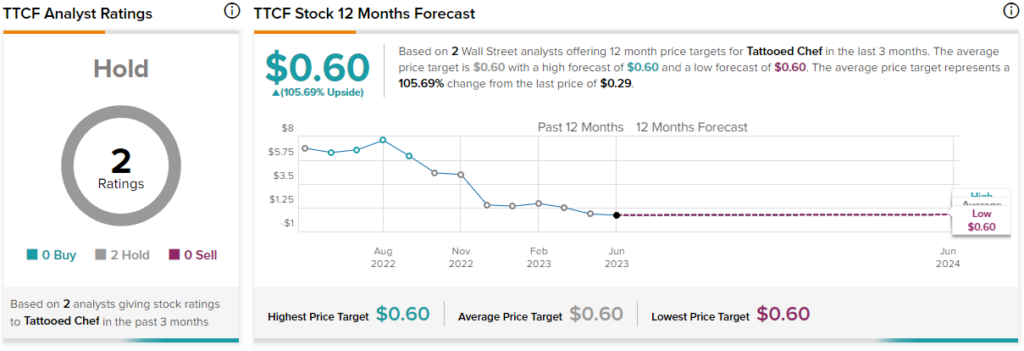

Is TTCF Stock a Buy, According to Analysts?

Turning to Wall Street, TTCF is a Hold based on two Hold ratings. The average Tattooed Chef stock price target is $0.60, implying 105.7% upside potential (though that might change in the near future).

Conclusion: Should You Consider Tattooed Chef Stock?

I like plant-based food as much as anyone, but the red flags were there for Tattooed Chef all along despite the CEO’s outlook for the company. Now, after a 46.6% single-day drop in Tattooed Chef stock yesterday, the shareholders have little more than Galletti’s promise to “provide clarity” and perhaps the hope of a miraculous meme-stock short-squeeze.

Waiting around for miracles isn’t a viable investing strategy, so I won’t blame any of Tattooed Chef’s unfortunate shareholders if they choose to cut and run. As for anyone who’s tempted to buy TTCF stock now, just bear in mind that the company’s cost-reduction measures and the chief executive’s confidence weren’t enough to avert a Chapter 11 filing, which may end up being the final chapter in Tattooed Chef’s tragic tale.