The medical devices scene is an intriguing corner of the Healthcare sector and one that could entail above-average growth rates through the next decade. Undoubtedly, it’s not just biotech innovators (think the makers of GLP-1 weight-loss drugs) that can help inject growth into investor portfolios. As the following capable med-tech firms advance their unique innovations forward, it should come as no surprise that a number of top analysts stand by names such as SYK, ISRG, and DXCM at current levels.

Meet Samuel – Your Personal Investing Prophet

- Start a conversation with TipRanks’ trusted, data-backed investment intelligence

- Ask Samuel about stocks, your portfolio, or the market and get instant, personalized insights in seconds

Therefore, let’s use TipRanks’ Comparison Tool to have a closer look at the trio of Strong-Buy-rated medical device stocks.

Stryker (SYK)

Stryker is a medical device heavyweight that’s just days away from pulling the curtain on its (latest) second-quarter earnings results. The setup for Stryker going into earnings looks pretty good, with the stock now down around 6% (I guess you could call it a mini-correction) from its all-time highs and the recent pick-up in acquisition activity. In any case, I’m inclined to stand by the bulls on this one as Stryker looks to power its way back to double-digit sales growth.

Up ahead, Stryker seems well-equipped to follow up on its strong first quarter showing (Q1 earnings per share coming in at $2.50, just ahead of the $2.36 consensus expectation). Needham, which upgraded the stock in May, sees Stryker surprising to the upside on revenue, thanks to “product launches and a capital equipment backlog.”

Last month, Stryker launched a handful of interesting new products, including the surprisingly slim LIFEPAK 35 monitor and defibrillator unit and the Gamma4 system in Europe for treating broken hip bones. And up ahead, Stryker could break new ground with its surgical robot Mako, which has spine and shoulder applications just around the corner.

Apart from organic innovations, Stryker is also moving fast on M&A, closing its Artelon deal—a firm in the business of soft-tissue fixation—just last week. All things considered, Stryker has much going for it in the second half of the year. And at just 28.9 times forward price-to-earnings (P/E), shares seem way too cheap, given the magnitude of its growth drivers.

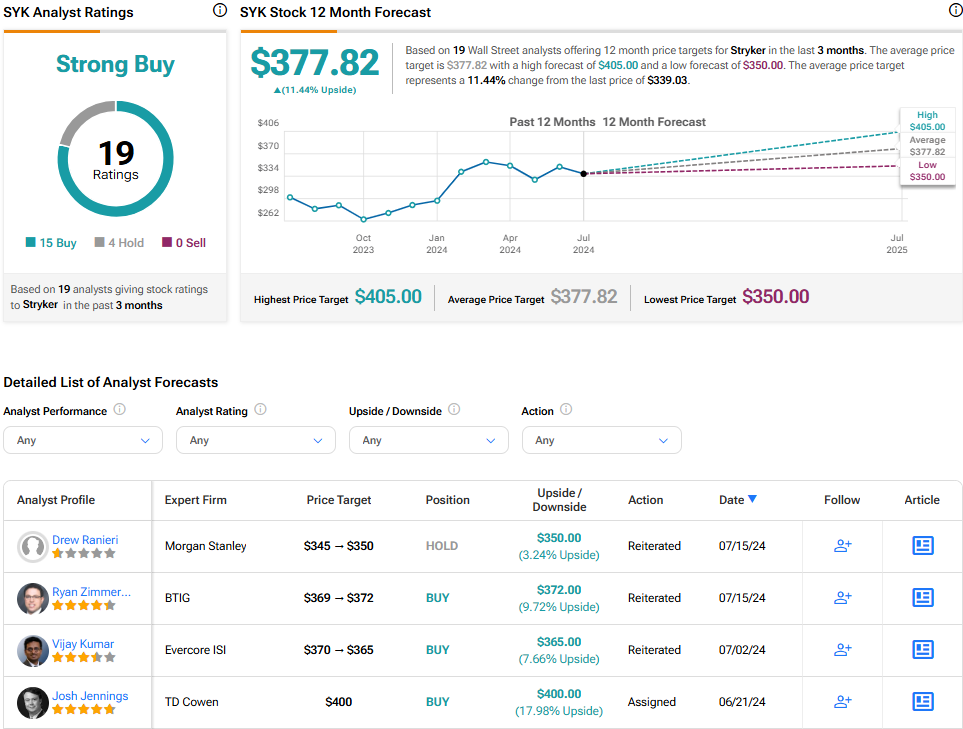

What Is the Price Target for SYK Stock?

SYK stock is a Strong Buy, according to analysts, with 15 Buys and four Holds assigned in the past three months. The average SYK stock price target of $377.82 implies 11.4% upside potential.

Intuitive Surgical (ISRG)

Speaking of surgical robots, we have the maker of the da Vinci surgical system, Intuitive Surgical, which has been quietly rallying to new all-time highs over the past few months. Despite gaining more than 36% year-to-date, Intuitive may still have enough wind at its back to end the year above the $500 mark (currently around $460).

In the past few weeks, a trio of analysts upgraded their price targets above $500. As da Vinci hopes to add to the momentum it saw in the second quarter (da Vinci procedures soared 17% in Q2), it’s hard to be anything but bullish on the name right now.

Of course, it’s hard for value-conscious investors to buy stocks at or around all-time highs. However, I view ISRG as having all the traits of a winner poised to continue winning. Indeed, if you avoided ISRG shares just because they’ve been hot, you missed out on a remarkable run.

As demand for minimally invasive surgeries continues to rise, perhaps the da Vinci 5 system’s robust second quarter is just a hint of what’s to come. Beyond da Vinci, the Ion Endoluminal system, which saw a blistering 82% in volume growth last quarter, looks like an intriguing growth driver as demand for minimally-invasive biopsies also picks up steam.

At 72.9 times forward P/E, ISRG shares do not come cheap. They’re markedly pricier than SYK shares right here. However, given the growth momentum behind the name and the firm’s leading position in surgical robots, the hefty multiple seems worth paying. Further, I’d not be shocked if ISRG evolves into the next big “Magnificent Seven” type of stock in as little as five years from now.

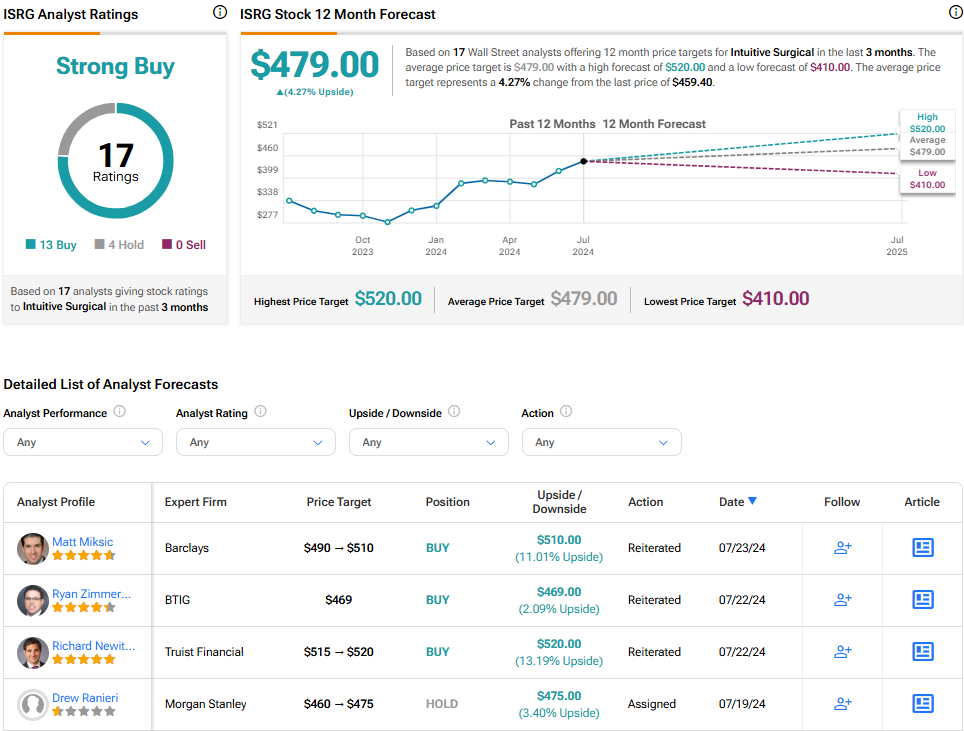

What Is the Price Target for ISRG Stock?

ISRG stock is a Strong Buy, according to analysts, with 13 Buys and four Holds assigned in the past three months. The average ISRG stock price target of $479.00 implies 4.3% upside potential.

Dexcom (DXCM)

Dexcom is a diabetes management firm that’s having a tough start to the year, with shares down 9% year-to-date. With quarterly earnings due on Thursday, perhaps investors may wish to nibble into the name ahead of the big number. Despite recent pressures, Dexcom is continuing to innovate with its glucose-monitoring system. And with new patients rising at an impressive rate, perhaps the med-tech innovator is more of a hidden value play that could make up for lost time in the second half of the year. For now, I’m inclined to be bullish.

Just over a month ago, the Dexcom G7, one of the market’s most accurate glucose monitors, landed on the (AAPL) Watch App Store, allowing users to track their blood sugar levels in real time. That’s an in-demand feature that may just be able to help DXCM stock sustain a comeback.

Though Dexcom almost seems untouchable in the diabetes scene right now, I would keep tabs on Apple and its future Apple Watch devices, as rumors have swirled that a future release may include its own glucose monitoring system. Indeed, such a system would be a game-changer for Apple and a massive gut-punch for Dexcom. For now, though, Apple Watch rumors are just that, rumors. As such, DXCM investors shouldn’t be running to the hills just yet.

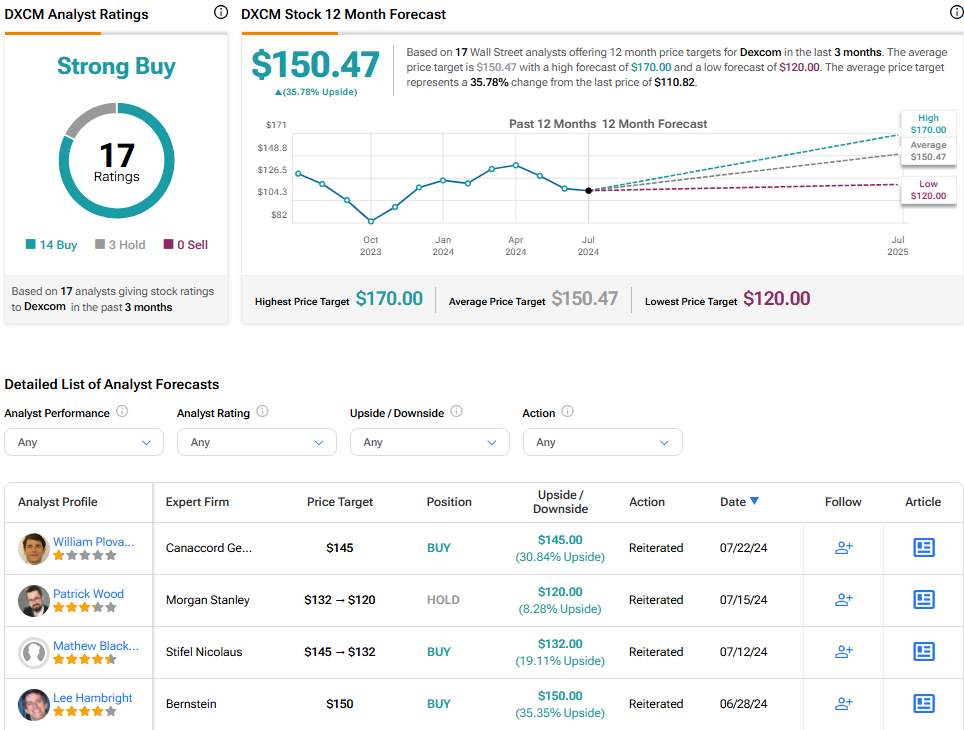

What Is the Price Target for DXCM Stock?

DXCM stock is a Strong Buy, according to analysts, with 14 Buys and three Holds assigned in the past three months. The average DXCM stock price target of $150.47 implies 34.2% upside potential.

Conclusion

The med-tech scene is full of high-growth innovators that may be a heck of a lot cheaper than they seem. Whether we’re talking about Stryker and its packed pipeline of devices, Intuitive Surgical and the momentum behind its da Vinci, or Dexcom and its new Apple Watch app, each one of the names has more than enough rally fuel as we head into the fall season.

Of the three names, Wall Street sees DXCM stock as having the most room to run (35.8% upside potential). Given its relative underperformance and market leadership, I’m inclined to agree with the Wall Street crowd.