I currently hold a neutral stance on Super Micro Computer (SMCI), a supplier of data center servers and storage solutions. Over the past 12 months, the company has experienced significant valuation volatility. In light of recent concerns surrounding its accounting practices and the resignation of its auditor, Ernst & Young, the stock has declined by 43.8% in the past three months. While Super Micro Computer may now be trading at a fair valuation, it still presents risks that warrant caution.

Claim 30% Off TipRanks Premium

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Stay ahead of the market with the latest news and analysis and maximize your portfolio's potential

Super Micro Computer Faces Regulatory Risks

I’m neutral on Super Micro Computer due to concerns about its management’s track record amid current accusations. Currently, the U.S. Department of Justice is reportedly investigating Super Micro Computer following allegations of accounting manipulation, undisclosed related-party transactions, and possible violations of U.S. export controls, raised by Hindenburg Research, an investigative firm known for short-selling.

Hindenburg Research highlighted Super Micro Computer’s previous shortfalls in its report, including that it was temporarily delisted from Nasdaq in 2018 for failing to file financial statements and that in August 2020, the SEC charged it with “widespread accounting violations.”

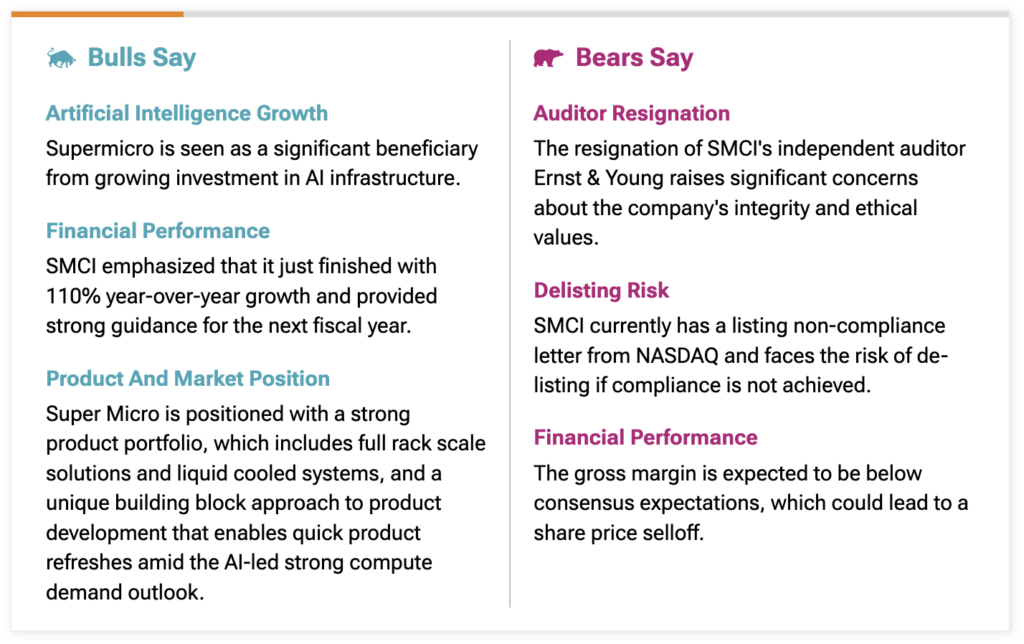

Recently, Ernst & Young, the company’s auditor, resigned, citing concerns about the reliability of management’s financial statements and internal controls. Although the company’s independent Special Committee found no evidence of fraud or misconduct, Ernst & Young’s resignation is, in my view, a significant red flag, weakening the appeal of the bull case.

SMCI May Be Fairly Valued in an Optimistic Outcome

I’m currently neutral on Super Micro Computer stock, even though it is down over 70% since March 2024 and now presents better value. Its EV-to-EBITDA ratio of 12.6 is close to the 10-year median of 11.3—a sharp drop from the peak of over 70 in March 2024 when market sentiment was at its highest.

This lower valuation is significant, given the company’s impressive 55.1% three-year annual revenue growth rate, far above the 10-year median of 17.2%. Strong growth is likely to continue through 2025, driven by demand for servers and storage solutions in data center expansions. However, by Fiscal 2026 and beyond, I anticipate more moderate annual revenue growth rates of around 16% to 17%, based on my analysis.

Super Micro Computer’s EBITDA margin is currently 8.73%, above its five-year average of 6.76%. While the company is likely to sustain stronger earnings than revenue growth due to economies of scale in high-value segments, earnings growth rates will likely taper as revenue growth slows. In the near term, however, this should expand its EBITDA margins, and I estimate an EBITDA margin of 9% by the end of Fiscal 2026.

If the company achieves my estimate of $30 billion in revenue for Fiscal 2026, it would therefore generate EBITDA of $2.7 billion. At an EV-to-EBITDA ratio of 13 (primarily due to its improved EBITDA margin), the company would have an enterprise value of $35.1 billion by June 2026, the end of Fiscal 2026. With a current enterprise value of $16.72 billion, this does suggest significant near-term upside potential.

SMCI’s Potential Reputational Loss Could Prove Detrimental

Remember, I’m neutral on the stock because the above outcome is highly dependent on a positive resolution of Super Micro Computer’s ongoing regulatory challenges and external investigations. In a worst-case scenario, the company could not only lose investor confidence but also many of its customers. Given the current high-risk environment and the concerns about management’s integrity, I believe it is best to consider other opportunities.

The analyst community is indeed divided on this investment. Bulls highlight the company’s impressive financial performance, with 110% year-over-year revenue growth driven by artificial intelligence advancements, while bears point to risks such as the auditor’s resignation and the potential for Nasdaq delisting.

It’s important to remember that the 110% year-over-year revenue growth reflects historical performance and shouldn’t be relied upon to predict future returns. The forward revenue growth rate currently stands at 65.5% but is likely to taper quickly in the coming years.

How Do Wall Street Analysts Rate SMCI Stock?

Looking directly at the Wall Street ratings, the stock currently has a consensus Hold rating, with an average SMCI price target of $54.17, indicating a 139% upside potential. This is based on three Buys, nine Holds, and one Sell.

While the average price target does suggest the potential for substantial near-term gains, the consensus Hold rating reflects significant risks that should not be overlooked, as outlined above.

Conclusion: The Opportunity Is Too High-Risk

There’s a saying in investing: “A large part of success is not losing money.” This is especially relevant in the case of Super Micro Computer stock. I remain neutral on this investment, as there are many other attractive growth and value opportunities in the market that do not carry the same level of regulatory risk. Despite its near-term growth potential, my rating is a Hold.