Super Micro Computer (SMCI) might have the word “micro” in its name, but make no mistake—this Silicon Valley-based server and storage powerhouse has been delivering mighty growth over the past three years. With the boom in AI training, cloud data centers, and enterprise IT, Super Micro has surged 829%, alongside some of the hottest trends in technology.

Claim 30% Off TipRanks

New trading tool for NBIS bulls/bears

While the company’s most explosive alpha years—2023 and 2024—are now behind us, I believe the runway is far from finished. Based on projected earnings per share growth and only a slight expansion in the price-to-earnings ratio, I’m targeting a 40% return from the stock over the next twelve months.

Super Micro Is Not So Micro

Let’s start with the obvious: Super Micro’s growth has been anything but modest. The surge in artificial intelligence workloads and expansion in cloud infrastructure has created ideal conditions for the company to thrive. Management has been bold, too. They’ve described the AI revolution as “much more impactful than the Industrial Revolution,” and they’re positioning Super Micro accordingly. If that thesis holds true—and I believe it does—then the company is in a superb position to capitalize over the coming years.

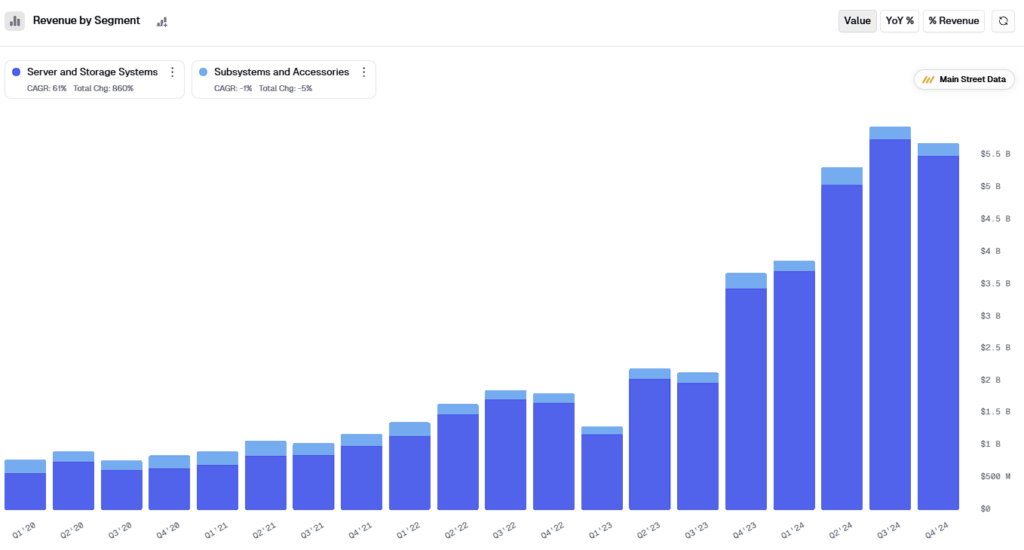

One specific area where Super Micro stands out is liquid-cooled server design. According to the company’s CEO, roughly 30% of new data centers are expected to adopt direct liquid cooling over the next twelve months. That’s significant—and Super Micro is already a frontrunner in this space. According to Main Street Data, SMCI’s revenues have grown as segment proportions have remained broadly consistent.

Let’s talk numbers. In FY2024, SMCI posted 110% year-over-year revenue growth. GAAP net income also surged, climbing 80% from the previous year. Looking further back, from FY2021 through FY2024, Super Micro pulled off a stunning 60% compound annual growth rate in revenue—while only growing its operating expenses by 25%. The company is scaling with discipline and efficiency, an increasingly rare feat in today’s hyper-growth tech landscape.

We’re already well into FY2025, with Q3 results expected in May. For the full year, management is guiding toward approximately $24 billion in revenue, representing about 60% year-over-year growth. They’re also quite bullish about FY2026, setting expectations for $40 billion in annual revenue. That forecast may be optimistic, but the broader growth trajectory is undeniably strong—and the valuation doesn’t seem overstretched given the potential upside ahead.

Super Micro’s Price Cooldown

Currently, Super Micro stock is trading at ~$35 per share after a sharp pullback, meaning it’s priced at less than its trailing twelve-month revenue—a clear signal of value. But investor sentiment has understandably cooled. The company dealt with accounting-related issues in past years, and for many market participants, those concerns still linger. Even so, a moderation to 60% revenue growth—the midpoint of current guidance—would take FY2025 revenue to around $24 billion and would exceed expectations, likely leading to a stock re-rating.

Looking further ahead to FY2026, I estimate Super Micro will generate around $3.75 in normalized earnings per share. Applying a modest 13.5x non-GAAP P/E ratio—roughly in line with where the stock trades today—gives us a 12-month price target of $50. That’s a potential return of about 40%, making a compelling case to stay bullish on SMCI stock.

Another High-Conviction Bet on AI

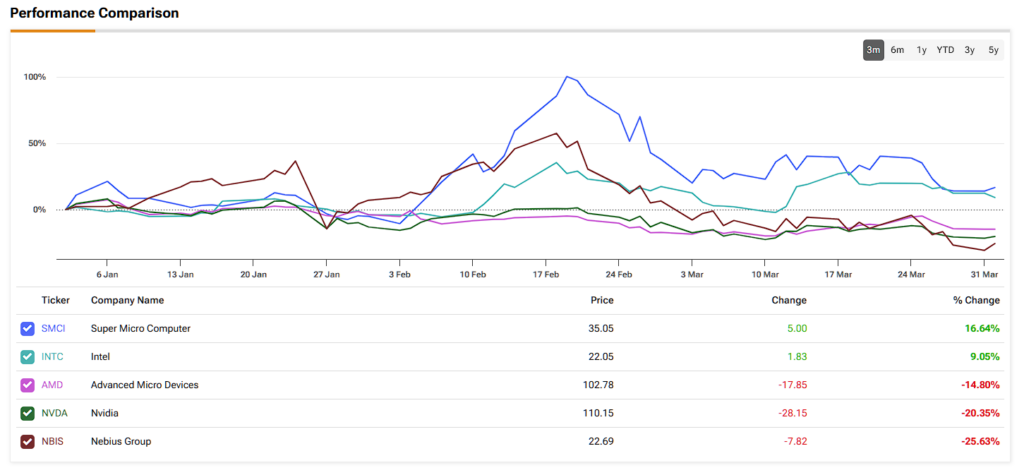

Some investors are cautious about the AI space, wary of a potential repeat of the dot-com bubble. But I believe this comparison falls short. Every time major partners like Intel (INTC), AMD (AMD), or Nvidia (NVDA) release new chips, Super Micro is often first to market with compatible servers. That kind of agility and first-mover advantage matters—especially when capital expenditures in data centers could scale to over $1 trillion annually in the next five to ten years.

Further underscoring the bullish sentiment, Super Micro is one of several core players in this megatrend that I believe deserves a seat in any forward-looking tech portfolio. Alongside Nvidia, AMD, and early-stage hyperscalers like Nebius (NBIS), Super Micro adds meaningful exposure to the infrastructure layer of AI computing. Of course, weighing the active risks is crucial; however, while the company has resolved its previous SEC filing delays, history still casts a shadow. The stock would almost certainly take a steep dive if another accounting issue arises. In financial markets, once bitten, twice shy.

Is Super Micro Computer a Good Stock to Buy?

On Wall Street, SMCI stock has a consensus rating of Hold based on four Buy, four Hold, and two Sell ratings over the past three months. SMCI’s average price target of $49 per share implies approximately 40% upside potential over the next twelve months.

The consensus upside projection is not a guarantee, of course, but it provides some external validation for the bullish thesis. And while analyst sentiment isn’t uniformly glowing, the general tone is far more constructive than what you’d expect from a stock with historically murky accounts. In Super Micro’s case, the fundamentals are robust—if you’re comfortable with the volatility and believe in management’s future integrity.

SMCI Stands Tall as a Risk-On Play for AI Optimists

Let’s not kid ourselves—Super Micro is a risk-on trade—but a calculated one. Even if hyper-growth days are behind us, SMCI continues posting above-average revenue figures while trading at a reasonable valuation. With my estimated $3.75 in normalized EPS by FY2026 and forward earnings multiples under 13.5x, this looks like a sensible entry point for long-term investors who believe in AI infrastructure as a secular theme.