Election day is just around the corner, and Wall Street is placing its bet on a Democratic sweep. Following the Presidential debate on September 29, the chance of a Biden victory has been increasing in the market.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Since September 30, the S&P 500 has moved 5.5% higher. That said, the rotation into cyclicals and small-caps has been much more pronounced, with the Russell 2000 surging 8.5% over the same period.

Weighing in for Raymond James, strategist Tavis McCour argues the shift into cyclicals and small-caps “provides some evidence of how the market will rotate in the case of a Democratic sweep, with the logic being stronger fiscal support, steeper yield curve and faster cyclical recovery.”

McCour points out that “in the background is remarkably sustainable economic data, and the likely positive impact to EPS.” According to the strategist, Atlanta Fed GDPNow, a model used to estimate real GDP, has increased materially since July, with the firm’s analysts continuing to skew towards raising 2020 EPS estimates nearly every week since May. He noted, “Every sector of the S&P 500 has seen 2020 EPS expectations increase since mid-August (which is not normal). It should be a good Q3 earnings season, and earnings still matter.”

Bearing this in mind, our focus turned to three stocks backed by Raymond James, with the firm’s analysts noting that each could skyrocket over 100% from current levels. Running the tickers through TipRanks’ database, we found out that the rest of the Street is also on board, as each boasts a “Strong Buy” consensus rating.

Catalyst Biosciences (CBIO)

Focused on addressing unmet needs in rare hemostasis and complement-mediated disorders, Catalyst Biosciences hopes to improve the lives of patients from all over the world. Based on the progress of its development pipeline, Raymond James believes its $4.80 share price could reflect the ideal entry point.

After the company provided an update on the recent progress made by both of its lead assets gearing up for Phase 3, MarzAA and DalcA, firm analyst David Novak points out that his bullish thesis is very much intact. MarzAA is a next-generation SQ FVIIa designed as a potential treatment for hemophilia A or B with inhibitors, and DalcA is an SQ FIX designed for hemophilia B.

“With two Phase 3-ready assets addressing a significant market opportunity and shares currently trading at an enterprise value of ~$2 million, CBIO remains substantially undervalued in our view. We believe the company is well-positioned for a significant market re-rating over the next 12 months,” Novak commented.

Highlighting its poster presentations at the International Society for Thrombosis and Haemostasis (ISTH) Virtual Congress, Novak believes the data supports the selected dosing regimen for MarzAA in the upcoming Phase 3 CRIMSON-1 trial. On top of this, strong safety and efficacy data from its Phase 2b trial of DalcA was presented at the World Federation of Hemophilia Virtual Summit.

To this end, Novak sees several potential catalysts on the horizon. The enrollment of the first patient in the Phase 3 trial of MarzAA in hemophilia A or B with inhibitors is slated for 2H20, but this is subject to COVID-related delays. What’s more, MarzAA will be evaluated in a Phase 1/2 trial in patients with FVII deficiency, Glanzmann Thrombastenia and those using Hemlibra, with this trial set to kick off in late 2020.

Adding to the good news, the announcement of a FIX gene therapy candidate and the unveiling of a systemic complement inhibitor development candidate, which could both come in late 2020, stand to drive additional upside, in Novak’s opinion.

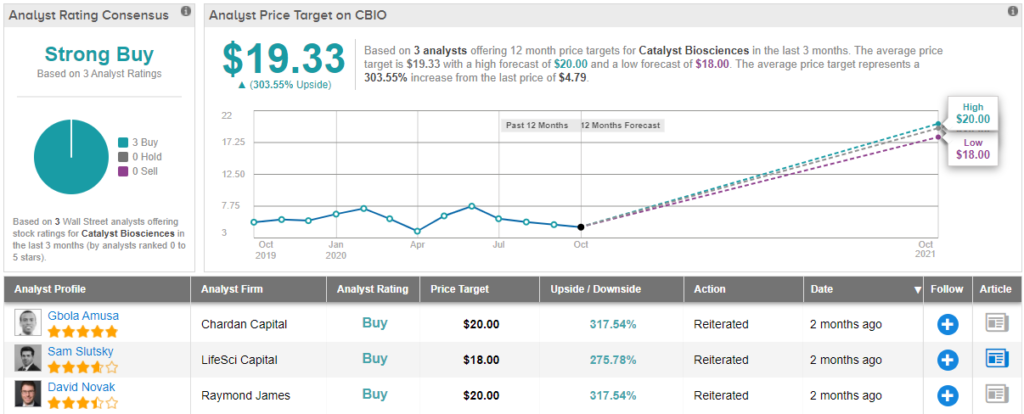

To this end, Novak rates CBIO an Outperform (i.e. Buy) along with a $20 price target. Investors could be pocketing a massive gain of 317%, should this target be met in the twelve months ahead. (To watch Novak’s track record, click here)

Other analysts don’t beg to differ. With 3 Buy ratings and no Holds or Sells, the word on the Street is that CBIO is a Strong Buy. At $19.33, the average price target implies 303% upside potential from current levels. (See CBIO stock analysis on TipRanks)

Mirum Pharmaceuticals (MIRM)

With the goal of creating life-changing therapies for patients with liver diseases, Mirum Pharmaceuticals believes its approach can address the underlying causes. Ahead of a key filing, Raymond James likes what it has been seeing.

Writing for the firm, 5-star analyst Steven Seedhouse points out that his optimism is driven by MIRM’s new plan to submit an MAA application to the European Medicines Agency (EMA) for maralixibat (MRX), its minimally absorbed and orally administered investigational therapy that could potentially be used in several indications, in PFIC2 in Q4 2020.

While this filing would come before the ongoing MARCH Phase 3 study wraps up, Seedhouse points out that this move is in line with discussions it has already had with the EMA. According to the analyst, based on statistical analyses conducted by NAPPED that compared Phase 2 data (including long-term transplant-free survival data) to natural history data, the EMA is on board with MIRM’s strategy to file for full approval.

“Thus, we have increased confidence MRX will be approved in PFIC2, which we estimate could occur by Q1 2022 (up from our estimate of 2H22),” Seedhouse mentioned. Contributing to his bullish stance, MRX already has a very large safety database as it has been evaluated in several studies across multiple indications (NASH, ALGS and PFIC).

Additionally, the Phase 2 INDIGO study demonstrated a statistically significant pruritus improvement (ItchRO scale) in the overall PFIC2 population, as well as strong and sustained improvements in serum bile acid (sBA) level, ItchRO score, height z-score and PedsQL (quality of life metric) for 6 responder patients that all had a form of the disease characterized by non-truncating bile salt export pump (BSEP) protein. Approximately half of all PFIC patients fall into this category.

Looking at data on five-year outcomes with MRX, transplant-free survival was established in seven non-truncating PFIC2 patients who achieved sBA control. If that wasn’t enough, no clinical events were witnessed and 2 out of 7 patients came off of the transplant waiting list.

Seedhouse added, “This data is further supported by natural history data from the NAPPED consortium, which shows 100% 15-year native liver survival in biliary diversion patients with sBA levels controlled to below 102µmol/L.”

Everything that MIRM has going for it convinced Seedhouse to put a Strong Buy rating on the stock. He assigned a $48 price target, suggesting 140% upside potential. (To watch Seedhouse’s track record, click here)

Are other analysts in agreement? They are. Only Buy ratings, 5 to be exact, have been issued in the last three months. Therefore, the message is clear: MIRM is a Strong Buy. Given the $49.50 average price target, shares could soar 150% in the next year. (See MIRM stock analysis on TipRanks)

PolyPid (PYPD)

Last but not least we have PolyPid, which develops locally administered therapies to improve surgical outcomes. Given the strength of its PLEX (Polymer-Lipid Encapsulation matriX) technology, which is a platform that is anchored in the surgical site to provide controlled and continuous delivery of medications, Raymond James thinks that it’s time to get in on the action.

The company only IPO’d in June, and it has already impressed firm analyst Elliot Wilbur. Looking at its D-PLEX100 product, it was granted Fast Track Designation by the FDA for the prevention of post abdominal surgical site infections (SSIs) in August. Fast Track Designation gives PYPD an advantage in that it increases the frequency of communication with the FDA. Additionally, it enables a rolling submission of the NDA, which allows the company to submit parts of the application as they are completed, expediting the review process.

“Although earlier approval is not guaranteed with the Fast Track Designation, the additional resources available to the company and the FDA recognition that D-PLEX100 has potential to address the unmet medical needs of the SSI market should be viewed as positives,” Wilbur stated.

In July, PYPD enrolled the first patient in its randomized SHIELD I (Surgical site Hospital acquired Infection prEvention with Local D-plex) trial, the first of two Phase 3 clinical trials evaluating D-PLEX100 in post-abdominal surgery (soft tissue) SSIs. The primary endpoint is prevention of deep or superficial surgical site infection, as determined by a blinded review committee within 30 days post abdominal surgery.

Wilbur expects the application of D-PLEX100 locally to the wound site combined with its extended release through thousands of bilayers of polymers and lipids to yield increased efficacy and safety over the current standard of care (SoC), which usually involves an antibiotic IV before an incision.

It should be noted that SHIELD I remains on track to enroll 600-900 patients across 60 centers globally, starting with centers in Israel and Europe before continuing to the U.S. “Management sees minimal anticipated impacts from the COVID-19 pandemic for this trial, and robust top line data (expected in late 2021) coupled with the benefits from the Fast Track Designation may be enough to obtain early approval for the drug,” Wilbur commented.

As SHIELD II is set to initiate in late 2020, with it serving as the second potential confirmatory Phase 3 trial, Wilbur sees an exciting opportunity on the table.

It should come as no surprise, then, that Wilbur sides with the bulls. In addition to an Outperform rating, he, the price target is left at $23, indicating 128% upside potential. (To watch Wilbur’s track record, click here)

What does the rest of the Street have to say? Other analysts echo Wilbur’s sentiment. PYPD’s Strong Buy consensus rating breaks down into 4 Buys and no Holds or Sells. With an average price target of $25.50, the upside potential comes in at 153%. (See PYPD stock analysis on TipRanks)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.