In recent years, the e-commerce scene has battled macro headwinds and rapidly changing consumer behavior. Undoubtedly, high rates and fears of anything worse than an economic soft landing have caused some consumers to cut back not just on discretionary goods but also on necessities by opting for the cheapest alternatives where possible.

Claim 55% Off TipRanks

Trade AMZN with leverageWith one rate cut likely in store in the second and economic growth that could pick up speed (perhaps via a productivity boost from AI), the consumer has reasons to be more hopeful. Whether it’s enough to take e-shopping sprees into overdrive, though, remains to be seen. Regardless, given that most discretionaries are better bought online these days, I’d argue the following e-tailers—PDD, AMZN, MELI— seem best equipped to power back.

Therefore, let’s use TipRanks’ Comparison Tool to check in with a trio of e-commerce titans that analysts have rated as Strong Buys.

PDD Holdings (NASDAQ:PDD)

PDD Holdings (formerly Pinduoduo) is a Chinese e-tailer that’s been riding high on its international e-commerce business Temu. Even if you’ve never shopped on Temu, you’re probably familiar with the platform and the ad that lets you “shop like a billionaire,” whereby you can shop freely without worrying too much about price. With obscenely low prices on a wide selection of goods, which come straight from the source, Temu seems to be winning the “race to the bottom” in terms of pricing for digital retailers.

With hard-to-match prices, a unique, “gamified” shopping experience that’s uniquely Chinese, and a world of growth opportunities, Temu stands out as the new e-commerce disruptor. All things considered, I remain bullish on PDD stock as it looks to extend its glorious two-year run that saw shares gain almost 150%.

Thanks to Temu, PDD has been able to one-up Chinese e-tailer Alibaba (NASDAQ:BABA) to become China’s largest e-commerce firm by market cap. With Alibaba in a horrid multi-year slump and Temu continuing to soar in popularity, the lead is likely PDD’s to keep for the long haul.

In the first quarter, Temu helped power PDD to 131% year-over-year sales growth. That’s the kind of growth that makes the added risks from investing in Chinese stocks forgivable. Nowhere else on Earth can you find that kind of growth for 19.7 times trailing price-to-earnings (P/E) or around 13 times forward P/E.

What’s even more remarkable is the user growth, with nearly 30 million global Temu app downloads as of February 2024. Clearly, the ads seem to be working. But the big question is if PDD can keep new customers continue “shopping like billionaires” for the long haul. I think they can with its rock-bottom prices amid inflation and the engaging “gamification” of the platform.

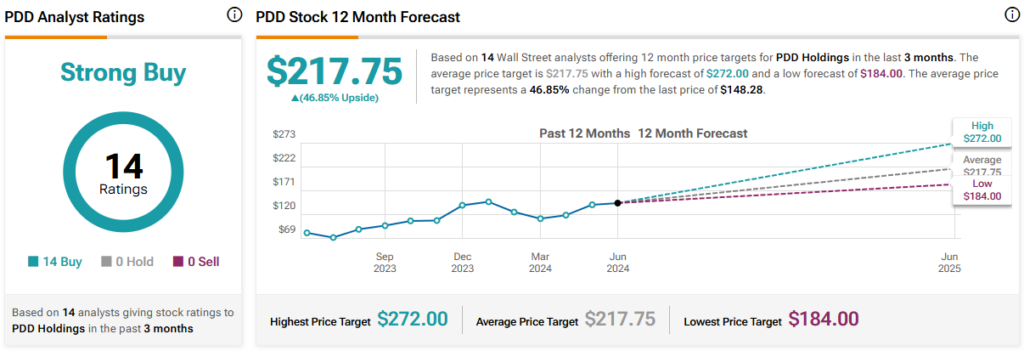

What Is the Price Target for PDD Stock?

PDD stock is a Strong Buy, according to analysts, with 14 unanimous Buys assigned in the past three months. The average PDD stock price target of $217.75 implies 46.9% upside potential.

Amazon (NASDAQ:AMZN)

If you want rock-bottom prices on goods, you head on over to Temu, but you’ll have to wait a long time for the delivery to arrive on your doorstep. Indeed, if you’re in the U.S., it could take weeks before your Temu order finally arrives. If time is of the essence and speed is what you need, you’ll probably want to take your business over to Amazon. The prices aren’t unreasonable on Amazon, but they are far from being the absolute cheapest for any given product category. I guess that’s the price you pay for blazing delivery speed.

Even if Temu can reduce delivery times by a few days or so, it will probably never come close to matching the speed of Amazon Prime deliveries. Indeed, a profound amount of logistical innovation is going on behind the scenes to make same-day shipping possible. Given this, I’m staying bullish on AMZN stock.

Additionally, Amazon is home to many authentic brand-name goods, many of which you can’t find over at Temu. In that regard, I don’t view Temu as a massive threat to Amazon’s e-commerce moat. That said, Amazon could lose some business to Temu in this environment, where consumers are price-sensitive and willing to wait weeks to get their product.

The good news for AMZN stockholders is that Temu and its fashionable Chinese e-commerce peer Shein have the attention of the Seattle-based e-commerce titan. Reportedly, Amazon drastically decreased fees for cheap clothing (articles going for under $20), a move that should help it hit back at fast-moving Chinese e-tailers as they look to disrupt the original disruptor in e-commerce.

What Is the Price Target of AMZN Stock?

AMZN stock is a Strong Buy, according to analysts, with 42 unanimous Buys assigned in the past three months. The average AMZN stock price target of $221.20 implies 20.2% upside potential.

MercadoLibre (NASDAQ:MELI)

MercadoLibre is an e-commerce and payments firm that serves Latin America. It’s pretty much the Amazon for Latin American nations—like Brazil, where the actual Amazon rainforest is located. Serving emerging markets can entail significant long-term growth potential, making MercadoLibre an e-commerce play for those who seek growth above all else. With a robust growth narrative and a dominant position in its circle of competence, I’m staying bullish on the stock despite its frothy multiple.

At writing, MELI stock goes for more than 70.9 times trailing P/E, which makes AMZN (51.6 times trailing P/E at writing) and PDD (19.7 times) look like relative bargains. That said, having a dominant position in higher-growth markets does entail a greater premium. Given PDD’s international presence with Temu, however, I’d argue PDD stock is, by far, a better option for value-conscious growth investors.

Looking ahead, analysts envision 2024 sales hitting $19 billion, up 25% year-over-year. With a similar growth playbook as a younger Amazon in markets that have far more growth potential, MELI stock seems like a name to watch or even buy on a pullback.

What Is the Price Target of MELI Stock?

MELI stock is a Strong Buy, according to analysts, with 12 Buys and two Holds assigned in the past three months. The average MELI stock price target of $1,921.82 implies 23.3% upside potential.

Conclusion

The e-commerce market looks primed for performance as the economy rises from an inflationary environment full of macro headwinds. Believe it or not, Amazon isn’t the growthiest pick of the pack these days when you expand your horizons to encompass some of the international e-tailers. Of the trio, analysts like PDD stock the most, as it has the highest implied upside potential (about 47%).