Cybersecurity company Palo Alto Networks (NASDAQ:PANW) will release its fourth quarter and Fiscal 2023 results after the market closes on Friday, August 18. While the unconventional timing of its earnings (companies usually do not hold conference calls after the market closes on Friday) has raised eyebrows, Wall Street analysts maintain a bullish outlook on the stock ahead of Q4 earnings.

Meet Samuel – Your Personal Investing Prophet

- Start a conversation with TipRanks’ trusted, data-backed investment intelligence

- Ask Samuel about stocks, your portfolio, or the market and get instant, personalized insights in seconds

Analysts‘ Opinions Ahead of Q4 Earnings

On August 7, RBC Capital analyst Matthew Hedberg lowered PANW’s price target to $255 from $277 and termed its earnings release timing “extremely unconventional.” This raises speculation about whether Palo Alto’s Fiscal 2024 guidance could miss the Street’s expectations, especially after its rival Fortinet (NASDAQ:FTNT) delivered weak financial results, noted the analyst. Nonetheless, Hedberg maintains a Buy rating on PANW stock. Along with Hedberg, BTIG analyst Gray Powell, and Barclays analyst Saket Kalia also reiterated a Buy on Palo Alto stock.

Commenting on its Fiscal 2024 outlook, Goldman Sachs analyst Gabriela Borges said that her industry conversations suggest softening trends in firewalls and cloud security. However, the trends in Cortex (its next-gen endpoint security solution) and Prisma Access (its next-gen cloud-delivered security platform) are still strong. Thus, the analyst expects PANW’s Fiscal 2024 revenue guidance to be in line with the Street’s expectations, while billings/FCF will miss the forecast. However, the analyst projects its earnings outlook to surpass analysts’ expectations.

Borges reiterated a Buy on Palo Alto stock on August 10 and expects it to outperform in the long term, led by its “unique competitive positioning” and “unit economics that will likely drive significant margin upside over the next 3 years.”

With this backdrop, let’s delve into Q4 expectations.

Q4 Top and Bottom Lines to Improve

While enterprises’ value consciousness persists amid macro uncertainty, analysts expect Palo Alto Networks to post revenues of $1.96 billion in Q4, up from $1.55 billion in the prior-year quarter. Also, its top line is expected to increase on a sequential basis, reflecting the ongoing strength in the service and subscription revenue.

Higher sales, a higher software mix in revenue, a reduction in supply chain costs, and efficiencies in customer support will support its margins and bottom-line growth in Q4. Analysts expect Palo Alto to post earnings of $1.29 per share, higher than its EPS of $0.80 in the prior-year quarter. Moreover, EPS is also likely to show improvement on a quarter-over-quarter basis.

Will PANW Stock Go Up?

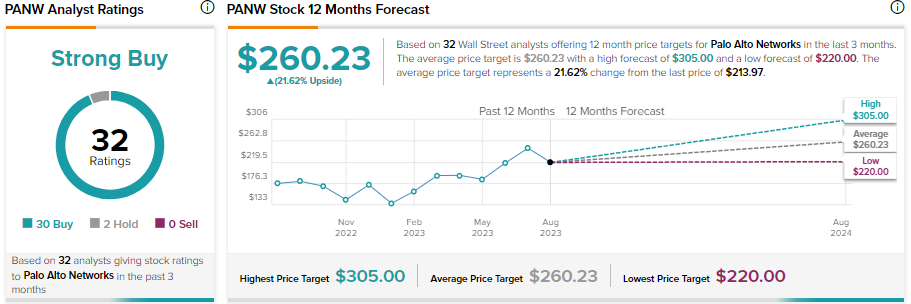

Palo Alto stock is up over 53% year-to-date. However, the stock lost more than 14% of its value in August as weak results from Fortinet and macro uncertainty led investors to book some profit in PANW stock. However, based on analysts’ average price target of $260.23, the stock offers an upside potential of 21.62% from current levels.

Further, with 30 Buy and two Hold recommendations, Palo Alto stock has a Strong Buy consensus rating on TipRanks.

Options Traders Expect a 4.71% Earnings-Related Move

Options traders are pricing in a +/- 4.71% move after PANW’s earnings report, which is lower than the previous quarter’s earnings-related move of 7.68% and the average 8.7% move in the last eight quarters. The anticipated earnings move is determined by computing the at-the-money straddle of the options closest to expiration after the earnings announcement.

Learn more about TipRanks’ option tool here.