It’s hard to believe, but it was just two years ago that OpenAI released ChatGPT to the world – and showed us all just how much potential there was in generative AI technology. Since the release, genAI has expanded its penetration into the tech world, streamlining digital advertising and online search, making translation matrices more efficient and accurate, automating the time-consuming processes that eat up so much of our productivity. It’s truly a tech revolution, and it’s ongoing.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Covering the AI tech sector from Wedbush, industry expert Daniel Ives sees AI as the key development in the software segment.

“Now it’s time for the broader software space to get in on the AI Party as we believe the use cases are exploding, enterprise consumption phase is ahead of us beginning in 2025, launch of LLM models across the board, and the true adoption of generative AI will be a major catalyst for the software sector and key players to benefit from this once in a generation 4th Industrial Revolution set to benefit the tech space. The AI Software era is now here in our view,” Ives opined.

Following this, Ives has picked out two stocks in software, Palantir (NASDAQ:PLTR) and Elastic (NYSE:ESTC), as the top AI stocks to take full advantage of the AI expansion. In Ives’ view, we’re at the point where the ‘revolution hits the next gear,’ and this is the time to buy in. Let’s take a closer look.

Palantir Technologies

First up is Palantir, an innovative data technology company co-founded by Peter Thiel in 2003. The company has built a tremendous reputation as a leader in data analysis and related disciplines, in part by combining automated computer systems with human intuition, to bring out the best of both. It’s an approach that is naturally conducive to integrating AI technology, and Palantir has also been an early adopter and innovator in AI, particularly generative AI.

Getting down to basics, Palantir’s product offerings include a full set of data analytic tools, while the company also has a dedicated AI platform, dubbed AIP. The company has realized a solid qualitative gain in the last two years, as AI technology has both expanded and advanced. The advent of generative AI has been especially beneficial to Palantir, particularly its use in natural language processing and large language models.

That is because Palantir offers its AI-powered data tools to customers with natural language interfaces, as often as possible in the customer’s native language. The company boasts that there is no need for users to learn complex computer coding languages in order to get the most mileage from Palantir’s tools; prompts and requests can be entered in ordinary syntax, and are received the same way.

These advantages – as well as the company’s reputation for quality – are at the root of Palantir’s success. The AIP is finding acceptance in both the private sector and in government agencies. In recent weeks, the company has chalked up two more important such wins. On November 7, the company announced a partnership with Anthropic and AWS to provide access to the Claude 3 and 3.5 AI models, now available on AWS, to various US intelligence and defense agencies. And on November 13, the company announced it had renewed its multi-year enterprise agreement with the giant mining conglomerate Rio Tinto Group.

Turning to the financial results, Palantir released its 3Q24 earnings on November 4 and the numbers came in ahead of expectations. Revenues were reported at $725.52 million, up 30% year-over-year and almost $22 million better than had been expected. The non-GAAP EPS, of 10 cents, was a penny above the forecast. During the quarter, Palantir grew its customer count by 39% year-over-year, and closed 104 deals valued at $1 million or more. The company finished the quarter with total cash and liquid assets worth $4.6 billion.

Shares in Palantir, which had been climbing steadily all year, jumped sharply after the earnings report, gaining almost 25% in 24 hours. Year-to-date, PLTR stock is up an impressive 274%.

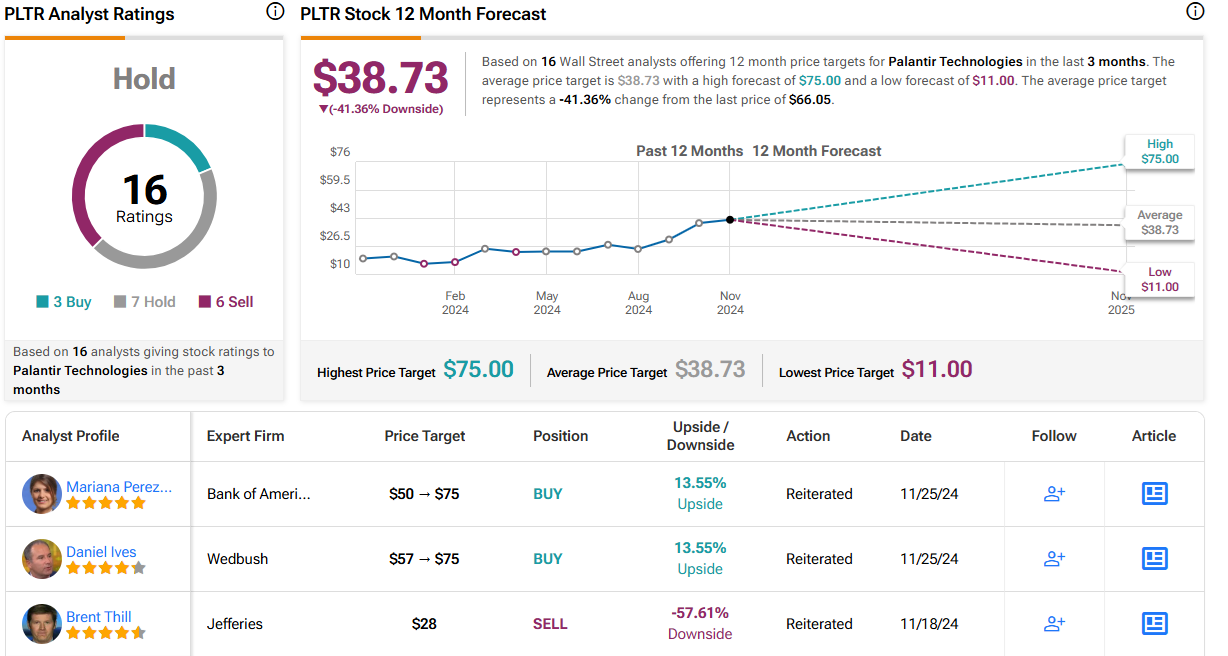

While the stock’s steep recent gains have some analysts fearing that Palantir is overvalued, Wedbush’s Ives remains upbeat. In his recent note on the company, Ives writes, “We are raising our price target on Palantir from $57 to $75 reflecting our increased confidence in the game-changing AIP strategy with use cases for AI taking hold over the next 12-18 months. The Messi of AI growth story will see unprecedented demand as more enterprises realize the value of PLTR’s entire product suite with more AI use cases.”

The analyst’s stance comes with an Outperform (Buy) rating, and his newly raised price target implies a one-year gain of 13.5%. (To watch Ives’ track record, click here)

Overall, it’s safe to say that the overvaluation worries are stirring up some caution on Wall Street. The shares have a Hold consensus rating, based on 16 recent reviews that include 3 to Buy, 7 to Hold, and 6 to Sell. The stock is priced at $66.05 and its $38.73 average target price suggests that the shares will slip by 41% in the coming year. (See PLTR stock forecast)

Elastic

The second stock we’re looking at, Elastic, fills a vital role behind the scenes in the tech and business worlds. The modern digital economy runs, in large part, on data – and that means that everyone needs and maintains large databases. But accessing and using that data is another matter; there’s no point in having all the information if you can’t put it to work. Elastic offers enterprise customers a software-as-a-service platform featuring local data search capabilities, designed to put customers’ databases to work.

The platform is based on both cloud computing and generative AI tech; from the user’s point of view, Elastic’s service requires no major infrastructure but still allows for real-time data search solutions. The company’s software solves user problems in data searching, observability, and security, and the more recent versions and updates include tighter integration of generative AI tech and large language models. The company also offers its customers access to Search AI Lake, serverless generative AI that can perform on-demand searches in real-time, featuring low latency and enterprise scaling.

While Elastic is not a household name, the company is well-known in its niche – and its customer base includes such big names as Cisco, T-Mobile, and Land Rover. While the service is popular and in high demand, the company did see a setback in late summer when it pared back its full-year revenue guidance on worries about a lower volume of customer commitments; the stock fell by 26.5% in response. More recently, however, the shares got a boost from the fiscal 2Q25 earnings report.

In the quarter, Elastic showed a top line of $365 million, some $10.7 million better than anticipated and up more than 17% year-over-year. The non-GAAP earnings came to 59 cents per share, beating the forecast by 21 cents. For the full fiscal year 2025 (which ends this coming April 30), Elastic is now predicting revenues between $1.451 billion and $1.457 billion – bringing the guidance back up from the $1.436 billion to $1.444 billion range it had reduced it to in the fiscal Q1 report. The stock jumped almost 15% after the fiscal 2Q25 release.

Like the recent investor sentiment, Daniel Ives is also upbeat on Elastic. He likes the company’s general position, and writes of it, “ESTC looks to capitalize on growing AI demand for its platform approach with more customers looking to consolidate spend from legacy vendors to next-gen migration while accelerating its express migration program. This is the right time at the right place for Elastic…”

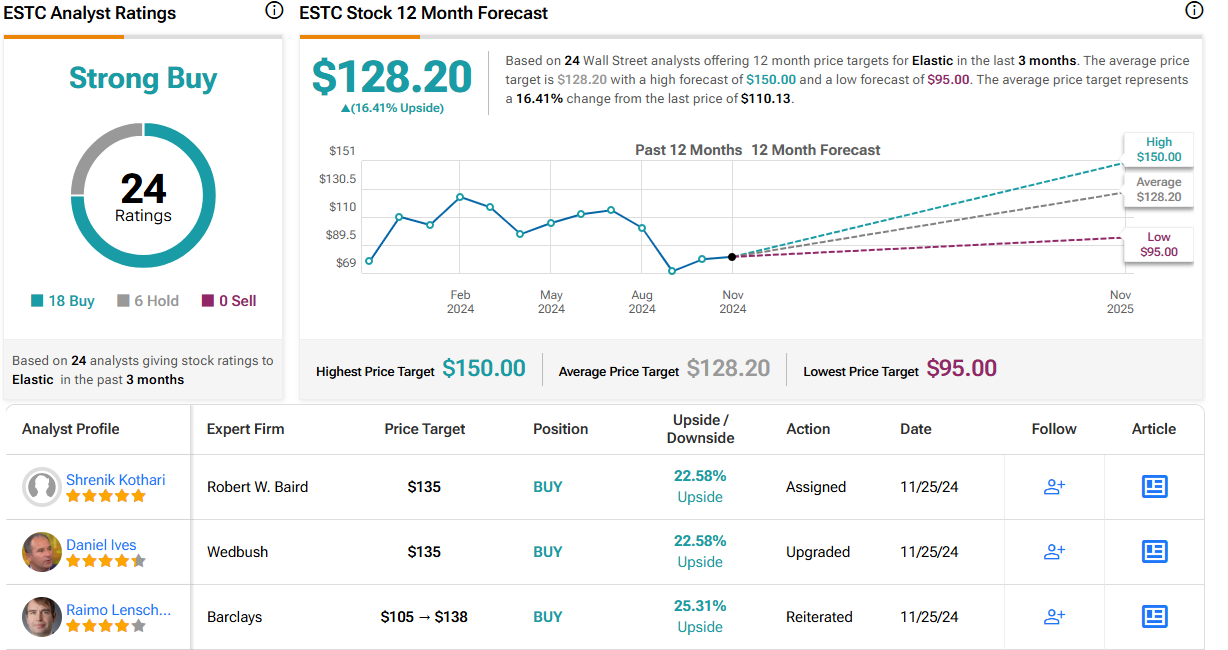

These comments support Ives’ upgrade of the shares to Outperform (Buy). His price target of $135 suggests that the stock has a 22.5% upside potential on the one-year horizon.

There are 24 recent analyst reviews available for Elastic, and the 18 to 6 breakdown favoring Buy over Hold, gives the stock its Strong Buy consensus rating. The shares are priced at $110.13, with a $128.2 average target price pointing toward an upside of 16.5% in the next 12 months. (See ESTC stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.