Shares of graphics processor manufacturer Nvidia (NASDAQ:NVDA) more than tripled in 2023 amid surging interest in artificial intelligence (AI). Nvidia’s chips became a go-to product for many AI applications, used in the training and utilization of large language models and other systems. The question for many investors this year is whether or not Nvidia can maintain that upward trajectory this year.

Claim 30% Off TipRanks

New trading tool for NVDA bears

Analysts across Wall Street answer that question with a resounding “yes.” I join them in their optimism for Nvidia’s performance, going forward. The age of AI—and, with it, the massive demands for computing power—is just beginning and likely to only expand at this point. Nvidia enjoys tremendous brand strength and an advantageous position relative to other companies trying to break into the space.

The firm also has plans to more than triple its free cash flow in the coming years, opening up untold possibilities for new product development. This is on top of a promising pipeline of upcoming products already in the works. Below, we take a closer look at why Nvidia still looks attractive.

Nvidia and AI

An estimated 80%+ companies around the world are expected to use generative AI by 2026, bringing the AI semiconductor market to nearly $120 billion by 2027. Nvidia is well-positioned to capitalize on this increase in demand. The company is predicted to hold 85% of the market share for the AI chip space into 2024, according to Srini Pajjuri, an analyst at Raymond James.

Nvidia’s high-powered enterprise graphics processing units (GPUs), which typically cost tens of thousands of dollars and are installed in systems with several GPUs working simultaneously, are in demand by tech companies but remain out of reach for most consumers. Fortunately for individuals looking to explore AI, Nvidia has solutions on the way.

On January 8, Nvidia announced the launch of the RTX 4060 Super, RTX 4070 Ti Super, and RTX 4080 Super, three GPUs for use in personal computers, which also have the capacity to run generative AI programs. Priced at $999 or less, these GPUs could help to expand Nvidia’s AI chip reach into the consumer market.

Hardware sales have been Nvidia’s major revenue booster in recent quarters, helping drive its forward P/E ratio to around 27x, while competitors like Advanced Micro Devices (NASDAQ:AMD) are in the high 30s. However, revenue gains may not necessarily be the reason why a P/E ratio is lower, so it’s important for investors to look at multiple factors.

Intense Competition, but Nvidia Has the Advantage

Undoubtedly, Nvidia’s competition for the AI market will continue to heat up in the months to come. Rivals like Intel (NASDAQ:INTC) and AMD are eager to claim some of the growing market for themselves. So far, Intel has focused on GPUs at a lower price point than Nvidia’s. With the launch of Nvidia’s new AI-capable GPUs at a lower cost, investors may want to watch how Intel responds.

Nvidia may also have an advantage in the massive Chinese market. The company reportedly plans to initiate production on specially-designed chips for China that comply with U.S. export regulations in Q2. China makes up about a third of the global semiconductor market.

Free Cash Flow Plans

Bank of America (NYSE:BAC) expects that Nvidia’s growing revenue could help it generate $100 billion in free cash flow in the next two years. The company’s free cash flow for the last two years was under $30 billion.

Even factoring in potential buybacks, Nvidia is likely to have tens of billions of dollars at its disposal. This capital could be strategically invested in the development of innovative products or potentially used to acquire companies offering products and services outside of the company’s wheelhouse. Software and subscription-based AI services could be a target.

Reasons for Caution

Despite its massive momentum and strong prospects, investors should be aware of the risk factors associated with Nvidia. The company’s revenue profile is heavily concentrated in hardware sales. A major materials shortage or other disruption could leave Nvidia in a difficult position.

While the company has revamped some of its products to comply with export law so that they can be sold in China, some leading Chinese tech firms have signaled a lack of interest. One reason could be that the reworked chips are slower than Nvidia’s mainstream counterparts.

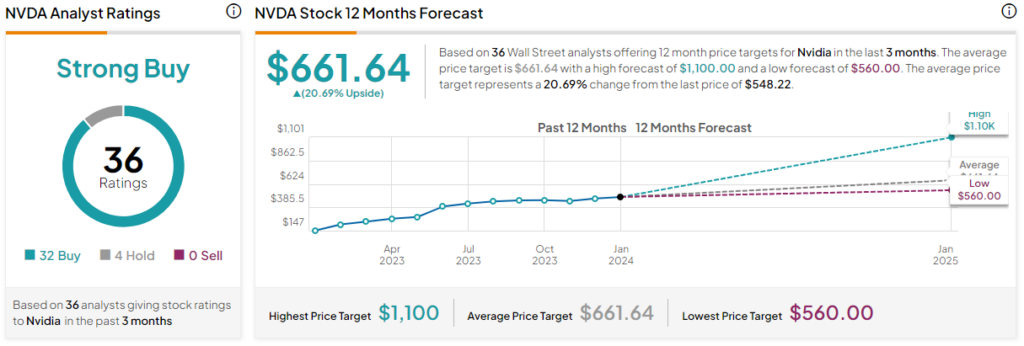

What is the Price Target for NVDA Stock?

On TipRanks, Nvidia enjoys a Strong Buy consensus rating based on 32 Buys, four Holds, and zero Sells assigned by analysts in the past three months. At $661.64, the average Nvidia stock price target implies almost 21% upside.

Conclusion: There’s Still Room for Growth

All told, Nvidia seems to be in a great position to continue to benefit from global AI demand. It has a strong pipeline of new products and should be able to generate the cash to continue to innovate. For these reasons, it’s no surprise that analysts rate the stock a Strong Buy. Nvidia was one of the best-performing stocks of 2023, and analysts believe its massive bull run isn’t over yet.