We’re almost halfway through 2025, and the overriding theme of the markets this year has been volatility.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

From President Trump’s barely-precedented non-consecutive second term to the mercurial President’s on-again, off-again tariff policy and trade negotiations, to the explosive expansion of the Middle East war – the markets have faced an almost non-stop series of turbulent events.

Even so, Wall Street isn’t standing still. Despite the volatility, major banks are actively searching for high-conviction plays for the months ahead. Morgan Stanley, one of the best-known names on Wall Street, has pinpointed two stocks as its ‘top picks’ – tickers it believes are well-positioned to beat the market as the year progresses.

Using the TipRanks platform, we’ve looked up the broader Wall Street view on both of Morgan Stanley’s picks – and the verdict is in: both carry Strong Buy consensus ratings. Let’s take a closer look at what makes them stand out right now.

Chart Industries (GTLS)

The first of Morgan Stanley’s top picks that we’ll look at is Chart Industries, a company that provides essential ancillary services in the energy industry – specifically, to the natural gas sector. The company’s chief business operations lie in the field of cooling and compression, where Chart provides equipment and support needed by the Liquefied Natural Gas (LNG) segment. In addition, the company works in the industrial gas field, and provides solutions for a variety of industrial sectors – aerospace, cement, data centers, hydrogen energy, mining, and more.

Chart’s activities have a global footprint, and the company has a presence on all the major continents. In an important move, announced earlier this month, the company indicated that it has entered an agreement with Flowserve Corporation to conduct a ‘merger of equals.’ Flowserve is a global leader in industrial process technologies, making it a good fit for Chart’s existing operations. The combined entity will have its headquarters in Dallas, Texas, and will maintain important offices in Atlanta and Houston, supporting ops in more than 50 countries. The transaction, which is expected to close during 4Q25, will be conducted on an all-stock basis, and create a firm with an approximate enterprise value of $19 billion.

Looking at Chart’s Q1 results, the last quarter before the merger announcement, we find that the company generated $1 billion in revenue, a total that was up 5% year-over-year although it missed the forecast by a razor-thin $1.11 million. Chart’s $1.86 non-GAAP EPS was 3 cents per share better than had been expected. As noted, Chart finished the quarter with a strong work backlog.

The breadth of Chart’s activities is clear from the company’s reported 1Q25 backlog. Chart had a work backlog of $5.14 billion, the first time that metric had exceeded $5 billion. The company reported strong order activity in the space exploration, nuclear, HLNG vehicle tanks, and marine sectors – showing that its services are in high demand across a broad range of industries. The company’s strongest business segments in Q1 were Specialty Products, which saw orders worth $487.7 million, and Repair, Service, and Leasing, which saw orders worth $454.6 million.

Morgan Stanley analyst Daniel Kutz covers this stock, and starts his review with an upbeat summary of the Flowserve merger, writing, “Designating GTLS as our Top Pick: Deal synergy targets are compelling if realized —particularly the guided commercial synergy target of a +200bps top line CAGR boost. Yet, as noted, some question whether these targets are achievable, and out of conservatism, we only give partial credit for this target in our forecasts. However, we argue that GTLS’s organic growth prospects are already compelling, and frankly, think that if GTLS (and/or GTLS + FLS PF) come close to the growth targets these companies have laid out, that GTLS shares are undervalued (meaningfully).”

Looking ahead, Kutz explains why he sees GTLS shares as a solid opportunity, adding to his comments, “Additionally, at this point in the cycle and against a macro backdrop mired with uncertainty, we maintain our preference for exposure to portfolios that have relatively outsized duration and defensive/diverse characteristics offering idiosyncratic growth opportunities, including: (1) gas > oil, (2) opex (i.e., upstream O&G prod’n) > capex, (3) digital solutions, (4) new energy, and (5) non-upstream, and GTLS (as well as GTLS + FLS PF) screens among the best in our coverage against these preferences.”

Getting down to basics, Kutz puts an Overweight (i.e., Buy) rating on GTLS shares, with a $225 price target that suggests a robust 12-month upside potential of 58%. (To watch Kutz’s track record, click here)

This stock has picked up 15 recent analyst reviews, including 12 Buy and 3 Holds, for a Strong Buy consensus rating. The shares are currently trading for $142.58 and the $206.31 average target price implies a gain of 45% in the year ahead. (See GTLS stock forecast)

Coca-Cola Company (KO)

Next on our list of Morgan Stanley top picks is the Coca-Cola Company, one of Wall Street’s venerable blue chips. Coke’s iconic logo and bottles together make up one of the world’s best-known brands, an incalculable advantage in the crowded food-and-beverage space. The company was founded in 1892 in Atlanta, Georgia, where it still maintains its headquarters.

Coke is best known for its eponymous soda brand, which has been the leader in the cola niche for decades. Over the years, the company has expanded through the development or acquisition of new and existing soft drink brands, and has not been afraid to branch out in unexpected directions – into juices, coffee, and health drinks, for example. Today, Coca-Cola is the world’s most valuable beverage company, with a market cap of more than $296 billion.

Back in 2020, Coke made an acquisition that is proving prescient today. The company spent $980 million that year to fully acquire Fairlife (also called fa!rlife), the ultra-filtered milk brand it had founded as a joint venture with Select Milk Producers in 2012. Fairlife specialized in filtered milk drinks that have reduced lactose and sugar but still retain the protein content. Since Coke fully acquired the company, Fairlife’s sales have expanded – and last year, Coke broke ground on a $650 million Fairlife production facility in New York State. The move represents a strong push into the expanding market for health and wellness foods.

Turning to the company’s financial results, we find that Coke’s revenue in 1Q25 – the last period reported – came to $11.1 billion. This figure was down 2% year-over-year, hit by a headwind in the form of refranchising in bottling operations. At the bottom line, the company saw a non-GAAP EPS of 73 cents, beating the forecast by a penny per share. On May 1, Coke declared its Q2 dividend at 51 cents per common share, for a July 1 payment. Coke is well known as a reliable dividend stock, and has been gradually raising the payment for more than a decade. The current dividend annualizes to $2.04 per common share and gives a forward yield of 3%.

For analyst Dara Mohsenian, who covers this Wall Street stalwart for Morgan Stanley, the three keys here are Coke’s ability to control its pricing, its long-term growth potential, and the strength of the Fairlife brand. Mohsenian says of Coke’s future and its stock, “We see sustained MSD OSG [Mid-Single-Digit Organic Sales Growth] at KO longer term, which is peer-leading in a weaker CPG [Consumer Packaged Goods] topline growth environment, with Coke in the 5% range long term, above peers coalescing around/ averaging ~3%. We see Coke as offering numerous advantages on OSG (organic sales growth), including: 1) Much stronger sustained pricing power. 2) Solid and higher than peers historical volume growth, despite outsized pricing, which drives our comfort on forward sustainability as pricing growth drops off. Volume growth is fueled by market share gains, outsized innovation, higher and more effective marketing, superior execution than peers, which all should sustain. 3) Durable market share gains, with Coke’s competitive advantages rising given peer struggles in ancillary areas (PEP in snacks and KDP in coffee). 4) Growth contribution from the ‘fa!rlife’ acquisition.”

At the bottom line, Mohsenian comes to an upbeat conclusion, going on to write, “We can simplify our thesis: Our Coke OW call boils down to the notion that one can buy Coke at the same multiple as peers, but with durably higher long-term OSG. We are also moving KO to our top pick in beverages (previously time stopped out), although it has already been our favored stock in beverages and across our coverage.”

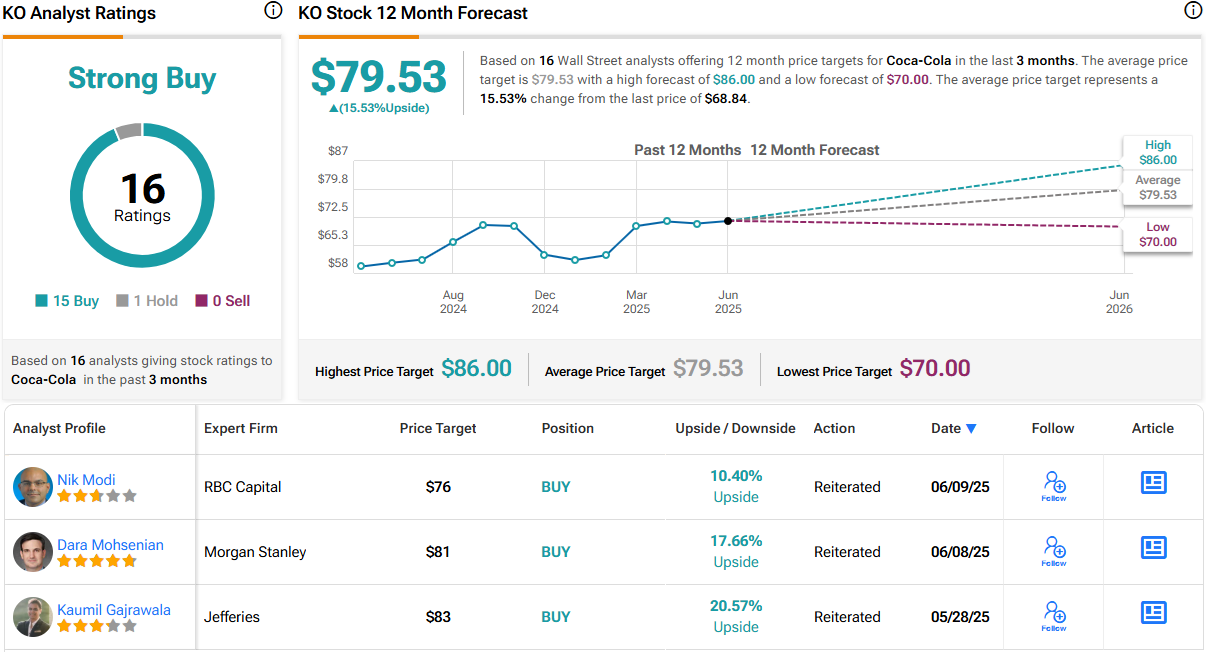

All of this adds up to an Overweight (i.e., Buy) rating from the analyst, whose $81 price target points toward a sound one-year upside potential of 18%. (To watch Mohsenian’s track record, click here)

It’s clear the bulls are driving the narrative here, as the 16 recent reviews include 15 to Buy and 1 to Hold for a Strong Buy consensus rating. The shares are priced at $68.84 and have an average target price of $79.53, suggesting that KO will appreciate by 15.5% over the next year. (See KO stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.