Microsoft (MSFT) is at the forefront of the AI arms race, boasting an exceptional business model that consistently generates substantial and growing free cash flow. With the company’s current valuation appearing fair, now may be an opportune time to buy its shares. I have a 12-month price target of $482.40, while the average Wall Street price target is $503.27. Therefore, I am decidedly bullish on MSFT stock, both in the short and long term.

Claim 30% Off TipRanks

Forget margin or options. Here's how the pros trade AMZNMicrosoft Should Not Be Underestimated in AI

I am particularly bullish on Microsoft because it is widely recognized as a global leader in AI. Based on my analysis, Microsoft is likely at the forefront of the AI market, as demonstrated by its $10 billion commitment to ChatGPT creator OpenAI. This investment has enabled groundbreaking products like Microsoft Copilot, which integrates AI into its Office suite to improve productivity for millions of users. Notably, ChatGPT reached one million users in less than five days and 100 million users in about two months—a feat of unprecedented growth.

Furthermore, Microsoft, alongside partners like BlackRock (BLK), is involved in the Global AI Infrastructure Investment Partnership, which aims to raise up to $100 billion to develop data centers and energy infrastructure supporting AI operations. This partnership aligns with Microsoft’s long-term strategy to lead the global AI industry. In the medium term, investors can anticipate growth driven by AI integrated into Microsoft’s cloud services (Azure).

However, the industry is crowded with Big Tech competitors, including Google (GOOGL), Amazon (AMZN), and the unexpected outperformer Meta (META). Among these, I consider Meta to pose the most significant competitive threat to Microsoft, as it has open-sourced its frontier AI models, enabling third parties to iterate on the source code and advance the technology more rapidly—a strategy Microsoft has not adopted.

MSFT Stock Is Attractive for Growth Investors

One of the primary reasons I view Microsoft as an outstanding long-term investment is its robust history of generating substantial free cash flow. At the time of this writing, the company’s free cash flow margin exceeds 30%, with free cash flow rising from $15.9 billion in 2009 to $74.1 billion in the last trailing 12 months. This financial strength provides management with the resources to make strategic growth investments.

While Microsoft may not appear as a value investment, it is reasonably priced, in my view, given its consistent revenue and earnings growth, which is likely to continue in the foreseeable future. I estimate a 13% normalized EPS growth over the next 12 months. Based on this forecast, I hold a price target of $482.40, estimating the stock will trade at a non-GAAP P/E ratio of approximately 36.

Looking further ahead, I expect Microsoft to achieve an average annual return of 15% over the next five to 10 years. While this outlook requires purchasing the stock at a fair valuation, I believe the current price presents an opportunity. The company’s forward non-GAAP P/E ratio is only a 6.5% premium over its five-year average, while its forward diluted EPS growth rate has expanded by nearly the same amount, at 5.8%.

MSFT Faces Potential Headwinds in the Long Term

One potential challenge to Microsoft’s long-term growth in AI is that its adoption may be cyclical. Currently, demand for AI systems is high, prompting Microsoft and other Big Tech companies to invest heavily in data center expansion. However, when the current trend peaks—potentially due to macroeconomic constraints—a slowdown in growth is likely. According to the TipRanks Risk Analysis tool, Microsoft faces 32% of its risk from legal and regulatory factors, which is above the sector average and could impact its AI operations due to increased scrutiny on data privacy and AI governance.

Given this outlook, I anticipate some volatility in Microsoft’s growth trajectory over the long term, though it may be less pronounced than that of semiconductor companies like NVIDIA (NVDA). Periodic price and valuation dips coinciding with temporarily lower growth rates could provide more attractive buying opportunities as sentiment fluctuates.

There is also a risk that Microsoft and other Big Tech players could over-invest in AI infrastructure. With 21% of its risk related to Tech & Innovation, Microsoft’s heavy investment in AI-driven initiatives, including data center infrastructure, could result in lower-than-expected returns if industry growth does not meet expectations. This may impact free cash flow margins in the medium term, contributing to further volatility.

Is Microsoft a Buy, Hold or Sell?

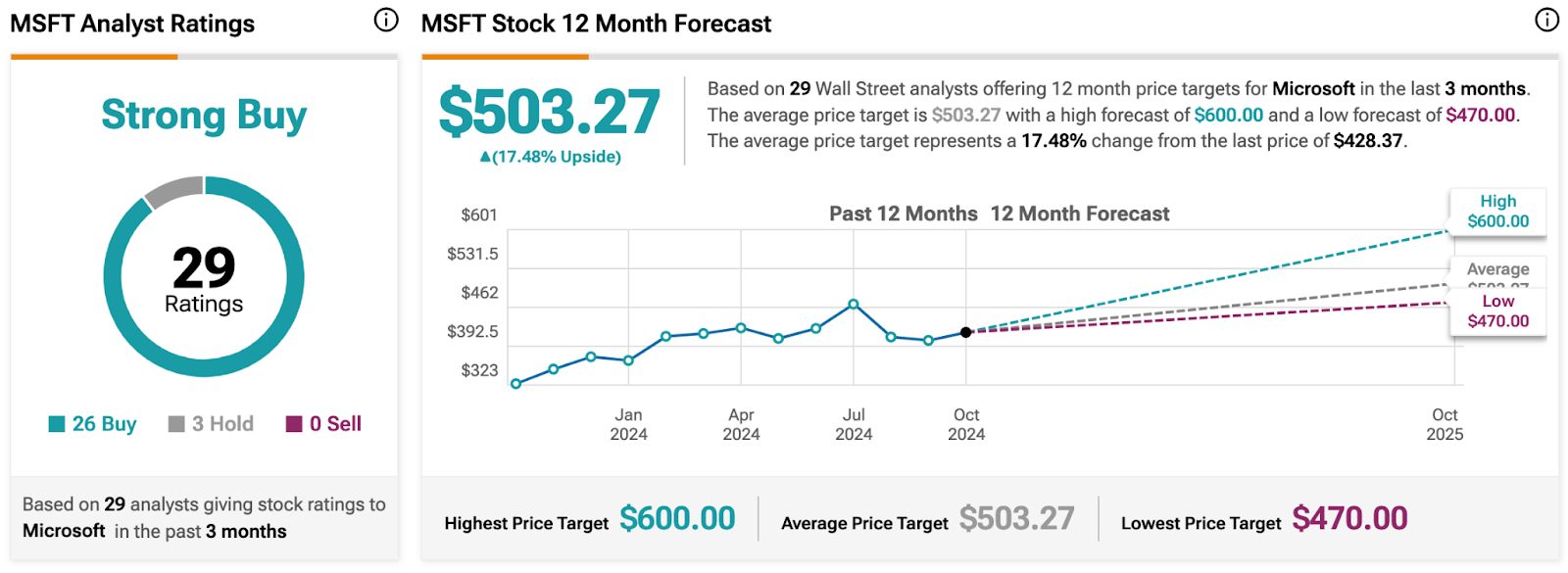

On Wall Street, Microsoft receives a broadly positive outlook, with 26 Buy ratings, three Hold ratings, and no Sell ratings. The average MSFT price target is $503.27, reflecting a 17.5% upside potential over the next 12 months.

This positive sentiment reinforces the view that now may be a prudent time to invest in Microsoft, given its strong market position and leadership in AI.

Key Takeaway: Microsoft Is a Leading AI Investment

I am bullish on Microsoft due to its leadership in AI, supported by its significant stake in OpenAI. Additionally, the company has demonstrated consistent free cash flow growth, which is likely to strengthen its market leadership over the long term. Although Meta is a strong competitor in the AI landscape, I remain confident that Microsoft holds the leading position. Based on my analysis, MSFT stock is a Buy.