Among the blue-chip names in the technology sector, Intel (INTC) stock has been an underperformer in the last 12-months. During this period, the stock has remained sideways.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Of course, the weakness in INTC stock has been due to growth concerns. However, it seems that the stock is undervalued at a price-to-earnings-ratio of 9.8.

I am bullish on INTC stock for 2022 and I believe that a major sentiment reversal is around the corner. Let’s discuss the possible catalysts for stock upside. (See Analysts’ Top Stocks on TipRanks)

Intel recently announced the intent to take Mobileye public. Mobileye has a leading market share in driver-assistance and autonomous driving solutions.

In 2017, Intel acquired Mobileye for a consideration of $15.3 billion. The initial public offering can potentially value Mobileye in excess of $50 billion. With a likely IPO of Mobileye in mid-2022, there is an impending value unlocking for shareholders.

It’s worth noting that Mobileye is expected to deliver revenue growth of more than 40% for 2021. If this growth trajectory sustains, valuations can be significantly higher in the next few years. The spin-off has the potential to create value and INTC stock is likely to trend higher.

Gradual Push for Growth

For Intel, gaining market share is unlikely to come overnight. Intel CEO Patrick P. Gelsinger believes that the turnaround effort is a five-year job. However, markets discount the future and with positive developments, INTC stock is likely to trend higher.

In September 2021, Intel announced that the company had commenced the construction of two leading-edge chip factories in Arizona. Intel will be investing $20 billion in these factories. With a global chip shortage, it’s possibly the best time to ramp up investments.

Intel has also pledged to invest $95 billion in Europe’s chip-factory expansion. Shortages of car chips have been a big headwind for EV companies in 2021. European expansion will be targeted towards addressing this demand-supply gap.

For 2022, Intel expects to incur capital expenditures in the range of $25 billion to $28 billion. Furthermore, the company is targeting higher investments in subsequent years. This is likely to translate into revenue and earnings upside.

It’s important to note that Intel is well positioned for big investments. For the first nine months of 2021, the company reported operating cash flows of $24 billion. This would imply an annualized cash flow potential in excess of $30 billion.

Therefore, even with an average annual investment of $25 billion to $30 billion in the next few years, Intel is positioned to deliver free cash flows. INTC stock already offers a healthy dividend yield of 2.8%. With investments likely to deliver earnings upside, Intel seems like an attractive dividend growth stock.

Another point from the growth perspective is innovation. Intel already has a strong innovation pipeline, with products that include the company’s first ASIC-based IPU. Additionally, the next generation discrete GPU for gaming is slated for launch in Q1 2022.

Wall Street’s Take

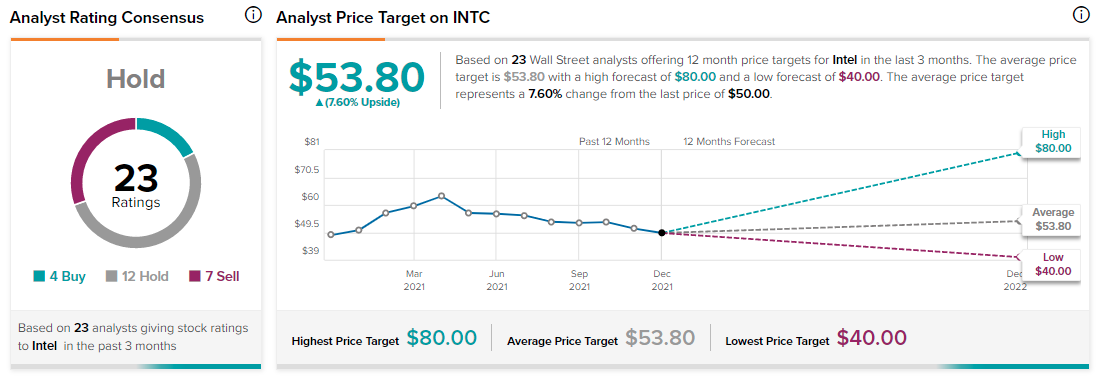

Turning to Wall Street, Intel has a Hold consensus rating, based on four Buys, 12 Holds, and seven Sell ratings assigned in the past three months. The average Intel price target of $53.80 implies 7.6% upside potential.

Bottom Line

Advanced Micro Devices (AMD) might have taken away market share from Intel in the last few years. However, Intel seems to be fighting back with capital investments and a pipeline of innovation.

A turnaround will not come instantly, but the transformation is likely to take INTC stock higher.

In the near term, Mobileye’s IPO serves as another catalyst. Therefore, INTC stock looks attractive at a forward P/E of less than 10.

Besides the potential for stock upside, Intel also offers the possibility of dividend growth in the coming years.

Disclosure: At the time of publication, Faisal Humayun did not have a position in any of the securities mentioned in this article.

Disclaimer: The information contained in this article represents the views and opinion of the writer only, and not the views or opinion of TipRanks or its affiliates Read full disclaimer >