We rarely give much thought to the power outlet on the wall, yet nearly everything in our modern lives depends on it. From appliances and lighting to computers, entertainment, climate control, and more – all draw on that steady flow of electricity. And that’s just within the home. In cities, where industry, utilities, and communication networks operate on a massive scale, demand for electricity multiplies rapidly. Even if the broader transition away from fossil fuels toward carbon-neutral electrification stalls, electricity will remain a critical resource with demand that shows no sign of easing.

Claim 30% Off TipRanks

Forget margin or options. Here's how the pros trade CEGA new report from Scotiabank analyst Andrew Weisel lays out the case for turning high electrical demand into a bonanza for investors.

“We have a bullish fundamental view on the group, driven by a robust outlook for electricity demand coupled with downside protection and strong balance sheets/cash flow generation,” the analyst said. “Demand is coming not only from high-profile data centers and electrification, but also from manufacturers and other sources, and though competition is high, both among IPPs and with regulated utilities, we believe that there is more than enough to go around, even assuming that macro forecasts are meaningfully overstated and even if the economy ultimately slows some. Importantly, the IPP paradigm has shifted, allowing investors to focus on upside opportunities rather than downside risk.”

Weisel follows up on this stance with recommendations on two utility-scale power producer stocks. According to the data at TipRanks, both get Buy ratings from the Street and present double-digit upside potentials. Here’s a closer look.

Constellation Energy (CEG)

The first stock we’ll look at, Constellation Energy, is the largest producer of carbon-free power in the US market. The company describes itself as a leader in providing competitively priced power supplies and energy products on the retail market, to homes and businesses. The company, set up as an independent entity in 1999, currently boasts a market cap of nearly $106 billion and is headquartered in Baltimore, Maryland.

Today, Constellation generates more than 32,400 megawatts of power from nuclear, wind, solar, hydroelectric, and natural gas sources. As noted, this portfolio puts the company in the #1 spot among carbon-free producers; it also accounts for approximately 10% of the carbon-free electricity generated in the US. The company supplies power to millions of customers in the residential and commercial sectors, as well as to institutional customers and public sector agencies. Approximately three-fourths of the Fortune 100 companies are on Constellation’s customer list.

In addition to its clean energy portfolio, Constellation also generates 12,000 megawatts of power from other fuel assets. This traditional generation capacity allows the company to maintain service at times of baseload, intermediate, and peak power generation demand.

Constellation is a major provider of nuclear-powered electrical generation in the US. Its nuclear fleet includes plants in Illinois, New York, and the mid-Atlantic region, and the company is part of the restart efforts at the Three Mile Island facility in Pennsylvania. This power plant was the site of the most serious nuclear accident in US history, and Constellation is working to restart Unit 1 at the site. The unit, renamed the Crane Clean Energy Center, is expected to provide new jobs, boost grid reliability, and enhance the carbon-free power available in the region. The company reports that the restart efforts are ahead of schedule and that Crane is set to return to operation in 2027.

When we turn to the company’s financial results, we find that Constellation beat the forecasts at both the top and bottom lines in 2Q25, the last period reported. The company’s $6.1 billion in total revenue was $1.22 billion better than had been expected and was up 11.5% year-over-year. At the bottom line, the company realized a non-GAAP EPS of $1.91, beating the estimates by 9 cents per share. The power company’s stock has outperformed the broader markets this year and is up 46.5% for the year-to-date.

For Scotiabank’s Andrew Weisel, the main point here is simply that Constellation has a strong position in a high-demand industry. He writes of the stock, “Our top pick overall is CEG, which we believe offers among the fastest growth… CEG is an industry leader on almost every metric in a sector seeing unprecedented demand, with a best-in-class fleet and track record of innovation and execution on data center contracts and organic growth initiatives; we view it as a ‘utility-like’ IPP (in the best sense).”

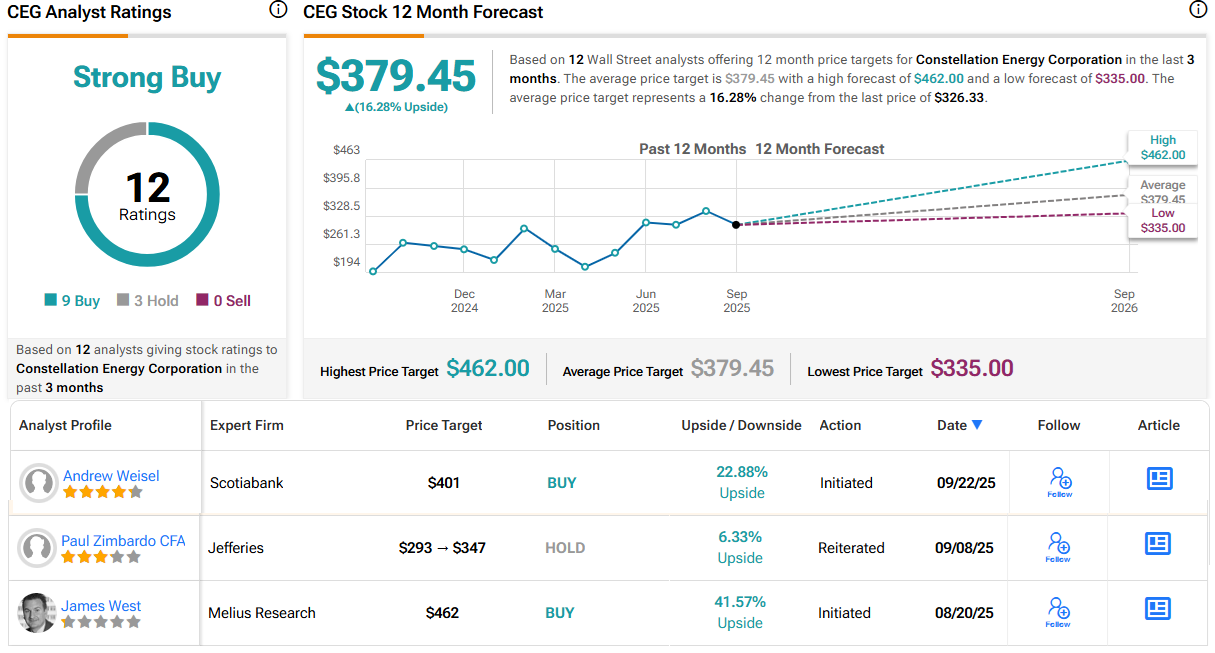

Putting this stance into quantifiable terms, Weisel rates CEG shares as Outperform (i.e., Buy), with a price target of $401 that suggests a one-year gain of 23%. (To watch Weisel’s track record, click here)

Overall, Constellation Energy’s stock gets a Strong Buy rating from the analyst consensus, based on 12 recent reviews that include 9 Buys and 3 Holds. The shares are currently trading for $326.33, and their $379.45 average target price implies a 12-month upside of 16%. (See CEG stock forecast)

NRG Energy (NRG)

Next on our list is NRG Energy, a Houston-based firm that provides power to residential, business, and industrial customers in an array of markets in both the US and Canada. Like CEG above, NRG Energy has seen strong share price gains this year that have outpaced the broader markets; NRG shares are up 83% since January. The company’s market cap stands at $32 billion, and NRG boasts more than 8 million residential and business customers, and has a power generation capacity of 13 gigawatts.

NRG takes note of an important fact that lies behind the rise in power demand: that making a query to a generative AI site uses ten times more power than a simple Google search. The company is working to expand its portfolio of power generation assets to meet the rising demand. Currently, NRG has assets in Maryland, Illinois, Texas, and California, and generates power from oil, coal, natural gas, and renewable sources. Customers purchase power through a variety of service plans, tailored to their particular needs and likely future growth.

NRG makes strong use of the most plentiful fuels in North America’s power sector, coal and natural gas. Coal is highly abundant and easy to store, important attributes that support reliability in the power supply chain, while natural gas, which makes up the largest share of NRG’s portfolio, is not only abundant and low-cost but also cleaner burning. By basing its power portfolio on these two fuels, NRG ensures that it can provide low-carbon energy with a stable reserve. The company uses emission control and carbon capture technologies to reduce pollutants from its coal operations.

In an interesting move, NRG announced in August that its stock will have a dual listing on the NYSE Texas. This is a new, Dallas-based stock exchange, opened up as a fully electronic platform for equities trading. Texas is one of the fastest-growing state economies in the US, and is also home to more NYSE-listed companies than any other single state; the aggregate market value of Texas-based companies on Wall Street is approximately $3.7 trillion.

Looking at the financials, NRG generated $6.74 billion in revenues during 2Q25. That figure was up a modest 1.2% year-over-year, and it beat the forecast by $290 million. The company’s earnings figure came to $1.73 per share by non-GAAP measures, which was 3 cents more than had been anticipated.

We’ll check in once more with Scotiabank’s Weisel, who, despite the year-to-date gains, still sees plenty of value in this power provider. In his recent comments on the stock, he writes, “NRG is our top pick for value. While we won’t attempt to argue that NRG has the highest-quality assets or business mix, we’re drawn to the cheap valuation, impressive track record of execution (though the strategy has been more than a little inconsistent), and tremendous optionality embedded in the portfolio.”

This stance backs up Weisel’s Outperform (i.e., Buy) rating here, while his $212 price target points toward a 30% upside on the one-year time horizon.

NRG shares have a Moderate Buy consensus rating from the Street’s analysts, based on 8 recommendations that include 5 to Buy and 3 to Hold. The stock has a trading price of $162.96 and its average target price of $200.14 suggests that the shares will gain 23% by this time next year. (See NRG stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.