In this piece, I evaluated two toymaker stocks, Hasbro (NASDAQ:HAS) and Mattel (NASDAQ:MAT), using TipRanks’ Comparison Tool below to see which stock is better. A closer look suggests neutral views for both, albeit for entirely different reasons that make one the clear winner of this pairing.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Both companies design, manufacture, and sell toys, although they’re better known by their various brand names. For example, Hasbro is known for brands like Littlest Pet Shop, Magic: The Gathering, My Little Pony, Nerf, Play-Doh, and Transformers. On the other hand, some of Mattel’s top brands include Barbie, Fisher-Price, American Girl Brands, and various construction and arts & crafts brand names.

Shares of Hasbro have surged 23% year-to-date, although they’re up only 8% over the last year. Meanwhile, Mattel stock is off by 1% year-to-date, although it has gained 3% over the last 12 months.

With such a dramatic difference in their share price performances, it’s surprising that both companies are facing uphill battles right now. In fact, Hasbro has become unprofitable, notching a net loss of $1.5 billion in 2023, while Mattel is hanging on by a thread with net income of $292.5 million last year, even after the huge success of the Barbie film.

Both companies issued their first-quarter earnings results in late April, so a closer look at those numbers can help us determine which stock is better as both companies execute their turnaround efforts.

Hasbro (NASDAQ:HAS)

Although Hasbro doesn’t have a price-to-earnings (P/E) ratio currently because of its losses on a trailing-12-months basis, its price-to-sales (P/S) multiple of 1.8x is roughly in line with its mean P/S ratio (looking back to July 2019) of 2.0x. Thus, a neutral view seems appropriate after the recent run-up in the share price.

For the first quarter, Hasbro reported adjusted earnings of 61 cents per share on $757.4 million in sales, smashing the consensus estimates of 27 cents per share on $739.8 million in revenue. Attributing most of its sales decline to the sale of its eOne film and TV business, the toymaker swung to a net profit of $58.2 million from a $22.1 million net loss in the year-ago quarter.

Investors were thrilled with the less-than-expected drop in first-quarter sales. In fact, the big picture for Hasbro revealed other major improvements overall. For example, the toymaker expanded its operating margin from 1.8% a year ago to 15.3% in the most recent quarter through its ongoing cost-cutting efforts and inventory reductions. In fact, Hasbro’s owned inventory plummeted 53% year-over-year — an excellent sign that management is in the process of righting the ship.

Meanwhile, management highlighted the 65% spike in Entertainment revenue (excluding the hit from the eOne sale) and the 7% sales growth in its Wizards of the Coast and Digital Gaming division. Unfortunately, sales in Hasbro’s Consumer Products division, which accounted for over half of its sales in Fiscal 2023, plunged 21% year-over-year.

Hasbro maintained the guidance it provided in February for Fiscal 2024. The toymaker continues to expect Consumer Products revenue to fall by 7% to 12%, far less than the first-quarter plunge, and its Wizards of the Coast division to see a sales decline of 3% to 5%. Notably, it did not provide guidance for the Entertainment division.

Deservedly, Hasbro received several price-target increases following this earnings release, but the recent run-up in its shares appears to have right-sized its valuation.

What Is the Price Target for HAS Stock?

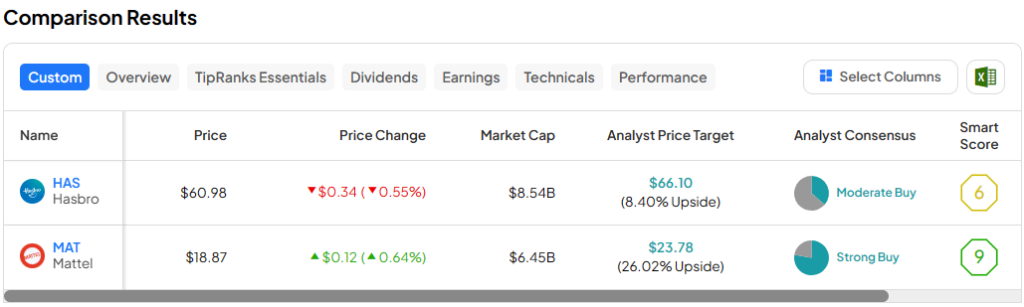

Hasbro has a Moderate Buy consensus rating based on four Buys, six Holds, and zero Sell ratings assigned over the last three months. At $67.78, the average Hasbro stock price target implies upside potential of 11%.

Mattel (NASDAQ:MAT)

Mattel shares have been range-bound between roughly $16 and $20 (with a brief spike to $22 in 2023) since late September 2022 despite fluctuations in its earnings results and valuation, suggesting there could be limited upside in the near term. Activist involvement could provide an upside catalyst strong enough to break through that resistance level, but a wait-and-see approach seems best for now, calling for a neutral view.

For the first quarter, Mattel posted an adjusted loss of five cents per share on $809.5 million in sales versus the consensus numbers of 13 cents per share in losses on $833.5 million in revenue. Net losses amounted to $28 million or eight cents per share, both improved from the year-ago loss of $78 million or 30 cents per share.

Cost-cutting measures enabled the toymaker to beat estimates on the bottom line, but the miss on sales is significant when compared to Hasbro’s significant beat. However, Mattel is apparently planning a lot of new hires and an expansion that will reverse much of that cost-cutting, so it seems like there could be a long road ahead.

Like Hasbro, Mattel faces many of the same issues, including an inventory glut and the broad-based cutbacks in toy purchases. However, a deeper dive reveals that Mattel didn’t have any division with a sharp increase in sales like Hasbro did. Mattel’s best-performing division was Vehicles, where worldwide gross billings rose 5% year-over-year (not adjusting for currency fluctuations).

In fact, the toymaker has drawn the interest of activist investor Barington Capital, which is calling for the sale of the American Girl and Fisher-Price brands. The firm is also targeting Mattel’s compensation and governance structure and calling for $2 billion in share repurchases.

While an activist could drive significant value at a struggling company like Mattel, any positive changes could take a while to come to fruition, especially with the other problems.

What Is the Price Target for MAT Stock?

Mattel has a Moderate Buy consensus rating based on six Buys, five Holds, and zero Sell ratings assigned over the last three months. At $23.10, the average Mattel stock price target implies upside potential of 22.4%.

Conclusion: Neutral on HAS and MAT

Although both toymakers receive neutral ratings, Hasbro is the clear winner here because its transformation looks much closer to completion, and it at least has one division with skyrocketing sales, even though the others are struggling. Additionally, its stock price displays signs of life, albeit with some volatility in recent years.

On the other hand, Mattel shares have been range-bound for years with no consideration of valuation or any other potential factors, and its sales miss and weakness across all its divisions are concerns as well. Although Barington’s involvement could eventually drive significant upside in the shares, it seems likely that it will take longer to see meaningful upside from Mattel than from Hasbro.