BRP Inc. (TSE: DOO)(NASDAQ: DOOO), which sells power sports vehicles such as boats and ATVs, has recently seen solid momentum regarding its stock price performance and fundamental performance. Since about mid-October, the stock has increased by nearly 30%, and it’s only down 5% year-to-date. The company also released strong Fiscal Q3-2023 results just last week, beating analyst expectations by a wide margin. Due to its strong fundamentals (aside from its high debt), the stock is worth considering, and analysts are unanimously bullish on the stock, giving it a “Strong Buy” rating.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

BRP’s Q3-2023 Results Were Impressive

When looking at BRP’s recent numbers, it becomes easier to understand why analysts love the stock so much. BRP produced record quarterly revenue yet again, coming in at nearly C$2.71 billion, up 71% on a year-over-year basis. This beat the consensus estimate of about C$2.346 billion. The company’s normalized earnings per share came in at C$3.64, beating the C$2.35 estimate, showing 146% year-over-year growth.

In addition, its normalized EBITDA was C$488 million (94% growth).

BRP also increased its guidance again. For the full year, BRP is projecting revenue to increase by 27% to 32% year-over-year, compared to the previous forecast, which was 100 basis points lower.

Also, normalized diluted EPS is forecast to be C$11.65 to C$12.00, C$0.35 higher than before, representing a 17% to 21% growth rate.

Is BRP’s High Debt Level Dangerous?

While BRP has been performing well over the past few years, it also loaded up on debt. As of the most recent quarter, it had about C$2.7 billion in debt compared to just C$59.9 million in cash and equivalents, or C$145.4 million when including short-term investments. This may spook investors, especially in a rising-interest-rate environment. However, it’s not necessarily dangerous.

When looking at BRP’s interest coverage ratio, which is calculated as operating income divided by interest expense over a specified period (we used the last 12 months), it comes out to 14.3x. This means that in the past year, BRP’s operating income has been able to cover interest payments more than 14x over. This is a pretty safe number, and since BRP is consistently profitable, the company should be fine, going forward.

However, it’s a cyclical retail company, so things can unexpectedly go south if the economy gets significantly worse. So, while the odds of financial trouble are low for now, it’s something to keep in mind.

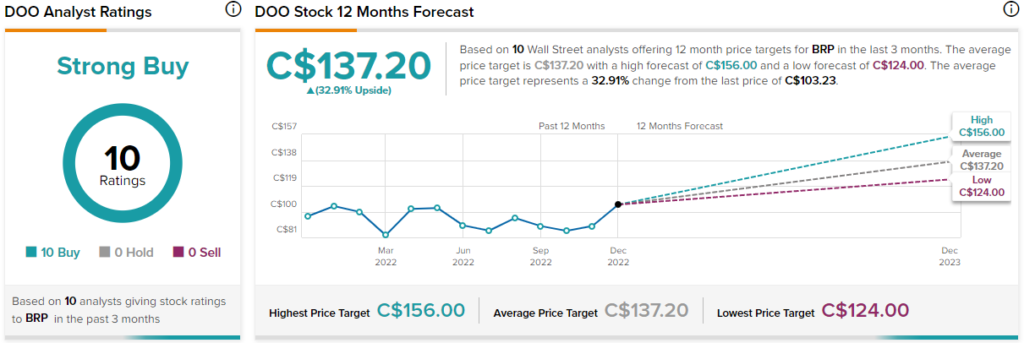

What is the Price Target for BRP Inc. Stock?

According to analysts, BRP Inc. stock earns a Strong Buy consensus rating based on 10 unanimous Buy ratings assigned in the past three months. The average BRP Inc. (DOO) stock forecast of C$137.20 implies 32.9% upside potential.

Conclusion: BRP Looks Cheap, but Consider Its Debt First

Analysts love BRP because of its strong performance. Based on its Fiscal 2023 guidance, the company is trading at a forward P/E ratio of about 8x, making it attractive. While this is surely indicative of a relatively cheap stock, investors need to consider if they are comfortable with the company’s high debt before making a purchase.