In this piece, I evaluated two Chinese e-commerce stocks, Alibaba (BABA) and PDD Holdings (PDD), using TipRanks’ Comparison Tool to see which is better. A closer look suggests bullish views of both, although a clear winner emerges from this analysis.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

While both Alibaba and PDD serve China, Alibaba focuses more generally on China and global marketplaces through its own platform and other brands like Tmall and Taobao, while PDD is known for its Pinduoduo discount e-commerce platform and its international counterpart, Temu. Alibaba also operates a cloud-computing platform and owns other technology companies.

Alibaba stock is up 5% year-to-date but off 18% over the last year, while PDD shares are down 12% year-to-date and up 43% over the last 12 months.

With such opposite share-price performances, it may be surprising that their valuations aren’t far apart. We’ll compare their price-to-earnings (P/E) ratios to gauge their valuations against each other and that of their industry.

Most of the Chinese online retail and e-commerce market is unprofitable, so Alibaba and PDD are in a class of their own and can’t be compared to an industry P/E. However, they can be compared to the industry on a price-to-sales basis (P/S). The Chinese e-commerce industry is trading at a P/S ratio of 1.2x versus the three-year average of 1.4x.

Alibaba (NYSE:BABA)

At a P/E of 18.4x and a P/S of 1.3x, Alibaba looks attractively valued, especially considering the sizable projected earnings growth that’s reflected in the much-lower forward P/E of 8.8x. Thus, a bullish view seems appropriate.

While forward multiples are based on unguaranteed future results, with a company like Alibaba, they do hold some credence. Alibaba has been widely considered the Amazon (AMZN) of China, and in many ways, it certainly is. Both stocks were once considered growth stocks, but this view is changing as these companies mature.

Both Alibaba and Amazon have successful, fast-growing cloud businesses. In Alibaba’s case, Cloud revenue is expected to grow in the double digits following the company’s strategic adjustments. In February, the company said it was in the process of revitalizing Tmall and Taobao and is focused on competitive pricing while investing in technology upgrades.

In the fiscal year that ended in March 2024, Alibaba’s overall revenue grew 8% year-over-year (in renminbi), which definitely removes the growth-stock status the company once held. However, if Alibaba’s cloud platform does ignite the massive growth that’s expected, we could see a resurgence of the massive revenue growth required for a company to be considered a growth stock.

Even if Alibaba’s overall growth rate remains steady, the stock just looks too cheap to ignore at current levels. It’s trading near the middle-to-low end of its historical five-year P/E range, which has varied from 10x to 30x since August 2019. The company may be being penalized for the 96% year-over-year drop in net income in the March quarter, but most of that drop was due to a decline in its publicly-traded investments.

However, it should be noted that there is significant risk in Alibaba stock because this thesis is based on expectations rather than concrete, current numbers. On the other hand, Amazon trades at a P/E of 52.5x and a P/S of 3.3x, and China offers much greater sales growth than the U.S. due to the size of the Chinese population alone.

What Is the Price Target for BABA Stock?

Alibaba has a Strong Buy consensus rating based on 13 Buys, three Holds, and zero Sell ratings assigned over the last three months. At $104.06, the average Alibaba stock price target implies upside potential of 33.5%.

PDD Holdings (NASDAQ:PDD)

At a P/E of 17x, PDD is trading in line with Alibaba’s valuation, although the P/S of 4.4x suggests it could be overvalued. However, PDD is priced like a growth stock on a sales basis. In 2023, the company put up an enormous revenue growth rate of 90% (in renminbi), albeit on a far smaller base than Alibaba. Overall, a bullish view seems appropriate.

PDD is currently trading at the low end of its P/E range, which has varied from 17x to 51x since March 2022, when it became profitable. The higher forward P/E of 10.5x is attractive but a bit more concerning, especially given the regulatory risks associated with PDD around its North America-focused Temu marketplace and its TikTok account (which boasts 1.8 million followers).

The U.S. recently started cracking down on TikTok and scrutinizing Chinese technology firms, questioning whether Temu is complying with laws meant to prevent companies from importing products made using forced labor. Unfortunately, PDD doesn’t break out separate earnings results for Temu, and less transparency is always a cause for investor concern.

A transcript of the latest earnings call reveals that PDD didn’t mention Temu specifically but did report that its “global business is still in a[n] exploration stage” with “plenty of room for improvement.” PDD also said it will invest in establishing an “industry-leading compliance program,” although what that entails is not clear yet.

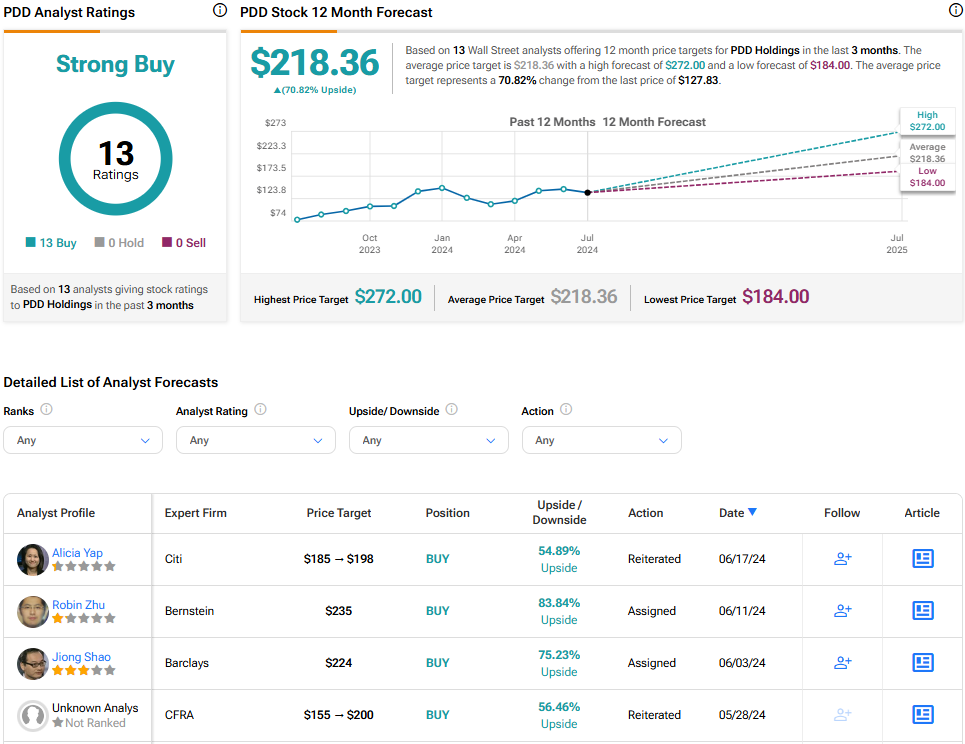

What Is the Price Target for PDD Stock?

PDD Holdings has a Strong Buy consensus rating based on 13 Buys, zero Holds, and zero Sell ratings assigned over the last three months. At $218.36, the average PDD stock price target implies upside potential of 70.8%.

Conclusion: Bullish on Alibaba and PDD Holdings

While both Alibaba and PDD look attractive over the long term, Alibaba looks like the better buy. Concerns about consumer spending in China have weighed on both stocks, but those look only temporary, suggesting now could be a good time to buy the dip in these stocks.

Importantly, the two companies share the risk of investing in Chinese stocks listed on U.S. exchanges, which could face delisting. Still, PDD looks riskier due to the threat of the U.S. passing a bill to force a separation from TikTok — or ban it from the U.S. entirely. Thus, as the more stable, stalwart Chinese e-commerce play, Alibaba looks like the better option.