Amazon’s (NASDAQ:AMZN) first quarter results could come in strong, but investors should brace for a tariff-driven bumpy ride ahead.

Claim 30% Off TipRanks

Forget margin or options. Here's how the pros trade AMZNThese are the dual conclusions reached by Truist analyst Youssef Squali, who points out that based on the Truist card data, it looks like Q1 is “tracking to the high-end of consensus expectations.”

To account for a smaller-than-expected foreign exchange (FX) impact, the analyst has adjusted 1Q25 estimates. Squali now sees total revenues of $156.2 billion (up from $155.4 billion), higher than the consensus estimate of $155.1 billion and exceeding the upper end of Amazon’s guide for $151.0 – $155.5 billion (+5-9% year-over-year). For North America, Squali is calling for revenues of $93.3 billion, slightly above the Street at $92.6 billion. Squali has also raised his International revenue estimate to $33.4 billion (+4.5%), up from $32.6 billion (+2%), and above consensus at $33.3 billion. Recall, management had guided to FX headwinds of $2.1 billion for 1Q25 when the company reported 4Q24 results in February. But the weakness of the US dollar relative to the Euro, JPY, and GBP in 1Q25 has led to a smaller FX impact than initially expected. Squali reckons FX reduced revenue by about 90 basis points (or $1.26 billion) in the quarter, compared to the previously expected 150 basis points ($2.1 billion). For operating income, Squali anticipates $17.5 billion (11.2% margin), the same as consensus and towards the high end of the guided range of $14-18 billion.

Moving forward, however, Squali is concerned about the effects of tariffs, especially with China, which is now on a 125% rate. “While there are several currents and countercurrents hurting and benefiting Amazon at the same time, we believe the net net of this is an increase in prices virtually across the board and a likely slowdown in consumer spending, which will weigh on the company’s growth for the rest of FY25 and FY26 and on margins,” the analyst explained.

As such, he has revised his NA revenue growth forecast for the last three quarters of FY25 from the previous 9% to 7% and for FY26 from 9% to 6%. As a result, overall revenue growth in FY25 is now expected at +8.3%, down from +9.3%, equating to $690.8 billion vs. $697 billion beforehand. For FY26, Squali has lowered his growth estimate from 9.3% to 8.1% with revenue expected to reach $747 billion, down from the prior forecast of $762 billion.

Despite the lowered expectations, Squali keeps an overall favorable stance here. “We still see Amazon as a share gainer and a LT winner across eCommerce, Advertising, Cloud and Logistics, and remain constructive on the stock at current levels,” he summed up.

Bottom line, Squali kept a Buy rating on the shares but lowered his price target from $265 to $230, now suggesting the stock will gain 28.5% in the months ahead. (To watch Squali’s track record, click here)

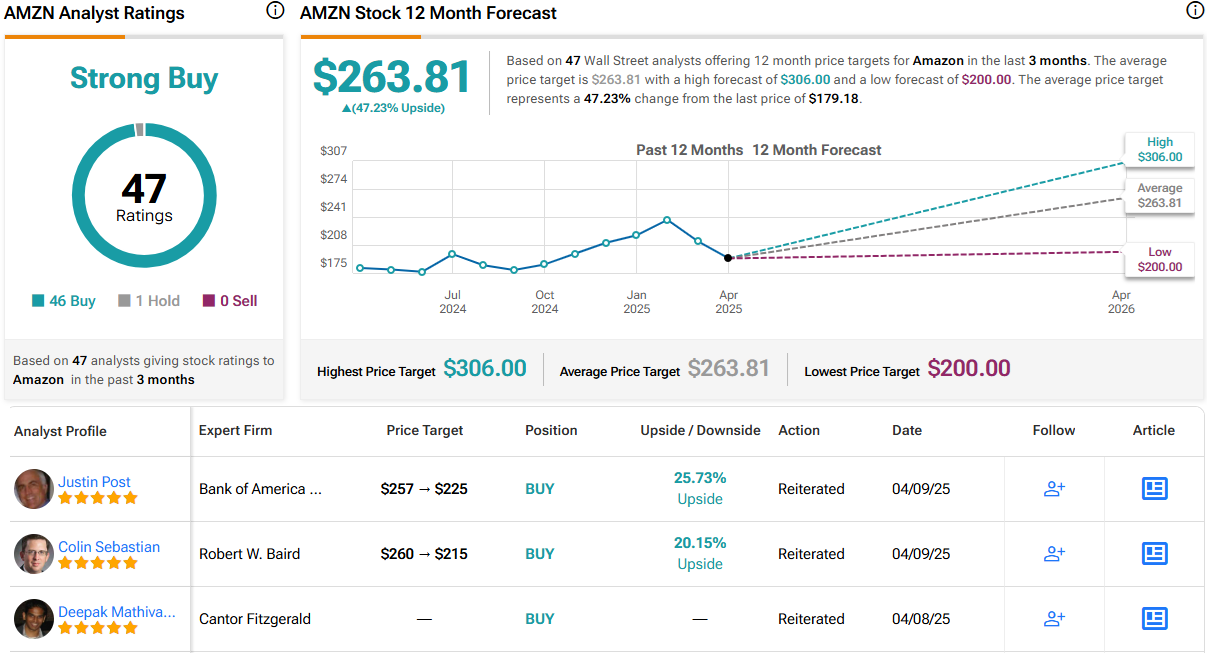

Like Squali, most others on the Street are backing AMZN’s chances. Only one analyst stays on the fence, and with an additional 45 Buys, the stock naturally claims a Strong Buy consensus rating. The forecast calls for 12-month returns of 47%, considering the average target clocks in at $263.81. (See Amazon stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.