We’re approaching a peak in Phase 1 of the AI infrastructure capex cycle—a period defined by urgency, a scarcity mindset, front-loaded spending, and intentionally redundant buildouts. Overbuilding has been the rational strategy, because being short on compute is strategically unacceptable. Advanced Micro Devices (AMD) has benefited meaningfully as a result.

Meet Samuel – Your Personal Investing Prophet

NVDS: built for a short position on NVDAAs the only credible second supplier at scale versus Nvidia (NVDA), AMD’s valuation risk has risen nearly as quickly as its data center revenue share. For that reason, I’m neutral on the stock as cyclical risk starts to reappear—even as I continue holding it tactically over the next six to nine months.

AMD’s Data Center Scale Will Come in Waves

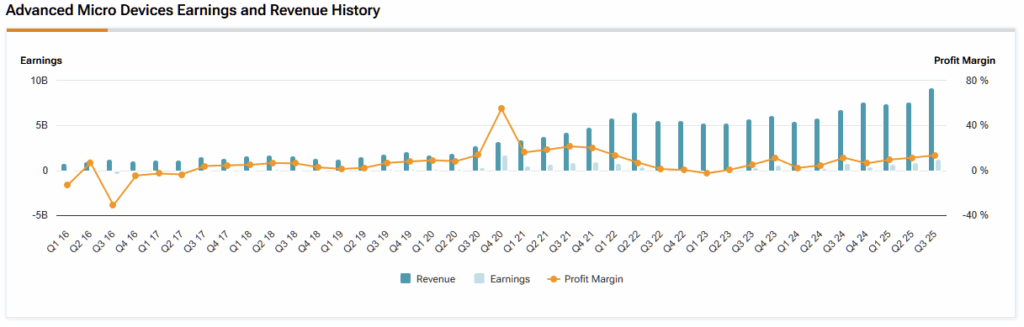

In its most recent quarter, AMD reported total net revenue of $9.246B, including $4.341B from its Data Center segment. The broader AI compute market is expanding so rapidly—and buyers want diversification so badly—that AMD can continue compounding by supplying a wider set of customers and workloads, even if Nvidia remains the clear No. 1 choice.

In many ways, AMD functions as compute-market insurance for Big Tech. When a single supplier becomes a bottleneck, having a second provider with credible performance at scale becomes a meaningful operational advantage.

That said, the current capex wave we’ve seen in Phase 1 has been sharply front-loaded. Put simply: scarcity drives urgency, urgency pulls forward orders, and eventually the system transitions from “secure capacity” to “utilize capacity.”

Importantly, Phase 1 capex cycles typically resolve through utilization and digestion rather than outright collapse. Spending continues, but the marginal return on each new unit of infrastructure inevitably declines once enough capacity exists. And for the market to correct meaningfully, demand growth doesn’t need to stop—it merely needs to stop accelerating.

What Phase 2 of AI Will Look Like

Even if AI semiconductor growth remains positive in Phase 2, markets will stop rewarding cyclicality with the same long-duration valuation multiples. The more likely outcome is valuation compression first, followed by a slower, more incremental upside profile.

AMD’s current valuation still implies infrastructure urgency will persist at or near peak intensity. That’s a demanding assumption.

Its forward P/E is roughly 120% above the sector median, though its forward PEG, about 26.5% below the sector median, helps explain investor optimism. Still, at such a high absolute valuation, even modest downward revisions to long-term growth expectations could compress the multiple quickly—and keep it under pressure for a prolonged period. This dynamic is not unique to AMD; it’s a risk across the AI equity complex.

Does that mean AI is automatically a bubble? Without getting stuck in semantics, today’s elevated multiples appear more durable than those of the dot-com era because the demand horizon is longer and more structurally tied to refresh cycles for AI GPUs. If a correction occurs, it’s more likely to resemble 2022 in magnitude rather than 2000 or 2008.

In Phase 2, growth should become steadier and spread across a broader ecosystem of vendors, with greater emphasis on inference-related technologies from companies like Marvell (MRVL) and Broadcom (AVGO). That’s why being heavily long AMD without a clear exit strategy at this stage of the cycle is increasingly unwise—regardless of what momentum, quant, or consensus indicators suggest.

Staying neutral on AMD in an overvalued, late-cycle macro environment isn’t exciting—it can feel boring—but those who remain calm at the top of the wave often get paid most when the cycle troughs.

Is AMD a Buy, Hold, or Sell?

On Wall Street, AMD holds a consensus Strong Buy rating, based on 26 Buys, eight Holds, and zero Sells from top analysts. The average price target of $283.48 implies 23% upside over the next 12 months.

That looks bullish on the surface, but it’s worth remembering that consensus tends to be most uniformly positive shortly before downside emerges. This is why macro valuation context matters—especially in a market where the S&P 500 (SPX) sits roughly 2.4 standard deviations above its modern-era trendline. Anchoring to broader valuations helps maintain objectivity beyond bullish consensus narratives.

The ‘Never-Ending’ Wave Fallacy Is Real

AMD has been a standout performer in Phase 1 of the AI infrastructure cycle, with urgency-driven capex and diversification demand solidifying its position as the only credible alternative supplier at scale to Nvidia.

AI is a durable opportunity—but much of the recent gain has become overpriced. Capex will inevitably shift from securing capacity to utilizing it, meaning growth may persist even as incremental returns and valuation support fade. Unfortunately, strong fundamentals do not guarantee strong stock performance from here, especially when valuations are extreme.

AMD can still expand its data center presence through broader customer penetration and greater exposure to inference, but the market is unlikely to reward that progress with the same valuation expansion investors have enjoyed so far.

Sometimes discipline means staying neutral—refusing to get swept up in excess precisely when it becomes most tempting. Holding AMD tactically for the next six to nine months can make sense, but committing long-term capital without a defined exit strategy risks confusing durable demand with permanent urgency.