Tech conglomerate Alphabet’s (NASDAQ:GOOGL) Google announced a planned shrink in the team size of its mapping services unit, Waze. This fits neatly with Google’s ongoing efforts to integrate Waze with its own mapping products.

Meet Samuel – Your Personal Investing Prophet

- Start a conversation with TipRanks’ trusted, data-backed investment intelligence

- Ask Samuel about stocks, your portfolio, or the market and get instant, personalized insights in seconds

With 140 million active users, Waze enables commuters to judge the fastest driving route from one location to another, utilizing the most recent traffic information.

Waze Unit Transformation

In a move to merge the Waze mapping services unit with its own map products, search engine Google revealed that it will cut jobs at the Waze unit. The number of jobs that will be trimmed remains undisclosed.

The news was disclosed by CNBC, citing an email to employees from Chris Phillips, head of Google’s map division. Israel-based Waze is a social-mapping-location-data company that gave Google a social data boost after its acquisition in 2013 for around $1.3 billion.

Indicating that Waze’s ad monetization will soon be managed by the Global Business Organization, which is similar to Google Maps, Phillips added, “Unfortunately, this will result in a reduction of Waze Ads monetization-focused roles in sales, marketing, operations, and analytics.”

Advertisers and partners will be notified of the change on Wednesday, June 28, while the plan’s next steps will be discussed with the Wazers (term for employees at Waze) at its next Waze Town Hall on July 11.

Google’s Motive Behind Waze Consolidation

Google plans to transform Waze’s strategy, with ads displayed on Waze using the Google ads platform instead of a separate ad system.

Since December 2022, the company has been integrating Waze’s into its own Geo unit (that includes Google Maps, Google Earth, and Street View).

In its efforts to enhance efficiency, Google has undertaken many steps. Cutting down 6% of its workforce in January, eliminating some projects, and downsizing a few are some of the ones adopted. In its most recent quarter, the company reported a 1.9% growth in Google search and other advertising revenue while YouTube ads and Google Network ads revenue were down 2.6% and 8.3% respectively.

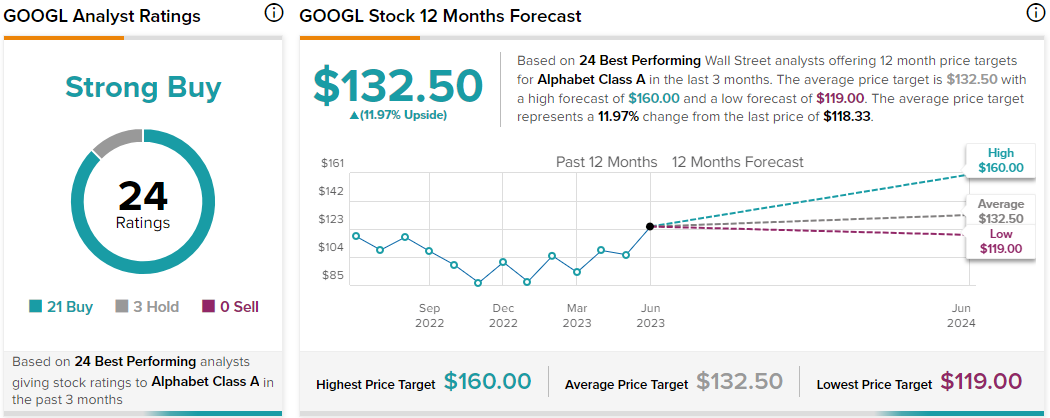

Is Google a Good Buy for the Long Term?

Of the 24 Top Wall Street Analysts covering the GOOGL stock, 21 have a Buy rating while three assign a Hold, taking the average analyst consensus rating to Strong Buy. The average analyst price target stands at $132.5, implying a 12% upside potential from current levels.

In the past two days, the stock has received two downgrades to a Hold rating from a Buy rating at Bernstein and UBS.

Looking at the GOOGL stock price, it has generated 69% returns in the past three years with YTD gains standing at 33%. The company’s fundamentals highlight a market leader position in the Search segment and a growing momentum in its Cloud business. These growth factors could present investors with a long-term buying opportunity.