As an investor, I’m looking to buy ownership in businesses with durable business models. In my view, the best way to discern whether an established company has a lasting business model is by looking at its dividend payment track record. A corporate history of consistent dividend growth is as true of a test of quality as any other. That’s because cash payments to shareholders can only grow over time if a company’s investments in projects are paying off. Having hiked its dividends per share for 41 consecutive years, Air Products & Chemicals (APD) is as proven as they come, easily earning the distinction of being a Dividend Aristocrat.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

A look at Air Products & Chemicals’ most recent earnings results and project backlog leads me to be optimistic about its fundamentals. However, the stock has rallied almost 23% so far in 2024. That has pushed the valuation multiple beyond what I believe is its fair value. That’s why I’m beginning coverage with a Hold rating.

Air Products & Chemicals Posts Double Beat in Fiscal Year 2024

I would argue that Air Products & Chemicals’ fourth-quarter results, shared on November 7th, support my Hold thesis. The company’s sales decreased by 0.1% year-over-year to $3.19 billion during the quarter, just shy of the analyst consensus of $3.21 billion for the period. The decline in sales was attributed to lower natural gas prices in North America, as explained by CFO Melissa Schaeffer in her opening remarks during the Q4 2024 earnings call.

Nevertheless, despite the dip in sales, Air Products & Chemicals delivered a strong performance on the earnings front. The company’s adjusted EPS surged 13% year-over-year to $3.56 in the fourth quarter, exceeding the analyst consensus by $0.08. This growth was driven by reduced pass-through costs and higher volume, which led to an impressive 450-basis-point expansion in the adjusted EBITDA margin to 44.1%. As a result, Air Products & Chemicals was able to achieve double-digit EPS growth, even with relatively flat sales during the quarter.

Air Products & Chemicals Poised for Growth from Key Projects

Air Products & Chemicals’ industry outlook is another reason I like the company from an operational standpoint and rate it a Hold. On a macro level, the forecast for the global clean hydrogen market is impressive: Air Products & Chemicals anticipates that the industry will surpass $600 billion in annual revenue by 2030 and exceed $1 trillion by 2050. To give an idea of the true scale of this growth opportunity, the company’s currently approved hydrogen projects make up less than 1% of future market expectations, according to Chairman and CEO Seifi Ghasemi.

The size of this market gives Air Products & Chemicals the ability to be selective with the projects to which it allocates shareholder capital. New assets in Uzbekistan should continue to drive growth in the near term. Looking ahead a few years, the company stands to benefit from its $5 billion NEOM green hydrogen mega project in Saudi Arabia, expected to be placed into service by the end of 2026.

That’s why, beyond the 3.7% rise in adjusted EPS to $12.89 expected for Fiscal year 2025, double-digit growth is anticipated in the future. In Fiscal year 2026, another 10.1% jump in adjusted EPS to $14.19 is projected. For Fiscal year 2027, an additional 11.9% climb in adjusted EPS to $15.87 is the current analyst consensus. Overall, Ghasemi is confident that Air Products & Chemicals can generate at least 10% annual adjusted EPS growth for the next 10 years.

APD Delivers Strong Dividend and Maintains Robust Balance Sheet

Air Products & Chemicals’ market-beating dividend and phenomenal balance sheet are two more reasons that back up my Hold rating. The APD stock’s 2.13% dividend yield comes in about 60 basis points above the basic materials sector average of 1.53%. Air Products & Chemicals’ starting income is also sustainable, evidenced by a payout ratio that’s expected to be in the high 50% range for FY 2025. I believe this should allow the company to deliver at least high-single-digit annual dividend hikes to shareholders over the next five to 10 years. For my money, this would be a nice mix of starting income and income growth potential.

Financially, Air Products & Chemicals is doing well. The company’s interest coverage ratio in FY 2024 was 20.4, meaning it could endure a meaningful downturn in its profits and remain financially solvent. The company’s 44% debt-to-capital ratio further suggests that its balance sheet is well-capitalized. For these reasons, Air Products & Chemicals possesses an A credit rating from S&P Global (SPGI) on a stable outlook.

APD Stock Looks Fully Valued

The one factor that counters my overall positive sentiment toward Air Products & Chemicals’ stock is its valuation, which explains my Hold rating. The stock is priced at a current-year P/E ratio of 25.7, greater than its 10-year average P/E ratio of 23.6. Since Air Products & Chemicals’ growth profile remains consistent with past performance, it’s difficult to justify a multiple any higher than the 10-year average.

This effectively means that the market is already pricing in both FY 2025 and FY 2026 results. As a result, the near-term upside is limited, which could mean that the stock may eventually present better buying opportunities.

Is APD a Good Stock to Buy?

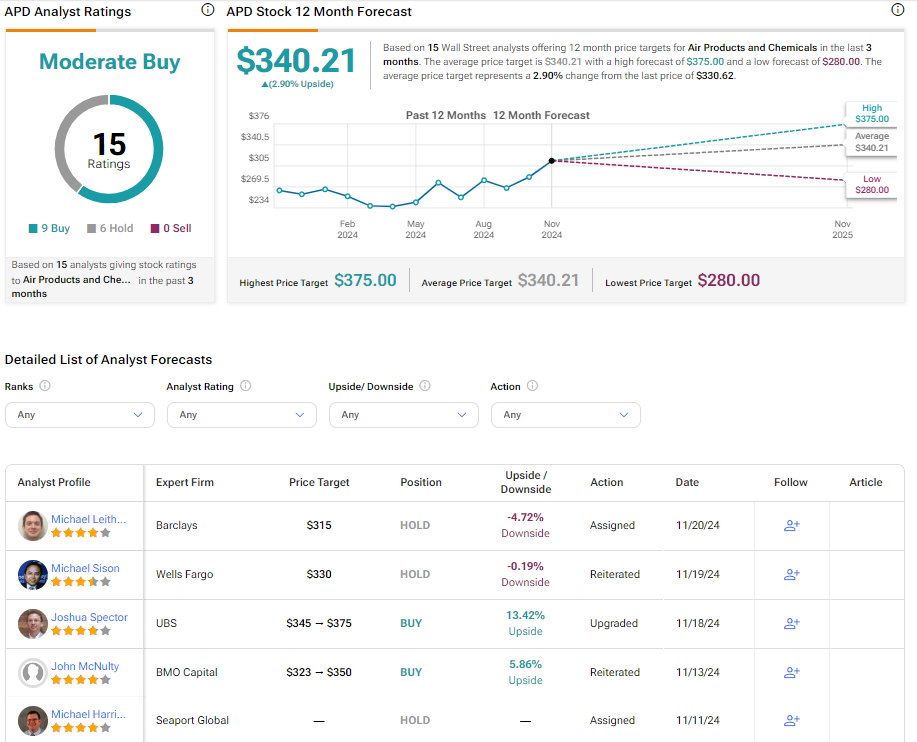

Shifting to Wall Street, analysts have a Moderate Buy rating for Air Products & Chemicals. Out of 15 analysts, nine have issued Buy ratings and six have assigned Hold ratings in the last three months. The average 12-month price target of $340.21 suggests a 2.9% upside from the current share price.

Key Takeaway

Air Products & Chemicals is a reliable name in the dividend stock investment universe. The company operates as a trusted leader in the global industrial gas industry, which appears poised for long-term growth. With an A-rated balance sheet, Air Products & Chemicals further solidifies its position as a steady pick. These factors make the stock one to watch for the next market pullback or correction. Therefore, I’m initiating coverage with a Hold rating.