Affirm Holdings (NASDAQ:AFRM) delivered better-than-expected Q3 Fiscal 2024 results. Despite the Q3 beat, AFRM stock closed 9.5% lower on Wednesday. Mizuho Securities analyst Dan Dolev recommends buying this weakness in AFRM stock. Dolev is bullish about AFRM, and his price target of $65 implies a 105.83% upside potential. Although Dolev is bullish, the majority of Wall Street analysts do not endorse buying AFRM stock and remain sidelined.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Let’s dig deeper.

Here’s Why Affirm Stock Declined

Affirm, which offers the Buy Now, Pay Later (BNPL) service, recorded the fourth consecutive quarter of increasing gross merchandise volume (GMV) growth. At the same time, credit performance was stable and generated a solid yield.

However, its key partner, Shopify (NYSE:SHOP)(TSE:SHOP), which accounts for a notable portion of its GMV, provided lackluster guidance, indicating a possible decline in e-commerce demand. Investors are apprehensive about the potential challenges this may pose for Affirm.

Moreover, Affirm’s Q4 guidance suggests a sequential slowdown in revenue and GMV growth rate, which is perceived as a negative.

AFRM – Q3 Performance

Affirm delivered total revenue of $576 million, up 51% year-over-year. Moreover, it surpassed analysts’ average estimate of $550 million. Revenue as a percentage of GMV grew to 9.2%, compared to 8.2% in the year-ago quarter.

In terms of key performance metrics, its GMV increased 6% year-over-year to $6.3 billion, with its growth rate accelerating for the fourth consecutive quarter. Active consumers increased 13% to 18.1 million as of March 31, 2024. At the same time, the active merchant count increased by 19% to 292,000.

Affirm reported a loss of $0.43 per share, much narrower than the loss of $0.69 per share in the prior-year quarter. Moreover, it compared favorably to the Street’s forecast of a loss of $0.70 per share.

Outlook

Affirm expects to report Q4 revenue between $585 million and $605 million, indicating 31% to 36% year-over-year growth. This surpasses analysts’ expectations of $578.7 million for the quarter.

Additionally, AFRM projects GMV to be between $6.75 billion and $6.95 billion, marking a 23% to 26% year-over-year increase. This projection also exceeds analysts’ estimates of $6.65 billion.

While its revenue and GMV forecast surpass analysts’ expectations, it shows a sequential deceleration in growth rate.

Dolev Sees Shopify Worries Overblown

In a note to investors, Dolev said that investors’ reaction was “overblown.” According to the analyst, Shopify constitutes only about 10% of AFRM’s GMV.

Thus, Dolev believes that the initial positive movement in the stock post-earnings aligns better with AFRM’s performance. He suggests buying AFRM based on its solid fundamentals rather than reacting impulsively to negative market sentiment.

Is Affirm a Good Stock to Buy?

Affirm stock is up about 157% in one year, which raises concerns over its valuation. AFRM sports a forward enterprise value to sales multiple of 6.94, much higher than the sector median of 3.04. High valuations and a fear of slowing growth in e-commerce spending keep analysts sidelined on AFRM stock.

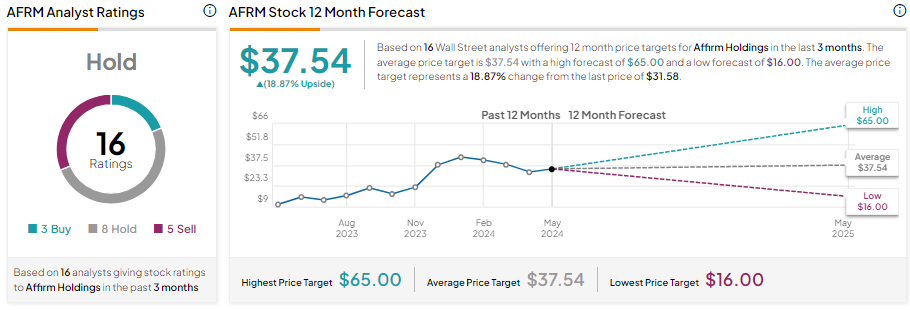

AFRM stock has a Hold consensus rating with three Buy, eight Hold, and five Sell recommendations. Analysts’ average price target on AFRM stock is 37.54, implying an 18.87% upside potential from current levels.