Adobe (NASDAQ:ADBE) stock is finally catching a break after clocking in some solid quarterly earnings results. With the company also recently clarifying in its updated terms of service that it will not use customer data to train its AI models, it looks like management has been quick to defuse what could have grown into a sticky situation. After all, in the AI age, protecting user privacy seems every bit as important as AI capabilities. Despite newfound momentum, though, I’m inclined to maintain a neutral stance on the stock, as some regulatory and competitive risks remain.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

With the U.S. Federal Trade Commission (FTC) reportedly targeting Adobe for charging customers hidden fees while making it hard for them to cancel, another layer of uncertainty stands to cloud the Adobe story as it transitions into the AI age.

The outcome of the FTC suit remains to be seen, but regardless, having such a regulatory overhang could not have come at a worse time. Though Adobe’s transition to the cloud under its long-time top boss, Shantanu Narayen, was a profound success, I’m not all too sure how the pivot to AI will play out over the coming few years.

Changes Could be Coming after FTC Suit

Undoubtedly, Adobe still has one of the widest economic moats in all of software. And while going all-in on Adobe Sensei and Firefly (Adobe’s AI innovations) could widen the moat further, questions linger as to how well the software giant will be able to keep its subscribers aboard should subscriptions become easier to cancel. Will new AI innovations be enough to prevent them from jumping ship? Further, with the FTC setting its sights on Adobe, I think there’s also a big chance that a big change could be coming for how Adobe does subscriptions.

Only time will tell if regulatory actions lead to Adobe’s suite becoming as easy to cancel as your run-of-the-mill video streaming service. Regardless, ease of cancellation and more flexibility for customers could entail greater churn rates. And if Adobe does not stay at the absolute front of the generative AI boom, competitors may finally have what it takes to disrupt the Adobe moat as we know it.

Of course, it’s far too soon in the game to know which firm can step up and act as a credible foe to Adobe. Putting more AI tools in the hands of creators may not be enough to give Adobe shareholders pause. At the end of the day, Adobe has a time-tested ecosystem and a massive user base that may not be so quick to leave Adobe’s walled garden, especially as Adobe injects more intelligence across its existing software.

Adobe’s Transparency and Caution on AI Could be Big Advantages

Indeed, using user data to train models would have given Adobe a massive advantage over its potential AI rivals. Even though Adobe confirmed it will not use customer data to train AI models, I think terms could be subject to change in the future. Perhaps Adobe could hit a middle ground that allows a subset of users to allow their data to be used for training purposes.

Indeed, not all users mind if their content is used by a company if it means doing their part to help a service become even better. With recent user worries surrounding how their data may have been used, it’s clear that transparency is number one when it comes to excelling in the AI age.

Perhaps nobody in the image generation and AI-fueled creativity software scene does it better than Adobe when it comes to transparency.

The company has been cautious when it comes to data sources used to train models like Firefly. And it’s this degree of caution that will allow Adobe to advance in the AI age without running into harsh setbacks its rivals may be subject to.

Last year, Stability AI, the firm behind image generator Stable Diffusion, was taken to court by Getty Images (NASDAQ:GETY) over images used “without permission.”

Undoubtedly, firms like Stable Diffusion may have run a bit ahead of their skis in the AI age. Either way, it’s clear Adobe wants to ensure it’s “flooring it” on AI while also steering clear of legal issues or potential harm that could arise from advanced models lacking appropriate guardrails. Regulators have taken aim at Adobe, and they could continue to be on its back. Therefore, Adobe must proceed with caution.

Can Adobe strike a balance between safety, transparency, and capability? Definitely. But can it do so better than up-and-coming rivals? As always, time will tell.

The Valuation Seems Expensive

After the stock surged on the back of an impressive quarterly earnings beat, the stock seems quite expensive at 47.2 times trailing price-to-earnings (P/E), especially versus the 41.1 times infrastructure software industry average. While I believe Adobe deserves a premium, given its AI powers, many of its disruptive rivals also stand to realize said powers.

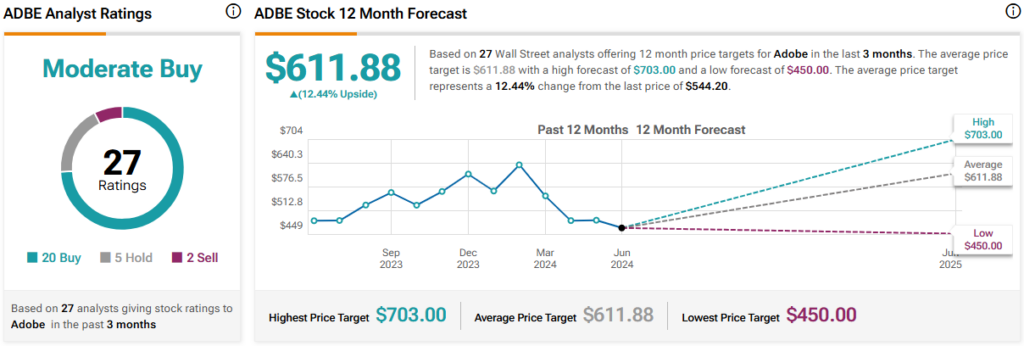

Is ADBE Stock a Buy, According to Analysts?

On TipRanks, ADBE stock comes in as a Moderate Buy. Out of 27 analyst ratings, there are 20 Buys, five Holds, and two Sell recommendations. The average ADBE stock price target is $611.88, implying upside potential of 12.4%. Analyst price targets range from a low of $450.00 per share to a high of $703.00 per share.

The Takeaway

The recent quarterly earnings beat has ADBE stock on the mend again. But with the FTC taking Adobe to court, the company will need to ensure it’s not skating offside to avoid further regulatory scrutiny in the future. Indeed, Adobe has fallen in the sights of regulators. If Adobe moves too fast on AI and breaks things, perhaps the creative software firm may face as much of a regulatory overhang as the Magnificent Seven.