Sometimes, all it takes is a little love from an analyst to turn a stock’s performance upward. That’s exactly what happened to Williams Sonoma (NYSE:WSM), well-known for its pricey home furnishing stores. It got an upgrade with one analyst and, with that, added modestly to its share price in Thursday afternoon’s trading.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

The word came from no less than Wedbush Securities, which upgraded Williams Sonoma from Neutral to Outperform. The reason was simple: there’s a good chance that Williams Sonoma can improve its margins and give investors a little more bang for their collective buck. Basically, Wedbush analysts look for a reversal in interest rates to hit in 2024. That, coupled with a reassertion of normal demand following the loss of the pandemic boost that pretty much any home supply store got in 2020 to sometime in about 2021 or so, should help improve things at the home retailer.

Things May Be Looking Up Already

If Williams Sonoma were having trouble, then the first place it would likely show up is in its store count. It would be cutting hours or closing stores altogether to help it save cash. That’s a mixed bag right now; Williams Sonoma is set to close at least one store in Wichita, Kansas. That’s a blow to Kansans, who believed that a Williams Sonoma on hand made their city really “feel like a city.” However, a planned closure in San Francisco has been pushed back a full year, confirming its lease until 2025. That makes it something of a wash right now, which could certainly be worse.

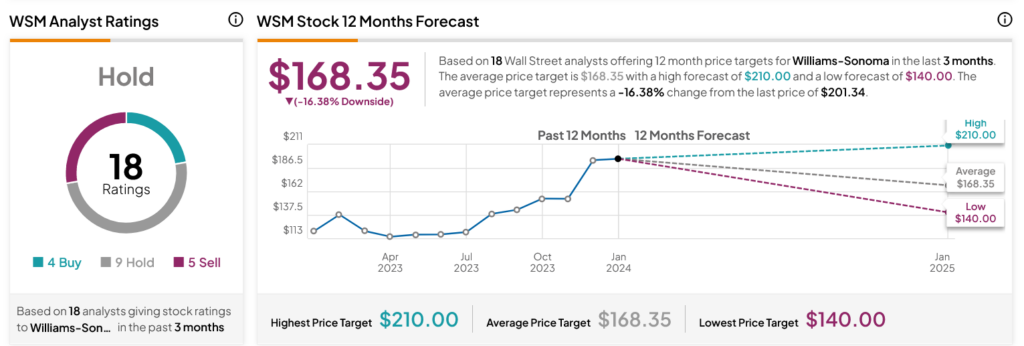

Is Williams Sonoma a Good Stock to Buy?

Turning to Wall Street, analysts have a Hold consensus rating on WSM stock based on four Buys, nine Holds, and five Sells assigned in the past three months, as indicated by the graphic below. After a 60.22% rally in its share price over the past year, the average WSM price target of $168.35 per share implies 16.38% downside risk.