“The customer is always right” is a credo that is often used and applies especially to consumer-facing businesses like Starbucks (SBUX). Throughout its history, the coffee franchise’s focus on the customer experience and product quality has paid off remarkably. After all, the Starbucks brand is estimated to be worth $60.7 billion, making it the 15th most valuable brand in the world. But even with all of this success, the company still has immense room for improvement.

Claim 30% Off TipRanks

Trade SPY with leverageIndeed, Starbucks’ sales have declined for three consecutive quarters. The good news is that newly appointed CEO Brian Niccol has plenty of ideas to return the storied brand to meaningful growth. Nevertheless, after rallying 39% from its 52-week low in July, Starbucks’ valuation looks a bit too steep to warrant a Buy rating. As a result, I have a Hold rating toward the stock right now.

Starbucks Had a Rough Q4

I am neutral on Starbucks because there is no denying that its FQ4 2024 results were ugly, as I alluded to at the outset. The company’s net revenue declined by 3.2% year-over-year to $9.1 billion during the quarter. This missed the analyst consensus by $300 million.

On a more positive note, net store openings in the last four quarters (+5.7%) pushed the total store count above 40,000. However, that was more than offset by operational weakness in North America and China, which pushed global comparable store sales 7% lower over the year-ago period.

In addition, Starbucks’ non-GAAP EPS dropped by 24.5% year-over-year to $0.80. This came up notably shy of the $1.02 analyst consensus during the quarter. Starbucks cited promotional activity and investments in store partner wages and benefits as the reasons for a 380-basis point contraction in its non-GAAP operating margin to 14.4%. That’s why the pace of the non-GAAP EPS drop exceeded the decrease in net revenue in the quarter.

Great Businesses Like Starbucks Usually Rebound

One of the harsh realities of business is that all exceptional companies must endure ebbs and flows along the way. The silver lining is that they often bounce back, and this looks like it will be the case for Starbucks. That’s because CEO Brian Niccol is already diligently working on implementing the plan to “Get Back to Starbucks.” This revolves around efforts to once again foster a welcoming and convenient coffeehouse environment. But this will take time, which is another reason why I am neutral on the stock.

Eliminating an extra charge for customizing beverages with non-dairy milk was the first step in this direction. That began with the launch of Starbucks’ holiday menu on November 7th. Almost half of current customers in the U.S. who pay to modify their beverage at company-operated stores will see a price reduction of over 10%. Additionally, Starbucks is planning on bringing condiment coffee bars back to cafes by early calendar year 2025 while also cutting down its overly complex menu. This should speed up order times and enhance the overall environment at stores.

The current Fiscal Year (2025) is likely going to be another down year for Starbucks, with non-GAAP EPS predicted to decrease another 5.7% to $3.12. However, as the management team continues to implement changes, a 20.2% rebound in non-GAAP EPS to $3.75 is expected in FY 2026, along with an additional 16.7% rise in FY 2027 to $4.38.

Starbucks Boasts a Market-Beating Dividend and Investment-Grade Balance Sheet

As I’m waiting for Starbucks’ turnaround to materialize, I take heart in the dividend. The stock’s 2.5% dividend yield clocks in at double the S&P 500’s (SPY) 1.2% yield. Starbucks’ most recent 7% quarterly dividend hike to $0.61 per share also demonstrates that the company is no slouch when it comes to dividend growth.

The payout ratio is expected to be a bit elevated in the high 70% range in FY 2025, so I foresee a temporary slowdown in dividend growth to mid-single-digits for the next couple of years. Beyond that, though, I believe high single-digit annual dividend growth will resume.

Another plus that supports the dividend is Starbucks’ balance sheet. The company’s interest coverage ratio was 12.3 in FY 2024. Given that this will probably be close to the earnings trough for Starbucks, that’s a healthy interest coverage ratio, in my view. Unsurprisingly, this bolsters the argument that S&P Global’s (SPGI) BBB+ credit rating for the company is justified.

Starbucks Trading at a Historically Premium Valuation

Despite my confidence that Starbucks will restore its growth, the market is pricing the stock as if this has already been done. The current year P/E ratio of 31.8 is above the 10-year average P/E ratio of 29.8. Starbucks does have room to grow in spite of its scale, but probably not quite at the rate to warrant a historically premium valuation. Even the forward P/E ratio of 26.5 suggests shares are already fully valued for at least the next year. This is the big element behind my Hold rating for Starbucks stock.

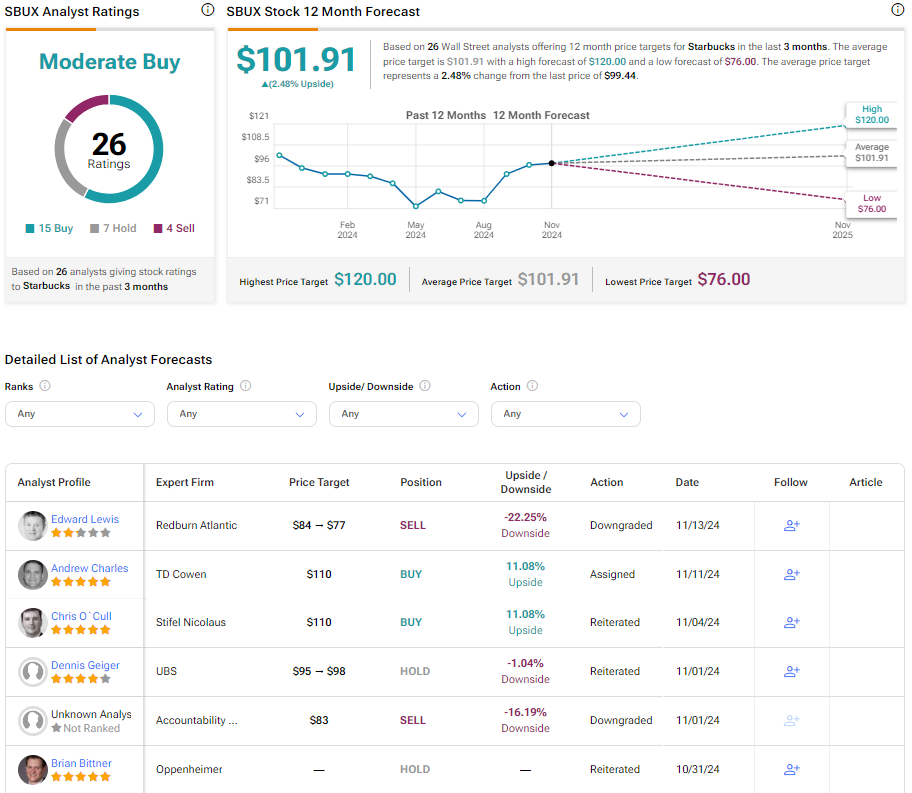

What Are Wall Street’s Thoughts?

Shifting to Wall Street, analysts have a Moderate Buy rating for Starbucks. Out of 26 analysts, 15 have issued Buy ratings, seven have assigned Hold ratings, and four have issued Sell ratings in the last three months. In addition, the average 12-month price target of $101.91 implies 2.48% potential upside from the current share price.

Conclusion

Time will tell whether the moves Starbucks is making will pay off and revive growth. A strong case can be made that Starbucks’ actions could indeed drive growth. Yet, the valuation seems to limit the upside in the next 12 months, which is why I’m going to be holding my stock and issuing a Hold rating.