In times of economic downturns, with much uncertainty surrounding the U.S. economy and Trump’s infamous import tariffs, a strong portfolio needs some defensive picks to weather the storm. Historically, PepsiCo (PEP) has been a reliable defensive dividend stock that many investors have turned to for diversification. I like to think of PepsiCo as a giant ocean liner—it moves slowly but reaches its destination unscathed, keeping the passengers happy through service and price.

Claim 30% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

However, at the moment, this massive ship is facing some headwinds that have slowed its progress. Specifically, PepsiCo is struggling with weakness in its snack segment, which has been hit by health-conscious consumers and users of weight-loss drugs stepping back from sugary drinks in favor of healthier alternatives. Additionally, in FY2024, PepsiCo could not fully cover its dividend distribution as free cash flow shrank compared to the previous year.

While I think there’s a good chance the management team can steer this ship through the current storm and eventually return to strong cash flow growth, I’m not sure how long that process will take. Until we get more clarity, PepsiCo may continue to underperform. Given this scenario, I don’t think now is the ideal time to buy PEP, and I’m adopting a neutral rating for now.

PepsiCo Battles Declining Snack Sales and Shifting Trends

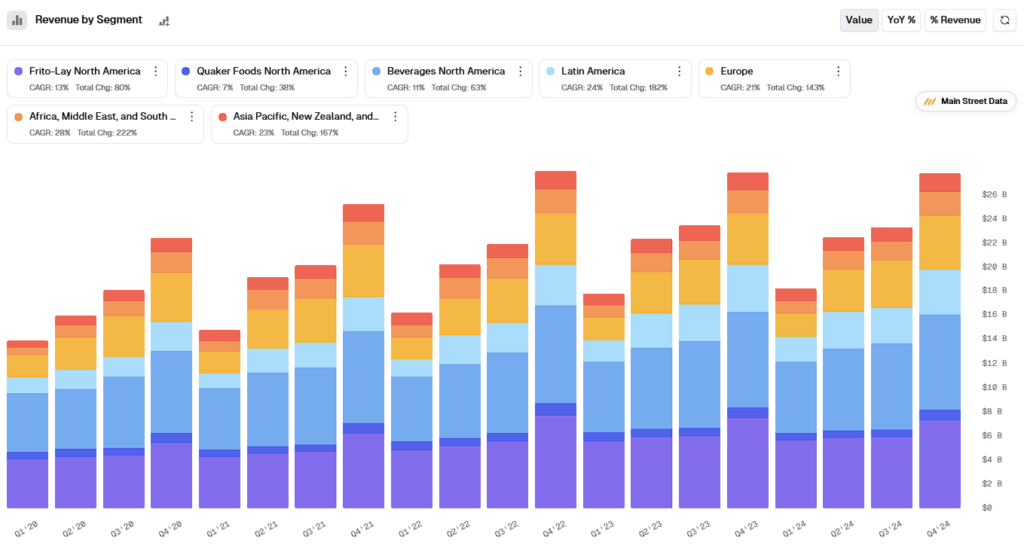

Even though PepsiCo’s strategy is built on slow growth and dividends, the company has experienced an interesting growth trend over the past five years, posting a CAGR of around 6.5%. This growth was primarily driven by the pandemic, which significantly increased spending as people ate more at home and dined out less.

However, such growth rates are unlikely to be repeated anytime soon. Shareholders may be lucky if PepsiCo can grow its top line in the low to mid-single digits. This is because PepsiCo’s products face increasing resistance as consumers choose more health-conscious options and turn to GLP-1 weight-loss drugs. These drugs already have around 15 million regular users in the U.S. As a result, PepsiCo’s Frito-Lay North America segment saw operating profits drop by 7% in FY2024, with organic volume falling 0.5% year-over-year.

PepsiCo’s go-to strategy to drive volume growth and efficiency in this segment is raising prices and adjusting package sizes. As CEO Ramon Laguarta explains: “We’re going to have much more surgical offerings to consumers, especially around price partitions. I think we can manage pricing and sizing in a way that gives consumers options without diluting the pricing of our business or the category.”

As the market increasingly sees PepsiCo as a food company and the company works to pivot the snack category back to growth, we’ve seen the stock underperform. The real question is whether PepsiCo is facing a true crisis, producing foods no longer popular with the broader public, or if this is just a temporary trend in consumer behavior.

Is PepsiCo’s Dividend Strategy Sustainable?

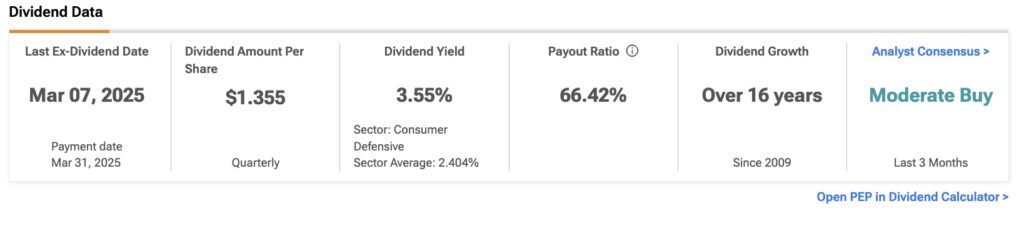

Regardless of PEP’s share price gyrations, passive income investors care about PepsiCo’s ability to consistently distribute dividends to shareholders. PepsiCo has rightfully claimed its title of “Dividend King” following its long history of paying and increasing dividends for at least 52 consecutive years. Once again, it was good news when PepsiCo announced a 5% dividend increase this year, well above inflation, although it was lower than the 7% increase from the same period last year.

Currently, PepsiCo offers a dividend yield of 3.55%, which is relatively strong compared to other U.S. dividend stocks. But of course, just paying a dividend isn’t enough—what matters most is how sustainable that payment will be in the future.

Looking at PepsiCo’s free cash flow generation in 2024, we see the company produced $7.19 billion. While that’s a dramatic drop of 9.2% from the previous year, it still represents a 2.5% compound annual growth rate (CAGR) over the last five years. However, last year, the free cash flow generated wasn’t enough to cover the $7.22 billion in dividends distributed. This is a cautionary sign that shouldn’t be ignored.

It’s still unclear how quickly PepsiCo will overcome the headwinds in its snack business and report better growth metrics for free cash flow. On the flip side, the company trades at 16.4x cash flows, about 15% below its historical average over the last five years. The market does expect operating cash flows to increase by 7.2% in 2025, but that’s still short of the growth rates seen in 2023 and 2024.

Is PepsiCo a Buy or Sell?

On Wall Street, PEP stock carries a Moderate Buy consensus rating based on nine Buy, seven Hold, and zero Sell ratings over the past three months. PEP’s average price target of $164.43 per share implies approximately 10% upside potential over the next twelve months.

PepsiCo’s Dividend Outlook Clouded by Structural Challenges

PepsiCo remains a renowned defensive stock with a low beta and attractive dividends, but whether the current moment is a good time to initiate a long position is another matter. There are some critical issues that make me uncomfortable about the company’s ability to sustain its appeal to passive income investors. Specifically, the headwinds in its snack segment— which could be structural—continue to impact the company’s cash generation, making it challenging to cover dividends adequately and sustainably. This is a key factor for me when selecting dividend stocks, as it only makes sense to include them in a portfolio if they can provide long-term stability.

Given the above, I prefer to stay cautious on PepsiCo for now. More clarity is essential on how quickly—and if—the snack segment can recover in terms of volume and operating margins to get PepsiCo’s cash generation back on a sustainable path.