Volatility has taken center stage in 2025. The year kicked off on the heels of a long-running bull market, but mounting concerns over President Trump’s tariff agenda and weakening consumer confidence have rattled investors and weighed on stocks.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

As bulls and bears battle it out, JPMorgan Global Investment Strategist Alan Wynne weighs both sides of the argument – ultimately tilting toward cautious optimism.

“Every story has three sides: the bull case, the bear case and reality… We sympathize with the bears: Risks still exist to our outlook. The tariff overhang could cause a wait-and-see approach towards capital allocation and slower growth. Increased goods inflation could persist if supply chains are in fact reshored,” Wynne opined. “We think the bulls are right about inflation. Inflation expectations still remain anchored, and hard data has held up despite a shift in sentiment. In fact, poor sentiment may even present an opportunity. Going back to 1971, investing in the S&P 500 during the nine consumer sentiment troughs led to an average +24% return in the next 12 months,”.

“We think that investing in U.S. equities from here can still provide attractive returns into year-end,” the strategist summed up.

Taking that view to heart, JPMorgan’s stock analysts are pointing to a handful of names they believe are primed to outperform in the months ahead. We popped the hood on the TipRanks platform to dig into the data behind two of their picks. Let’s dive in.

Freeport-McMoRan (FCX)

First on our list is Freeport-McMoRan, a mining company based in Phoenix, Arizona. Freeport-McMoRan operates in both North and South America and has extensive copper and molybdenum assets on both continents. In addition, the company also operates the Grasberg minerals district in Indonesia, on the island of New Guinea – this asset is one of the world’s largest deposits of both copper and gold.

While stubborn inflation and increased costs of metals production have put pressure on Freeport-McMoRan, the company does have some potential tailwinds gathering. The push toward increased use of electric vehicles, of all types, along with increased power demand from data centers, has put copper in high demand. In addition, President Trump’s tariffs are targeting, among other things, imported copper – and Freeport-McMoRan owns and operates seven active copper mines in North America, in the states of Arizona and New Mexico. These mines also produce notable amounts of gold and silver, and the company’s North American asset portfolio includes the potential for long-term development of significant untapped metal reserves.

We can note here that FCX shares are up 21% since March 10. The gains come as prices for copper are climbing – and have reached $5.13 per pound, close to record levels. Along with the tariffs and the company’s leading role as a domestic supplier of copper in the U.S., high prices for the metal are strongly supportive of the stock.

Turning to the last reported financial results, from 4Q24, we find that earnings beat expectations while revenues missed. The top line, of $5.72 billion, was down 3.2% year-over-year and fell shy of the forecast by $270 million; the company’s earnings, reported as a non-GAAP EPS of 31 cents, beat expectations by 9 cents per share.

Analyst Bill Peterson, in his coverage of FCX for JPMorgan, notes the company’s strong North American copper position as the chief strength. He writes, “Our Overweight rating reflects our view US copper import tariff risk is likely to maintain premium pricing for the company’s US-based footprint for the foreseeable future, which should directly benefit the company’s bottom line given legacy NOLs and no royalties both in the US. As such, we expect an inflow into the US market given the attractive arbitrage, pressuring RoW inventories and potentially driving LME pricing higher in the coming months. Longer-term, we see energy-transition demand and lagging mine supply deepening current deficits and supporting higher through-the-cycle copper pricing too. Taken together with easing capex next year, the company should generate a significant amount of additional FCF, which can support the company’s base and performance-based payout framework.”

Peterson’s Overweight (i.e., Buy) rating is complemented by a $52 price target, pointing toward an upside of 25% for the next 12 months. (To watch Peterson’s track record, click here)

This stock gets a Moderate Buy consensus rating from the Street’s analysts, based on 13 recent reviews that include 8 Buys and 5 Holds. The shares are currently trading for $41.61 and have an average target price of $49, suggesting that the stock will gain 18% by this time next year. (See FCX stock forecast)

IAC/InterActiveCorp (IAC)

The second stock we’ll look at is IAC, a holding company in the tech domain with a portfolio of internet and media names. The company dates back to 1996, when it was founded as HSN, the parent-holding company of the Home Shopping Network; today, IAC’s network of media properties includes Better Homes & Gardens, Investopedia, People, Daily Beast, and The Spruce, to name just a few. Most of these are wholly owned subsidiaries – but the company is currently in the process of spinning off its full ownership stake in Angi.com, the home services platform. The spin-off transaction is to be completed this month, with direct ownership of Angi transferring to existing IAC shareholders.

Shifting Angi out of the portfolio is intended to allow IAC to focus on its other properties. The company has already announced plans to build its monetization efforts at Dotdash Meredith and to make efforts at growing the Care.com site.

The company is also in the process of making changes to its upper management. Once the spin-off is complete, IAC’s CEO will be leaving his role and will become instead an advisor to the firm. IAC does not intend to replace its CEO, and with his departure, the company’s top executive officers will report directly to the firm’s Senior Executive and Chairman, Mr. Barry Diller.

IAC’s changes come at a time when its financial results have been trending downwards. The company’s revenue in 4Q24, the last period reported, came to $989.3 million, down 6.7% year-over-year although the figure beat the forecast by $55 million. The company’s EPS in the quarter came to a net loss of $2.39, a sharp change from the net profit of $3.70 per share reported in 4Q23. The current EPS missed expectations by $2.65 per share.

On a more positive note, IAC generated positive cash flows in 2024. For the full year, the company’s net cash from operating activities was up $165 million, to a total of $355 million. Free cash flow also increased by $241 million to reach $289 million for the year.

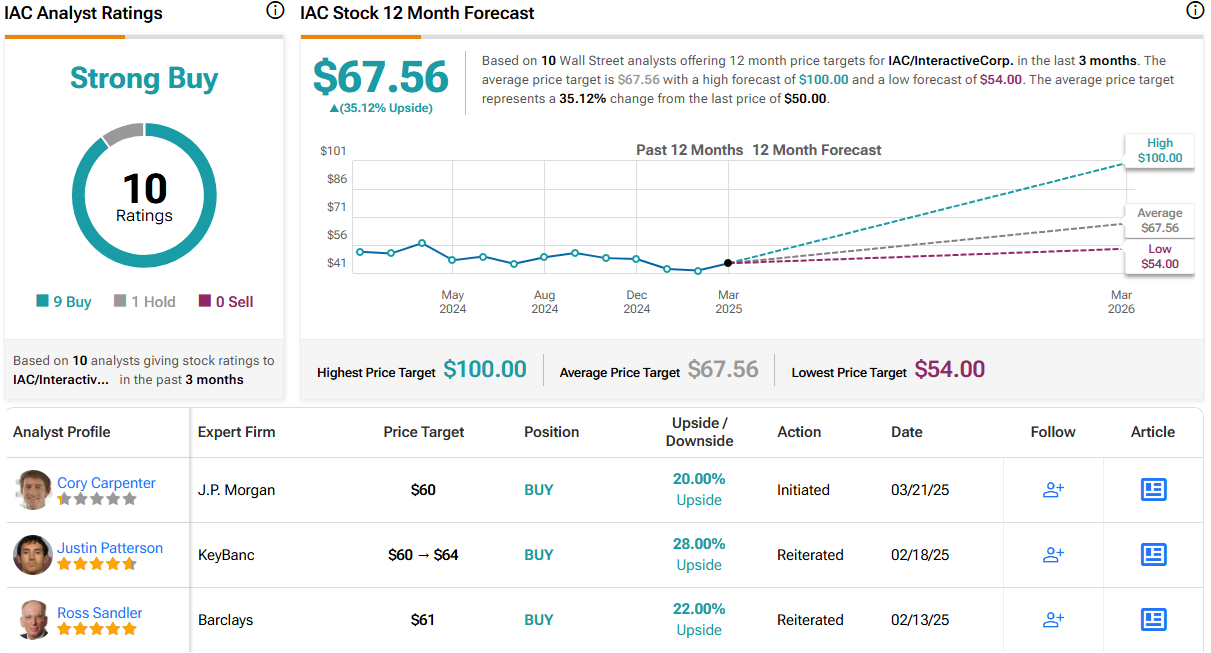

Covering this stock for JPM, analyst Cory Carpenter sees the changes in progress as net positives in the long run and writes of the stock, “IAC operates a portfolio of assets that includes public equity stakes in MGM (22% ownership) and ANGI (84% ownership), wholly-owned Dotdash Meredith and Care, Turo stake (32% ownership), ~$1B cash, & more. IAC shares currently trade near the value of its equity stakes in MGM/ANGI and cash, which means investors essentially receive all of its portfolio companies that we value at ~$1.5B for free. We think the Angi spin should serve as a catalyst to unlock portfolio value by simplifying the story and removing a business that has been an overhang on shares.”

Carpenter quantifies his stance on IAC with an Overweight (i.e., Buy) rating and his $60 price target implies a 20% share price appreciation in the coming year. (To watch Carpenter’s track record, click here)

There are 10 recent analyst reviews on file for IAC, and their lopsided split – 9 to 1 in favor of Buy over Hold – gives the stock its Strong Buy consensus rating. The shares are priced at $50, and the $67.56 average price target is even more bullish than the JPM view, suggesting a one-year upside potential of 35% (See IAC stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.