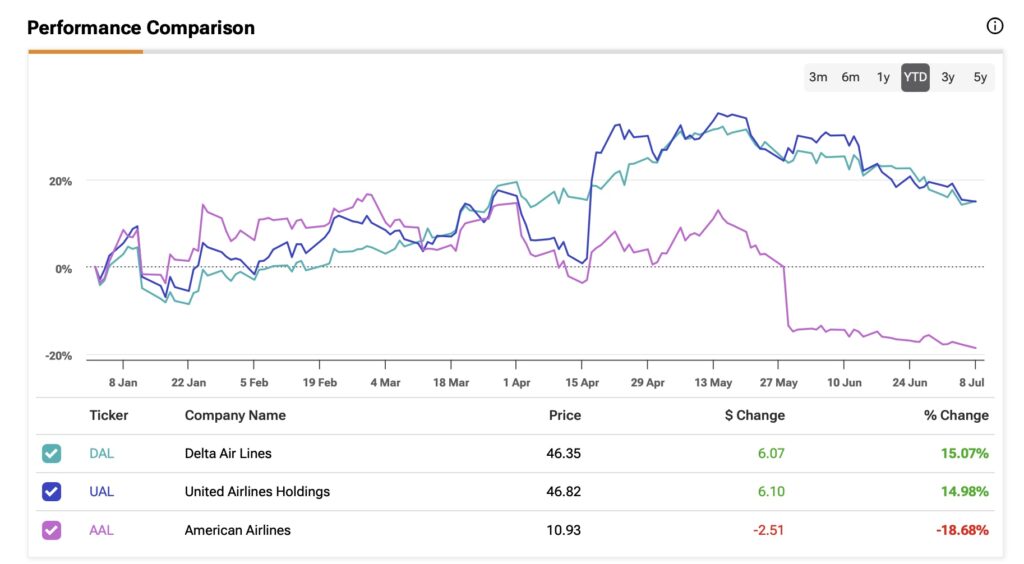

I hold a bearish position on American Airlines (NASDAQ:AAL), a U.S. legacy carrier that has notably underperformed its domestic peers, as you can see in the comparison below. The Fort Worth, Texas-based airline faces significant challenges, including a highly leveraged balance sheet, structural issues in its cost management, and an outlook for Q2 that fell below market expectations. These factors have contributed to a strong bearish sentiment surrounding AAL stock.

Claim 55% Off TipRanks

- Unlock hedge fund-level data and powerful investing tools for smarter, sharper decisions

- Discover top-performing stock ideas and upgrade to a portfolio of market leaders with Smart Investor Picks

Consequently, my pessimistic stance on American Airlines reflects concerns about its financial stability and competitive positioning within the industry. In this article, I will outline five reasons supporting this view.

#1. Weak Trading Momentum in AAL

Shares in American Airlines have been on a downward trend over the last 12 months, declining by more than 40%.

Despite a strong recovery from November last year to mid-May this year, during which market sentiment improved and shares traded above $15, recent developments have reversed this trend. The anticipation of downward revisions in Q2 earnings and the departure of a key company executive has pushed the stock back below $11 per share.

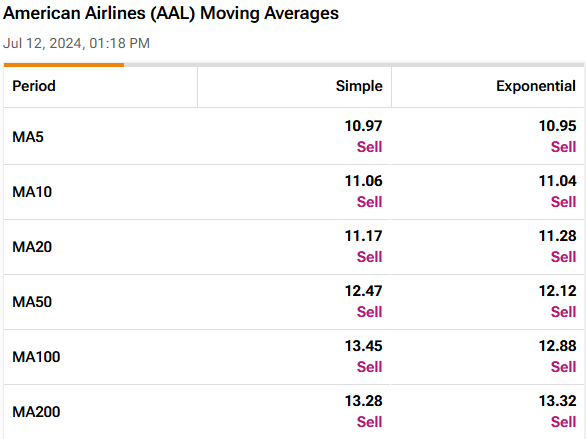

Analyzing current momentum trends, both short- and longer-term moving averages indicate a bearish outlook. These indicators, commonly used by technical analysts to identify support and breakout patterns, highlight the current situation. American Airlines’ 50-day simple moving average stands at $15.48, the 100-day moving average at $27.10, suggesting significant resistance levels.

#2. Slower Post-Pandemic Operational Recovery Compared to Peers

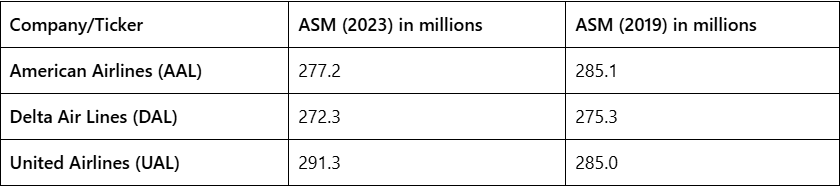

To better assess an airline’s operational capacity relative to demand, available seat miles (ASM) is a crucial metric.

After gradually recovering from the COVID-19 pandemic, in 2023, American Airlines reported flying 277.72 million seat miles, slightly below the 285.08 million flown in 2019. Alongside Delta Air Lines (NYSE:DAL), which also missed reaching pre-pandemic ASM levels by a small margin, American Airlines lagged in ASM recovery compared to United Airlines (NASDAQ:UAL), which exceeded its 2019 ASM figures.

It wasn’t until Q1 2024 that American Airlines managed to surpass its pre-pandemic ASM levels. One factor contributing to the airline’s lower capacity might be its limited exposure to coastal markets and higher leverage compared to its peers, thereby constraining its ability to rapidly increase operations.

#3. Balance Sheet Vulnerabilities

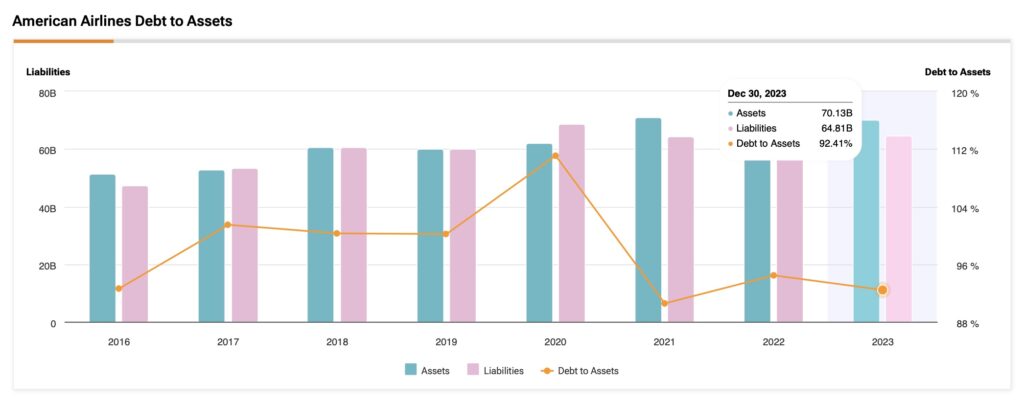

When looking at the balance sheet, American Airlines stands out as the most heavily burdened airline in the U.S. market by a significant margin compared to its peers. Currently, its net debt represents approximately 48% of all its total assets, whereas Delta and United maintain lower ratios, with net debt representing 30% and 28% of their total assets, respectively. Last year, liabilities funded about 92% of AAL’s total assets.

This high level of leverage has led American Airlines to incur substantial net interest expenses, amounting to $1.55 billion in 2023 alone. With operating income reported at $3.87 billion for the same period, this implies that only 60% of its operating income is retained after accounting for interest payments on its debt.

#4. Ongoing Concerns Surrounding Cost Structure

Another reason to be skeptical about investing in American Airlines stock is its lower cost structure compared to its legacy peers, especially Delta.

When considering AAL’s passenger revenue per available seat mile (PRASM) of 16.25 cents and cost per available seat mile (excluding items and fuel) (CASM-ex) of 13.49 in Q1 2024, it shows a profit of 2.76 cents per unit. In contrast, Delta reported a per unit margin of 2.90 in Q1, which is significantly lower than its pre-pandemic levels.

American Airlines already had the lowest pre-pandemic per unit margins among its peers, suggesting that this lower margin may be more indicative of an ongoing challenge rather than a temporary situation.

#5. Doubts in Valuation Reflect Waning Confidence

American Airlines trades at a forward P/E ratio of 5.4x, which is a discount compared to Delta at 7x and a premium compared to United at 4.6x. In my view, American Airlines’ weaker balance sheet theoretically justifies its discounted valuation relative to Delta, but it does not warrant a premium compared to United.

However, considering that U.S. legacy airlines as a whole are trading at relatively low valuation multiples, this likely reflects investors’ overall lack of confidence in these stocks rather than a perception of them being undervalued.

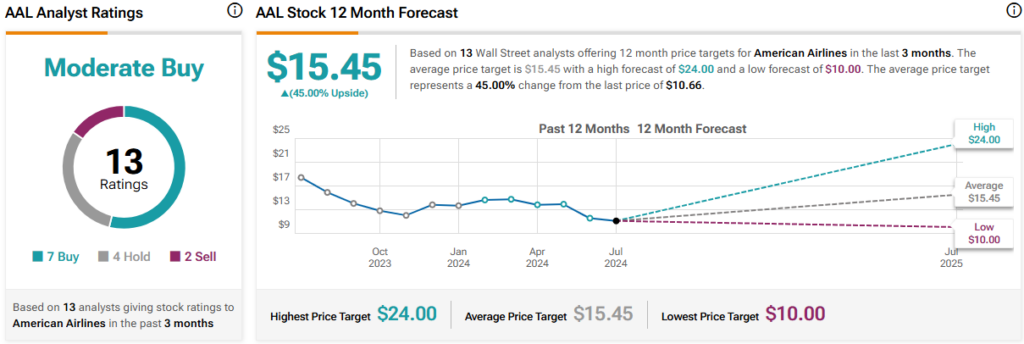

Is AAL Stock a Buy, According to Analysts?

Out of the 13 Wall Street analysts covering AAL stock, only two share my bearish stance on the legacy airline. Seven analysts have a bullish outlook on American Airlines, while the remaining four are neutral, resulting in a Moderate Buy consensus rating. The average AAL stock price target stands at $15.45, indicating upside potential of 45% for AAL.

Conclusion

American Airlines’ business fundamentals indicate that it is currently in a precarious position, performing significantly worse than its legacy U.S. peers. Given the reasons highlighted throughout this article, I believe that AAL represents the riskiest investment among the U.S. big three carriers today. Coupled with the inherently risky and volatile nature of the airline industry, this leads me to adopt a bearish position on American Airlines.