After another volatile week for AI infrastructure stocks, Sandisk (NASDAQ:SNDK) stock surged 9.5% on Thursday as money rotated back into memory and storage names following Nvidia’s latest earnings report and bullish commentary surrounding long-term AI spending. Nvidia’s forecast reinforced expectations that hyperscalers could continue pouring hundreds of billions into AI infrastructure over the coming years, a backdrop that directly benefits NAND memory suppliers like Sandisk.

Meet Samuel – Your Personal Investing Prophet

SNDK has a long & short ETF? Explore SNXX & SNDQThat AI spending thesis has already been transforming the memory sector into one of the market’s hottest areas. And among those names, Sandisk has separated itself from the pack in a massive way. We’re talking about a stock that has climbed a ridiculous 3,850% over the past year.

So, does that make it a risky proposition right now? Not at all, says one investor that goes by the pseudonym of Bay Area Ideas (BAI).

“While some may point to the stock rally as an indication of a bubble forming, I would say that a look at the valuation shows that the company is actually still undervalued right now based on the fundamentals,” BAI said.

The investor points out that the company’s recent fiscal third-quarter’s top-line results were “truly breathtaking,” underscoring the powerful tailwinds currently supporting the business. Sandisk reported revenue of $5.95 billion, representing a 251% year-over-year increase and a 97% quarter-over-quarter jump. The figures reflect a sharp acceleration, indicating strengthening momentum. The company also significantly exceeded analyst expectations, surpassing estimates by $1.22 billion.

“This is a mind-blowing amount of outperformance and shows that we are witnessing something truly extraordinary,” BAI opined.

When assessing the performance beyond revenue, there are clear indications that strong memory demand is driving exceptional results elsewhere. Gross margin expanded by 55.7 percentage points YoY, a level of improvement “almost unheard of,” and highlighting significant pricing strength.

Operating efficiency also shows positive momentum, with operating expenses rising only 8% sequentially and 17% YoY, despite a substantial acceleration in top-line growth.

Meanwhile, adj. EPS came in at $23.41, beating expectations by a huge $8.75, suggesting that favorable memory pricing conditions are benefiting both revenue and profitability.

Alongside the strong Q3 results, Sandisk also issued a “blowout” Q4 outlook, guiding above Street estimates. For revenue, the midpoint of the guided range implies YoY growth of 321%. This represents further acceleration compared with Q3’s already strong growth rate.

Those are all impressive metrics that help explain why the stock is outperforming. The thing is, even accounting for the share price surge, BAI thinks the valuation isn’t really that high.

A forward price-to-earnings (P/E) ratio of 21.43 does not appear particularly elevated given the current business momentum and profitability trends. At present levels, BAI believes the company’s fundamentals and outlook can “more than justify the valuation.”

Accordingly, BAI rates SNDK shares a Buy. (To watch Bay Area Ideas’ track record, click here)

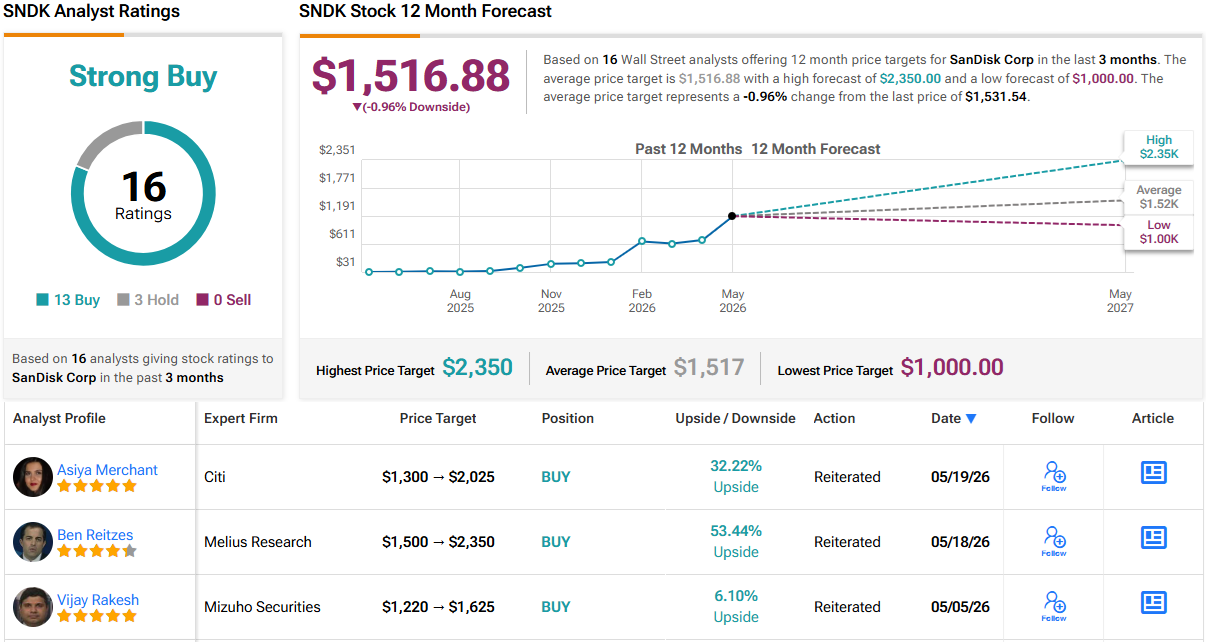

That take chimes with the general Street view, although the average price target has not fully kept pace with the stock’s explosive rally in recent months. SNDK currently boasts a Strong Buy consensus rating based on 16 analyst reviews, including 13 Buy ratings and just 3 Holds. The average price target stands at $1,517, slightly below the current share price. Yet, upcoming analyst revisions over the next few weeks may push those targets higher. (See SNDK stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured investor. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.