Investors are eagerly awaiting chip giant Nvidia’s (NVDA) fiscal first-quarter earnings on May 20. Ahead of Q1 FY27 earnings, top Wells Fargo analyst Aaron Rakers boosted his price target for Nvidia stock to $315 from $265 and reiterated a Buy rating. Rakers is optimistic about the company’s Q1 results and raised his data center revenue and EPS (earnings per share) estimates for Fiscal 2027-Fiscal 2029 to reflect the potential expansion of GW (gigawatt) capacity.

Meet Samuel – Your Personal Investing Prophet

Explore NVDS for 2X short leverage on NVDAWith more than $1 trillion in Blackwell and Rubin AI chip orders through 2027, Rakers estimates that over $840 billion remains after Q4 FY26. Moreover, the analyst sees further upside, as this forecast includes only Blackwell and Rubin orders and not other products, such as Groq 3 LPX, a rack-scale AI inference accelerator designed for Vera Rubin supercomputing architecture.

Wells Fargo Analyst Raises NVDA Estimates

Rakers stated that, given continued indications that compute demand is outpacing supply, he believes that a major factor boosting Nvidia’s data center revenue is the company’s ability to expand its AI infrastructure capacity (as measured in gigawatts). Notably, he expects Nvidia to increase its GW capacity of GPU compute infrastructure from about 9.2 GW in FY26 to nearly 15.7 GW in FY27, 20.8 GW in FY28, and 25.2 GW in FY29.

Consequently, Rakers now expects Nvidia’s Fiscal 2027, 2028, and 2029 data center revenue at $352.5 billion (up 82% year-over-year), $503.9 billion (up 43%), and $624.8 billion (up 24%), respectively, with these estimates surpassing the Street’s current projections by 3%, 11%, and 15%, respectively.

Furthermore, citing strong intra-quarter data points, Rakers increased his Q1 FY27 revenue and EPS estimates from $78.1 billion and $1.74 to $80.3 billion and $1.78, respectively, both ahead of the Street’s projections. The analyst’s revised expectations reflect a higher data center revenue estimate of $74.6 billion (year-over-year growth of 91%), up from the previous estimate of $72.2 billion. Rakers continues to expect a gross margin of 75.1%, compared to the company’s guidance of 74.5% to 75.5%.

Additionally, Rakers expects Nvidia to signal continued strong demand for its Blackwell AI chips into Q2 FY27, ahead of the launch of its Vera-Rubin platform. Accordingly, he raised his data center, total revenue, and EPS estimates for the fiscal second quarter. The analyst now expects Q2 2027 revenue and EPS of $83 billion and $1.98, respectively.

Is NVDA a Good Stock to Buy Right Now?

Wall Street expects Nvidia to report EPS (earnings per share) of $1.74, reflecting 115% year-over-year growth. Revenue is estimated to rise 78.4% to $78.62 billion.

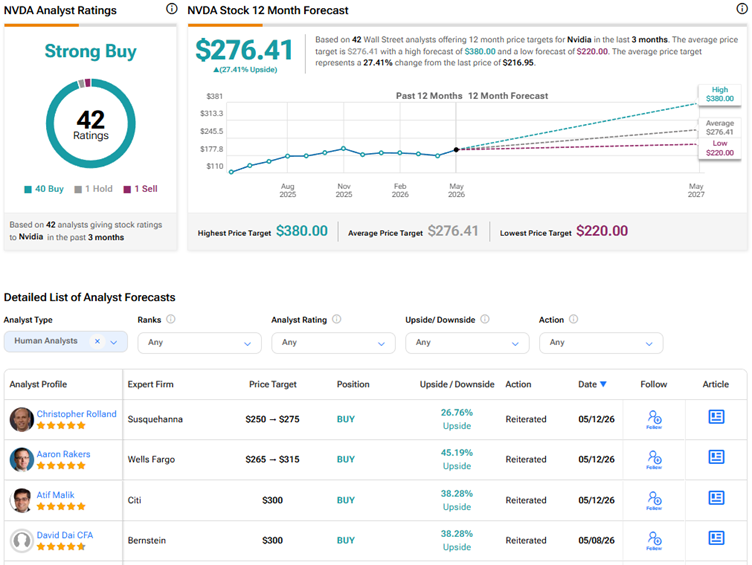

Ahead of Q1 earnings, Nvidia stock earns a Strong Buy consensus rating based on 40 Buys, one Hold, and one Sell. The average NVDA stock price target of $276.41 indicates 27.4% upside potential. NVDA stock has risen more than 17% year-to-date.