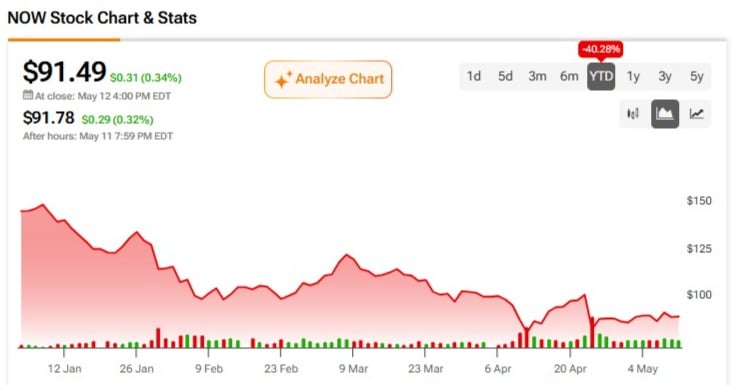

ServiceNow (NOW) keeps its long-term artificial intelligence (AI) bull case intact even after a mixed Q1 and the stock’s sharp sell-off. I remain bullish on NOW despite the stock being down more than 41% year-to-date. ServiceNow is one of the most important enterprise software platforms, helping companies automate workflows across IT, HR, customer service, security, and other business functions.

Meet Samuel – Your Personal Investing Prophet

- Start a conversation with TipRanks’ trusted, data-backed investment intelligence

- Ask Samuel about stocks, your portfolio, or the market and get instant, personalized insights in seconds

The latest quarter was not perfect, especially given margin pressure and some deceleration in organic current remaining performance obligation (cRPO) growth, but I believe the sell-off is too harsh relative to the company’s long-term AI opportunity and strategic positioning within AI workflows.

Q1 Was Mixed, but the Core Business Still Looks Healthy

ServiceNow’s first-quarter results were solid, though not strong enough to satisfy a market that has become very skeptical toward software stocks. Subscription revenue grew 19% year-over-year on a constant-currency basis, in line with the high end of guidance. cRPO grew 21% in constant currency, modestly above management’s prior outlook.

However, the quality of the beat was not as clean as investors wanted. Management noted a 75-basis-point headwind to subscription revenue growth due to delayed on-premises deals in the Middle East, and guidance implied slower organic cRPO growth in Q2. The Armis acquisition also creates near-term margin pressure, with management lowering its 2026 operating margin outlook to 31.5% and free cash flow margin outlook to 35%.

Still, I view these issues as manageable rather than thesis-breaking. The quarter reflected geopolitical and acquisition-related noise, not a breakdown in ServiceNow’s competitive position.

AI Momentum Is the Key Bullish Signal

The most important takeaway from Q1 was the strength of ServiceNow’s AI business. Management raised the target for its full-year NOW Assist customer spending in annual contract value (ACV) to $1.5 billion from $1 billion. That is a major increase and suggests customers are moving from AI experimentation toward real production use cases.

NOW Assist customers with an ACV of more than $1 million grew more than 130% year-over-year. The company also reported 16 deals with ACV above $5 million, up 80% year-over-year. These numbers matter because they show that AI is not just a marketing story for ServiceNow. It is becoming a meaningful revenue driver.

ServiceNow’s AI advantage comes from its deep workflow context. Raw data may become increasingly commoditized, but institutional process logic is harder to replicate. ServiceNow has spent years embedding itself into enterprise workflows, and that gives its AI agents a stronger foundation to sense, decide, act, and govern across complex business processes.

ServiceNow’s Platform Moat Remains Strong

ServiceNow is not simply selling standalone AI tools. It is building AI into a workflow platform that already sits at the center of many large enterprises. That distinction matters.

AI agents need more than large language models. They need governance, auditability, business context, workflow execution, and integration with existing systems. ServiceNow’s platform is well-positioned to offer these because it already connects business functions across IT, HR, security, and customer operations.

The company’s “Blueprint for Agentic Business” framework — Sense, Decide, Act, and Govern — shows how ServiceNow is positioning itself as an enterprise-grade AI orchestration layer. In my view, this makes NOW more likely to be an AI winner than an AI loser.

Acquisitions Add Noise, but Also Expand the Opportunity

Recent acquisitions, including Armis, Veza, Pyramid, and Moveworks, have made the financial picture messier. Armis alone is expected to reduce fiscal 2026 operating margin by 75 basis points and free cash flow margin by 200 basis points.

That said, these deals also strengthen ServiceNow’s AI and security capabilities. Moveworks, for example, has already exceeded expectations and closed six deals with net new ACV above $1 million. These acquisitions may create short-term margin friction, but they could improve ServiceNow’s ability to offer broader AI-driven automation over time.

Valuation Is Mixed, but Not Unreasonable for the Quality

ServiceNow is not obviously cheap on every metric. Its price-to-sales ratio is about 7, above the sector median of around 4, and its PEG ratio of 1.58 also looks elevated compared with the sector median of around 1.

However, its price-to-operating-cash-flow ratio of around 17.52 is below the sector median of around 20. That matters because ServiceNow remains a highly cash-generative business with strong recurring revenue, durable enterprise demand, and a large addressable market estimated at more than $275 billion.

Given the stock’s 41% year-to-date decline, I believe the market is pricing in too much skepticism around software and not enough credit for ServiceNow’s ability to monetize AI.

Wall Street’s View

According to TipRanks, ServiceNow carries a Strong Buy consensus rating, with 34 Buy, four Hold, and no Sell ratings. Based on 38 Wall Street analysts, the average price target is $142.03, implying 55.24% upside from the last price of $91.49.

Conclusion

ServiceNow’s Q1 was not flawless. cRPO growth decelerated, acquisitions pressured margins, and geopolitical delays created some uncertainty. However, the long-term AI story remains intact.

The company is deeply embedded in enterprise workflows. NOW Assist momentum is accelerating, and ServiceNow has a credible path to becoming a core AI automation layer for large organizations. After the sharp year-to-date decline, I believe the risk/reward looks attractive. I remain bullish on NOW.