AI has been shaping the market narrative for several years now. Companies operating in AI-related fields have seen massive real-world impact, and that has fed into stocks’ valuations, which have regularly soared to new highs.

Meet Samuel – Your Personal Investing Prophet

200% short exposure to NVDA with NVDSBut given the amount of hype surrounding the game-changing tech, there has been plenty of discussion around the possibility of an AI bubble, one that will eventually pop and send the market and the economy into a downward spiral.

However, billionaire investor Ken Fisher has a retort to that thesis, arguing that all the talk of an AI bubble might mean there actually isn’t one.

“The widespread discussion of AI as a bubble indicates fear in the market, which is the opposite of a real bubble characterized by euphoria and a belief in a fundamentally changed world,” Fisher, who has a net worth of $13.2 billion, said.

Fisher thinks today’s AI boom is completely different from the dot-com bubble of the late 1990s. Back then, many unprofitable startups depended on constant stock offerings to stay afloat, whereas today’s leading AI players are large, highly profitable companies financing their initiatives through strong cash flow and solid balance sheets.

That does not mean Fisher is blindly bullish on every AI stock, though. While he remains heavily invested in several of the market’s largest AI names, recent portfolio changes show he has been leaning far more aggressively into one industry giant while reducing exposure to another. Let’s take a closer look at what Fisher has been doing with Nvidia (NASDAQ:NVDA) and Micron (NASDAQ:MU).

Nvidia

We’ll start with Nvidia, recognized today as the AI company, a status built on its standing as the world’s most valuable company. Nvidia boasts an all-conquering data center business, yet hark back to the start of the decade and the chipmaker was primarily known as a manufacturer of GPUs aimed at the gaming market.

Gaming used to be Nvidia’s primary revenue driver, and it was not until the July 2020 quarter that the company’s data center business surpassed gaming for the first time. In that period, data center revenue reached $1.75 billion, ahead of gaming revenue at $1.65 billion. Although gaming temporarily regained the lead in the following quarters, the balance changed for good as generative AI entered the frame and gathered momentum. By the April quarter of 2022, data center revenue had decisively moved ahead of gaming and since then, the gap has continued to expand.

As it turned out, Nvidia’s pioneering GPUs proved ideally suited for the intensive mathematical processing required in machine learning. As businesses rushed to develop their own AI systems, demand for those chips soared, fueling a huge increase in Nvidia’s data center revenue. That translated into regular beat-and-raise reports that led to significant market share gains and ultimately helped establish the company as today’s market leader.

A look at the segment’s most recent revenue haul gives an idea of how huge the growth has been. Today the data center segment accounts for more than 90% of revenue and in its last reported quarter, it generated record sales of $62.3 billion, up by 75% year-over-year.

Nvidia will release its latest quarterly report this Wednesday (May 20) and Fisher must believe the Jensen Huang-led company will deliver again. During Q1, he bought 2,502,033 shares, holdings currently worth almost $590 million.

Interestingly, in recent months, with agentic AI and a memory bottleneck in focus, NVDA has underperformed peers, but Cantor analyst C.J. Muse notes that not only is the business flourishing, that factor opens up a big opportunity.

“Compute is extraordinarily tight, where we believe that NVDA is sold out for both 2026 and 2027,” Muse, who ranks in 9th spot amongst the thousands of Wall Street stock experts, said. “Agentic AI, particularly at Anthropic and OAI, has confirmed the massive ROIC for AI. This, in turn, has only led to even greater demand for Compute. And considering the many bottlenecks throughout the Semi supply chain, we believe there is clear support for a vision for Y/Y growth at NVDA through 2028-2029 at a minimum. At the same time, rising fears of competition from In-House Silicon and AMD and the sustainability of margin stacking on HBM have led to a massive compression to NVDA’s multiple, which is now at an incredibly low 14x stretch goal EPS of $15-16 in CY27.”

Accordingly, the 5-star analyst rates NVDA shares as Overweight (i.e., Buy), while his $350 price target points toward 12-month returns of 55%. (To watch Muse’s track record, click here)

The Street’s average target is a less exuberant $280.31, but that figure still factors in one-year gains of 24%. On the rating front, based on a mix of 40 Buys and 1 Hold and Sell, each, the stock claims a Strong Buy consensus rating. (See NVDA stock forecast)

Micron

Nvidia’s rise has been extraordinary, but Micron’s recent ascent has been no less fascinating to watch. Micron operates in the computer memory industry, one that has historically been highly cyclical, with revenue and profitability fluctuating sharply due to well-defined supply and demand dynamics in areas such as PCs, servers, and smartphones.

But AI has currently changed the rulebook. Demand for memory has surged dramatically, largely because AI workloads require vast amounts of high-capacity, high-speed memory. Training large AI models consumes enormous quantities of DRAM and HBM – both forms of high-performance memory used in active processing, with HBM offering the higher bandwidth needed for advanced AI computations – along with NAND for large-scale data storage, all areas Micron specializes in. And even as the industry increasingly shifts from training models to inference, memory demand remains extremely strong, since inference workloads also require substantial bandwidth and capacity to process AI queries efficiently at scale.

The AI-driven surge in memory demand has pushed customer commitments to unprecedented levels, with Micron already indicating that its entire 2026 HBM supply has been fully allocated. At the same time, limited industry capacity has created a supply imbalance that has sharply lifted memory pricing across the market. These dynamics have sent Micron’s sales, margins, and profits to record levels, and that in turn has fed into a huge market rally. To wit, the shares have gained ~640% over the past year.

Still, that backdrop did not convince Fisher to maintain a large position in Micron. In fact, during Q1, the billionaire sold 30,192 MU shares, reducing his stake by 57% overall. The move suggests he saw limited reason to keep even his already relatively modest exposure to the memory giant.

For Erste Group analyst Hans Engel, despite the huge growth on tap, the memory industry – and therefore Micron – still remains at the mercy of supply and demand dynamics. And that requires a cautious outlook.

“Micron Technology has issued a very high revenue guidance of USD 109 bn for the 2026 financial year due to the very high demand for memory (in particular HBM3E). Micron product sales in the extremely fast-growing HBM segment (high bandwidth memory) are already sold out for the full year 2026. High investments are therefore required to expand production. This reduces the free cash flow. There are also concerns about the long-term sustainability of the memory cycle. In the DRAM segment, which is the largest for Micron in terms of revenue but is growing more slowly, the price trend has cooled recently,” Engel commented.

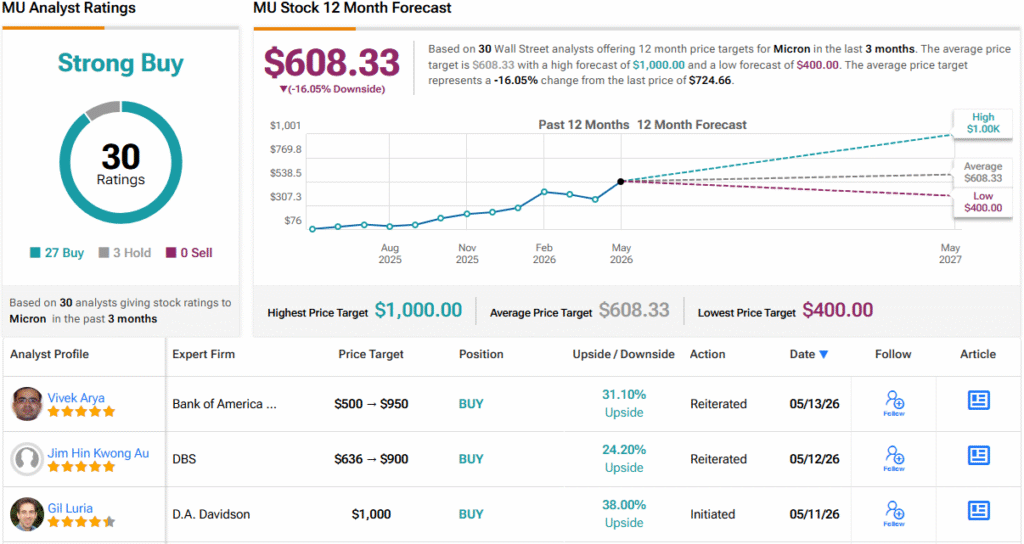

To this end, Engel assigns MU shares a Hold (i.e., Neutral) rating, without offering a fixed price target. (To watch Engel’s track record, click here)

2 other analysts join Engel on the sidelines, yet with an additional 27 Buys, the analyst consensus rates the stock a Strong Buy. However, after the stock’s massive run-up, the average price target of $608.33 now sits 16% below the current share price, suggesting analysts may soon need to reassess their stance on the stock. (See MU stock forecast)

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.