Marvell Technology (MRVL) is a chip company that designs data center, network, and custom silicon products for AI, cloud, and telecom systems. The stock has had a big run ahead of its next earnings report, scheduled for Wednesday, May 27, after the close.

Meet Samuel – Your Personal Investing Prophet

- Start a conversation with TipRanks’ trusted, data-backed investment intelligence

- Ask Samuel about stocks, your portfolio, or the market and get instant, personalized insights in seconds

The stock has rallied in 2026, rising 131.31% year-to-date. The surge has been fueled by strong demand for AI data center chips, upbeat guidance, and rising trust in Marvell’s custom silicon and interconnect growth story.

Still, the setup for earnings is not simple. Wall Street remains bullish, but the stock is now trading above the average analyst price target.

For the upcoming report, analysts expect earnings per share of $0.79 for fiscal Q1 2027. That compares with $0.62 in the same quarter last year.

Meanwhile, MRVL shares extended their rally on Friday, rising nearly 3% to close at $196.33.

AI Demand Is the Main Growth Driver

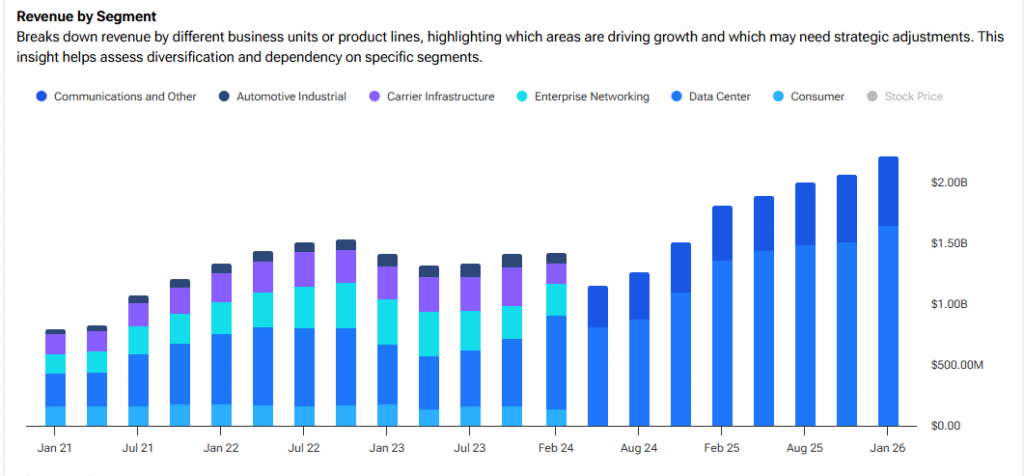

Marvell’s last earnings call gave investors plenty to like. The company reported record quarterly revenue of $2.219 billion, up 22% from the prior year. Fiscal 2026 revenue reached $8.195 billion, up 42%.

More importantly, the data center business continued to lead the story. Data center revenue surpassed $6 billion in fiscal 2026, up 46% from the year before. In Q4, data center revenue reached $1.65 billion, up 21% year-over-year.

Management also gave strong guidance. For fiscal Q1 2027, Marvell guided revenue of $2.4 billion, plus or minus 5%, implying about 27% growth from the prior year at the midpoint. The company also expects fiscal 2027 revenue to approach $11 billion, helped by about 40% growth in data center revenue.

Looking further out, management said fiscal 2028 revenue could reach roughly $15 billion. It also said non-GAAP EPS could be “well over $5.”

That outlook is built around demand for AI data center gear, custom chips, and high-speed interconnect products. Marvell has also moved to strengthen its AI position through the purchases of Celestial AI and XConn.

However, there are risks. Inventory and working capital are rising, costs are moving higher due to recent deals, and demand is still tied closely to large cloud customers. In addition, some of the deal benefits are not expected to show up in a major way until fiscal 2028.

Overall, Marvell enters earnings with strong business momentum and strong analyst support. But after a 131% year-to-date surge, expectations are high. This week’s report will need to show that the AI growth story still has room to run.

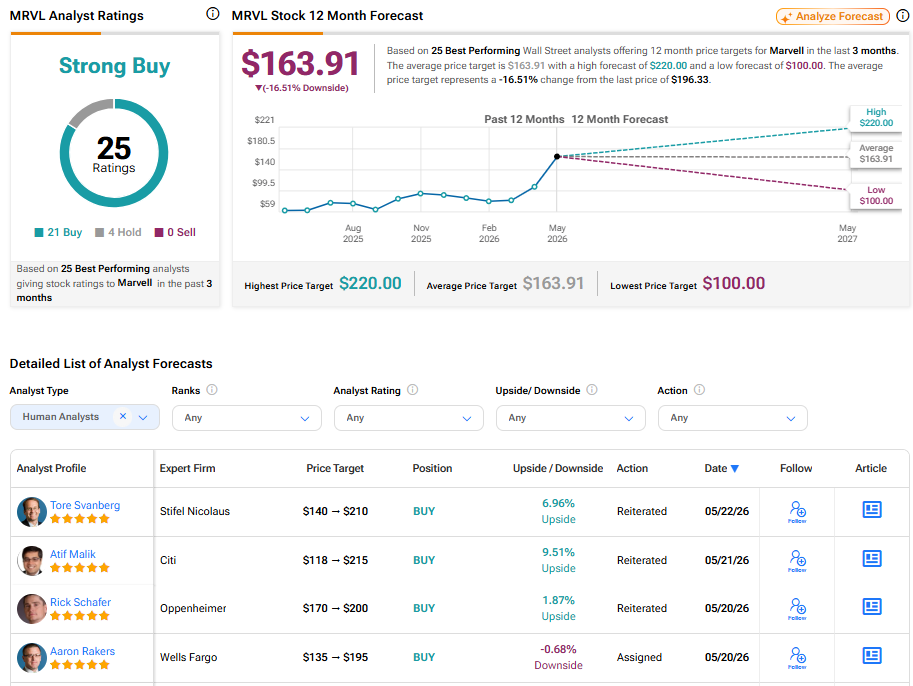

Is MRVL Stock a Strong Buy?

Turning to the Street, Marvell carries a Strong Buy rating based on 25 top analyst ratings. Of those, 21 analysts rate the stock a Buy, while four rate it a Hold. There are no Sell ratings. The average MRVL stock price target is $163.91, indicating about a 16.5% downside from the current price.

However, the high target is $220, while the low target is $100. This gap highlights the key issue ahead of earnings. Analysts like the business, but the stock has already priced in much of the good news. As a result, Marvell may need to deliver strong results and a clean outlook to sustain the rally.