Intuit (INTU) shares declined 10% in after-hours trading even after the software company reported upbeat fiscal third-quarter results and raised its full‑year revenue outlook. Alongside financials, the company confirmed that it will reduce its full-time workforce by 17% to simplify operations and increase speed across the organization. The company expects $300-$340 million in restructuring charges, mostly in Q4.

Meet Samuel – Your Personal Investing Prophet

- Start a conversation with TipRanks’ trusted, data-backed investment intelligence

- Ask Samuel about stocks, your portfolio, or the market and get instant, personalized insights in seconds

Adjusted earnings per share (EPS) of $12.80 topped Wall Street forecasts of $12.5 and increased from $11.65 in the prior-year quarter. Also, revenue of $8.6 billion came in ahead of consensus expectations of $8.54 billion.

Consumer revenue rose 8% to $5.3 billion due to gains across key products. TurboTax revenue grew 7% to $4.4 billion, Credit Karma jumped 15% to $631 million, and ProTax held steady at $278 million. On the business side, Global Business Solutions revenue climbed 15% to $3.3 billion, driven by a 22% rise in QuickBooks Online Accounting and 19% growth in the broader Online Ecosystem, including money and payroll services.

Capital Deloyment Activities

The company repurchased $1.6 billion of stock during the third quarter. Also, Intuit announced a new $8 billion stock repurchase authorization. The buyback program was approved by the board of directors, reflecting confidence in the company’s AI-driven growth strategy.

The board also approved a quarterly dividend of $1.20 per share, payable on July 17, 2026. This marks a 15% increase per share compared to the same period last year.

Full‑Year 2026 Guidance Raised

On the back of its strong Q3, Intuit raised its full‑year outlook. The company now expects:

- Revenue of $21.34 billion to $21.37 billion, up 13-14%. Also, it is above the prior guidance of $21 billion to $21.2 billion. Analysts’ expectation is pegged at $21.25 billion.

- Adjusted operating income up nearly 16%

- Adjusted EPS in the range of $23.80 and 23.85, compared with the previous guidance of $22.98 to $23.18. Further, it is above the consensus estimate of $23.22.

For the fourth quarter, Intuit expects revenue growth of 11-12%, implying sales between $4.22 billion and $4.26 billion, above the consensus of $4.14 billion. Adjusted EPS is projected between $3.56 and $3.62, also topping the consensus estimate of $3.13.

Is INTU a Good Stock to Buy?

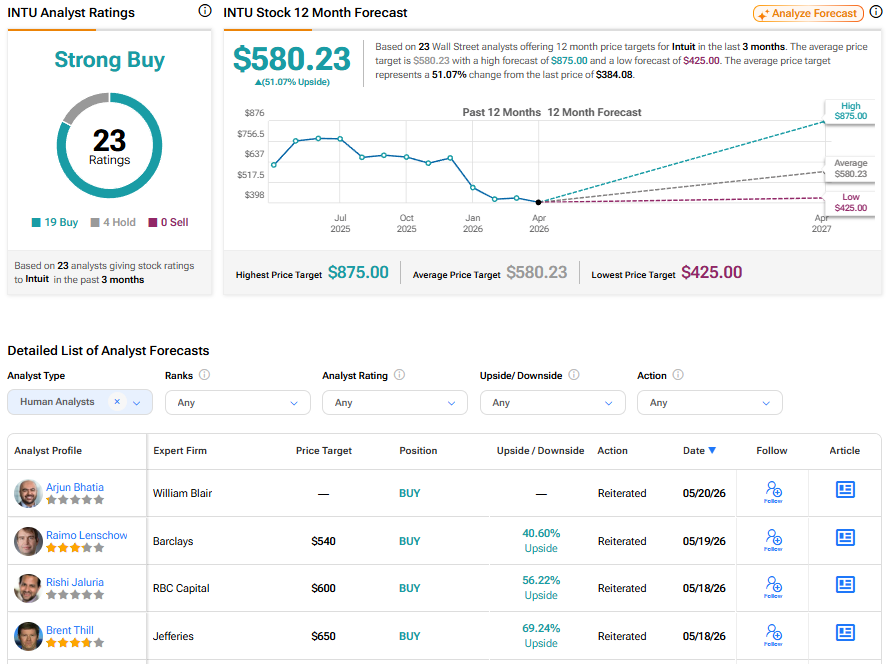

Turning to Wall Street, INTU stock has a Strong Buy consensus rating based on 19 Buys and four Holds assigned in the last three months. At $580.23, the average Intuit stock price target implies a 51.07% upside potential. It’s worth noting that these estimates will likely change following today’s earnings report.