The meltdown in Hims & Hers Health (HIMS) stock has raised doubts about the company’s momentum. The post-earnings sell-off since its Q1 report came earlier this month shows the market did not take the unexpected net loss or the sharp compression in gross margins lightly. Even so, I do not think the broader story has broken.

Meet Samuel – Your Personal Investing Prophet

- Start a conversation with TipRanks’ trusted, data-backed investment intelligence

- Ask Samuel about stocks, your portfolio, or the market and get instant, personalized insights in seconds

Beneath the messy headline numbers, several of this multi-specialty health and wellness platform’s most important long-term growth drivers still appear to be firmly intact. That leaves the recent weakness potentially looking like an attractive entry point for those willing to believe in Hims & Hers’ long-term prospects. That is why I remain bullish on HIMS stock.

The Q1 Post-Mortem: Why the Market Panicked

Even for someone like me who is bullish on HIMS stock, there is no denying that Q1 was rather ugly. Hims reported an unexpected quarterly net loss of $92.1 million, translating to a GAAP earnings per share (EPS) of -$0.40. This was a staggering miss of Wall Street’s break-even-to-$0.01-per-share profit expectation. As you may remember, Hims finally crossed into consistent profitability last year. Therefore, this sudden, dramatic reversal into losses felt like a freezing-cold shower.

In the meantime, total revenue came in at $608.1 million, also missing the consensus estimate of $616.8 million. It represented a meager 4% year-over-year increase, instantly demoting HIMS from its hyper-growth status. To make matters worse, domestic U.S. sales fell 8% to $529.9 million. So it’s no wonder this abrupt deceleration led fears that the company’s very core domestic engine is stalling, fully justifying the immediate and sustained stock sell-off.

From there, the bottom line suffered even further as gross margins compressed sharply to 65% from 73% a year ago, hurt by infrastructure investments and a deliberate pivot toward lower-margin branded glucagon-like peptide-1 (GLP-1) weight-loss products. The quarter was also heavily weighed down by restructuring charges and a legal settlement. To be fair, however, I hardly believe the market would care about short-term margins and restructuring charges had growth been exceptional. The severe slowdown in growth, especially in the U.S., which is the most monetizable region for any company, is why the bear case has become more popular recently.

The Catalysts for Re-Acceleration

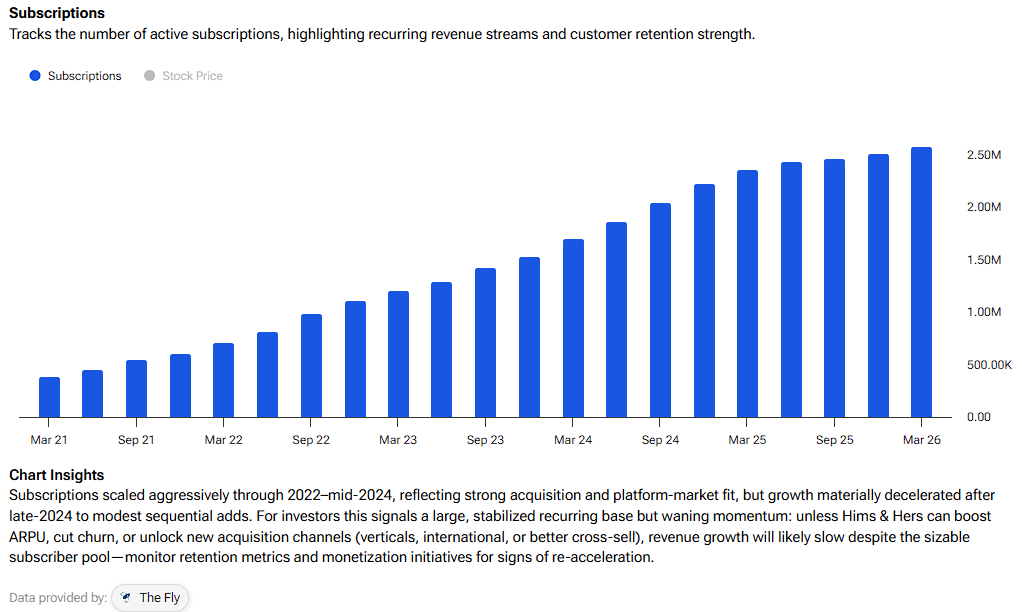

However, despite the domestic slowdown, the platform’s underlying digital ecosystem is expanding at a robust pace across the board. Total subscribers still reached nearly 2.6 million, marking a solid 9% year-over-year increase. More importantly, personalized subscribers using customized treatment plans via MedMatch technology surged 20% to 1.7 million, now representing 65% of the total user base. I like that this specific cohort seems to enjoy significantly higher long-term retention.

The most explosive catalyst, however, seems to be the international segment. International sales were up nearly tenfold, from $7.3 million to $78.2 million, due to the integration of overseas acquisitions, including ZAVA and Livewell. Simultaneously, the company is launching new clinical specialties, such as testosterone treatments. The Hers business alone is positioned to cross the $1 billion annual revenue milestone this year, also proving that Hims is successfully evolving into a diversified global healthcare ecosystem.

Management appears confident about the medium-term outlook as well. They raised the company’s full-year 2026 revenue guidance to a range of $2.8–$3 billion, pointing to 19%–28% year-over-year growth. They also expect a rapid bounce-back in Q2, forecasting revenues between $680 million and $700 million. Therefore, the recent deceleration we saw, especially domestically, could indeed prove to have been a one-off season headwind before growth picks up again.

The Valuation Puzzle

Valuing HIMS stock is quite tricky. If the market’s negative view proves correct and revenue deceleration persists, the stock could remain expensive with further downside potential. After all, Hims is not expected to post a profit this year, and even with consensus estimates of $0.56 for FY2027, the stock still trades at 41x next year’s earnings, which is undeniably a lofty multiple in a vacuum.

However, if growth reaccelerates and margins expand toward their prior levels, HIMS could actually be pretty cheap. The stock is trading at 1.85x this year’s expected sales of $2.89 billion, versus a healthcare sector median of 3.52x forward sales, while management reiterated its long-term revenue targets of at least $6.5 billion by 2030 and $1.3 billion in adjusted EBITDA. This means that if margins indeed expand, the stock should look very cheap on a P/E basis as well.

There is a chance that, with positive operating leverage in the next few years, gross margins should stabilize and possibly return to prior levels. This, in turn, should allow bottom-line earnings to scale rapidly. The recent EPS miss introduced legitimate operational questions, but the long-term risk-reward profile remains highly asymmetric, which is why I like HIMS at its current valuation.

Is HIMS Stock a Buy, Sell, or Hold?

Despite its turbulent performance, Hims & Hers stock features a Moderate Buy consensus rating on Wall Street, based on five Buy and 11 Hold ratings. Notably, no analyst rates the stock a Sell. Furthermore, HIMS’ average price target of $28.97 implies about 18.66% upside over the next 12 months.

Final Thoughts

Overall, I would argue that the recent post-earnings panic may have created a disconnect between short-term noise and long-term business fundamentals. Hims is enduring the pains of a structural pivot, but its raised guidance and international surge prove the growth story is intact. If growth continues to decline, the stock will indeed prove expensive today. However, if you trust management’s short- and medium-term outlook, then the recent drop in HIMS stock could be a compelling buying opportunity.