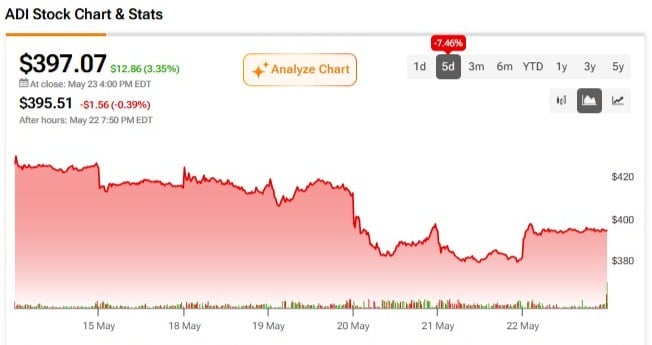

Analog Devices’ (ADI) stock reached an inflection point following its fiscal second-quarter 2026 earnings release on May 20, 2026. The global semiconductor manufacturer delivered the kind of quarter investors usually reward, beating expectations on both revenue and earnings. Despite an upgraded forward guidance for the next quarter, ADI stock experienced a sharp 7% post-earnings pullback.

Meet Samuel – Your Personal Investing Prophet

- Start a conversation with TipRanks’ trusted, data-backed investment intelligence

- Ask Samuel about stocks, your portfolio, or the market and get instant, personalized insights in seconds

This analysis adopts a Buy rating on ADI stock on the current pullback, viewing the market reaction as a classic sell-the-news event that discounts structurally expanding operating leverage and a newly fortified grid-to-core power delivery moat.

Analog Devices’ Stock Falls on Good News

Heading into the earnings print, the semiconductor stock had staged a powerful 53% year-to-date rally, driven by accelerating investor optimism surrounding its expanding footprint in artificial intelligence (AI) infrastructure, and a cyclical recovery in other business lines.

A sharp pullback, extending into Thursday’s trading, crystallizes the central investment-thesis conflict on ADI stock: the clash between an undeniably strong cyclical recovery with accelerating revenue growth and operating margin expansions powered by AI-related demand, and overstretched valuation multiples that leave a margin for error that’s increasingly too thin for investor comfort. A correction is healthy.

On the one hand, Analog Devices’ stock has rallied “too high” and appears detached from its near-term fundamental baseline, particularly given prolonged digestion cycles in legacy end markets. On the other hand, the latest operational update validated a structural transition toward higher-margin data center power architectures.

Strong Operating Performance

ADI’s accelerating revenue and earnings growth rates during the second quarter highlight the structural operating leverage inherent within its product portfolio.

The company reported record second-quarter revenue of $3.62 billion, representing a 37% year-over-year increase and exceeding consensus estimates of $3.51 billion. Revenue growth rate accelerated from 22% seen during the same quarter last year. This top-line momentum is trickling directly down the income statement, pushing adjusted gross margins up by 360 basis points year-over-year to 73%. Simultaneously, adjusted operating margins expanded by 780 basis points to 49%.

Nearly half of every dollar of revenue was an operating profit for ADI last quarter, up from 41% a year ago!

While my pre-earnings concerns flagged potential risks regarding a sluggish automotive vertical, the segment demonstrated resilient bookings alongside a 56% year-over-year surge in the broader industrial segment, which accounts for half of total revenue, and a 79% jump in communications segment revenue, propelled by a 90% increase in data center revenue.

ADI Building New AI Data Center Moats

The primary long-term fundamental catalyst for ADI’s growth includes its recent acquisitions in the power-management chip vertical. Early acquisitions of Linear Tech in 2017 and Maxim Integrated in 2021 advanced the company’s power-management offerings. Analog Devices’ newly announced $1.5 billion all-cash acquisition of Empower Semiconductor is another strategic transaction that addresses the primary physical limitation governing modern AI scaling: power density.

Empower specializes in Integrated Voltage Regulator (IVR) silicon and advanced silicon capacitors to reduce power consumption and improve energy efficiency in AI systems. By integrating this technology into its grid-to-core portfolio, Analog Devices cements a highly defensible hardware moat at the data center rack level, transforming standard power management components into high-value proprietary subsystems.

The new acquisition may help bring in significant revenue starting in 2027, CEO Vincent Roche indicated during an earnings call on Wednesday.

Valuation: ADI Stock’s Greatest Vulnerability

Analog Devices is doing well operationally and aggressively repurchasing its stock to augment shareholder returns. However, its stretched valuation is close to becoming the tech stock’s Achilles heel.

ADI’s profitability is rising, but so is the multiple investors assign to its forward earnings. The stock’s forward P/E of around 33x is 34% higher than its sector average and has risen to nearly 30% above its five-year average of roughly 25x. The tech stock generates copious amounts of cash flow. However, a forward price-to-cash flow (P/CF) multiple of 35x is nearly 85% higher than a sector median of approximately 19x, and it’s 44% higher than a five-year average of about 24.3x.

The market has re-priced Analog Devices stock higher.

That said, the above valuations are well deserved for ADI. The stock boasts a historical trailing twelve-month (TTM) revenue growth rate of nearly 30%, well ahead of peers Texas Instruments (TXN) at 15%, NXP Semiconductors (NXPI) at 2.4%, and ON Semiconductor (ON) at -9%, and its recent earnings per share growth rate of approximately 82.5% has been in its own league. None among its immediate peers has come any closer.

While valuation multiples sit above long-term historical averages and are comparably much higher than peer multiples, ADI’s premium is structurally supported by strong revenue and earnings growth, expanding corporate margins, and strong cash flow.

Watch Cash Flow

At the core of a bullish investment call on ADI stock rests capital efficiency and free cash flow conversion. On a trailing twelve-month basis, operating cash flow reached $5.1 billion, and free cash flow at $4.57 billion represented an elite free cash flow margin of 36% of revenue. This massive liquidity generation allows the enterprise to execute its $1.5 billion all-cash acquisition of Empower Semiconductor without incurring dilutive equity expansion or tapping high-coupon debt tranches.

Furthermore, capital deployment remained highly favorable to shareholders, with approximately $1.3 billion returned via dividends and share repurchases in the second quarter alone. The board sustained its quarterly dividend at $1.10 per share, which yields 1.2% and is fully insulated by strong free cash flow.

Risks to Consider

Despite Analog Devices’ strong operational momentum, the primary risk to holding the stock stems from aggressive competitive positioning within the power management integrated circuit (PMIC) sector. Entrenched competitors like Texas Instruments and Monolithic Power Systems (MPWR) are actively developing their own proprietary vertical power architectures, which could trigger a pricing war and erode the premium margins that Analog Devices currently commands.

Additionally, the $1.5 billion cash deployment for Empower Semiconductor introduces notable execution and integration risk, as the technology must be rapidly qualified by hyperscale data center architects. Furthermore, while immediate bookings are at record highs, any broader macroeconomic slowdown or tightening of capital expenditures among tier-one hyperscalers could trigger sudden inventory corrections, leaving the stock vulnerable to a severe multiple compression given its elevated valuation baseline today.

Is Analog Devices a Buy?

Wall Street analysts are bullish on Analog Devices stock, giving it a Strong Buy rating based on 18 analysts who released 17 Buys and a single Hold rating during the past three months. The average analyst price target of $459.56 implies 15.74% potential upside on ADI over the next twelve months.

Wall Street consensus remains heavily optimistic. Analysts have been raising their price targets on the semiconductor stock following its latest earnings report. Analog Devices is printing a marvelous growth story, and recent bullish price targets of $500 from KeyBank (KEY) and $515 from Wells Fargo (WFC) analyst Joseph Quatrochi may see upward revisions over the next 12 months.